Resilient Brooklyn Market Holds Firm Through Year-End Lull

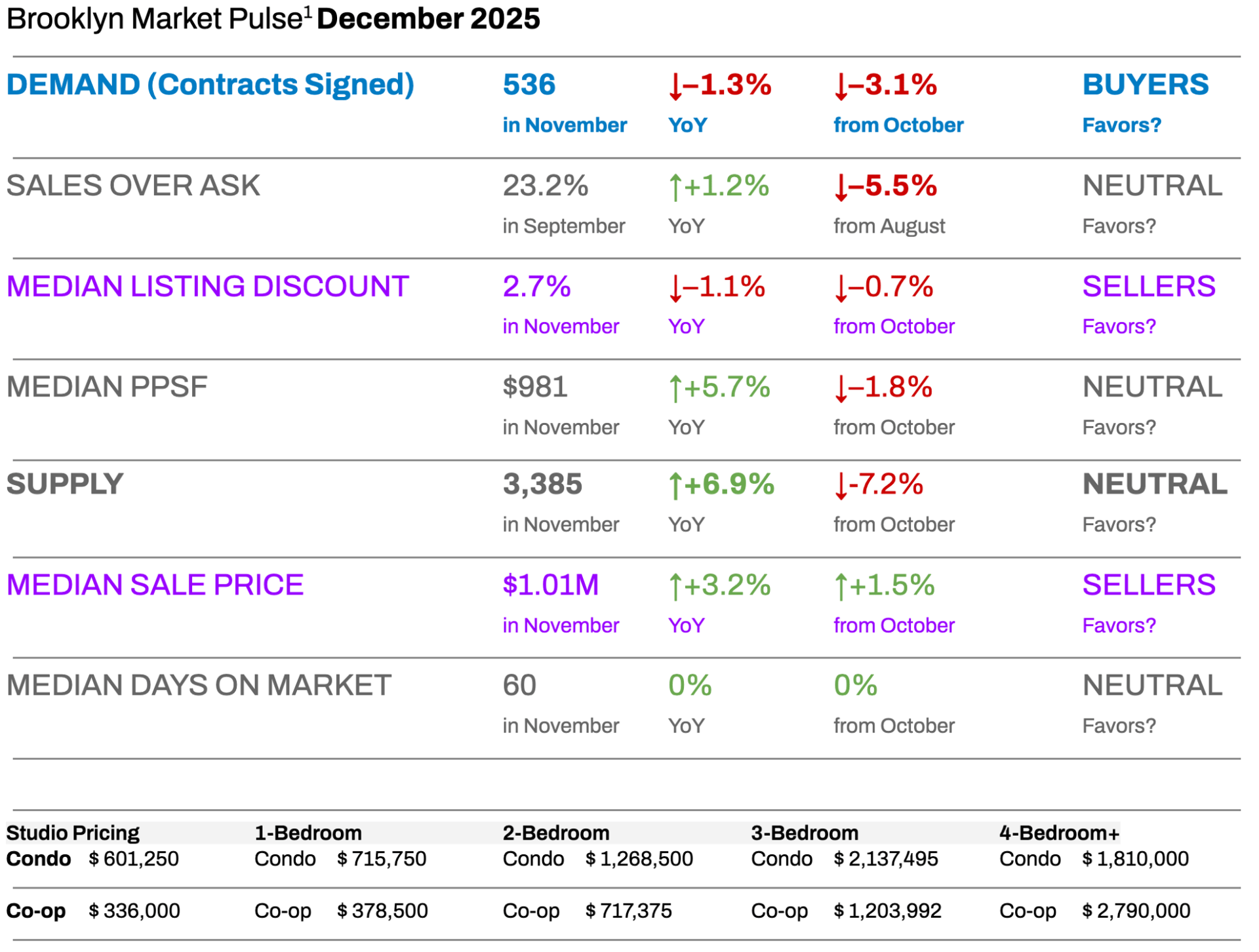

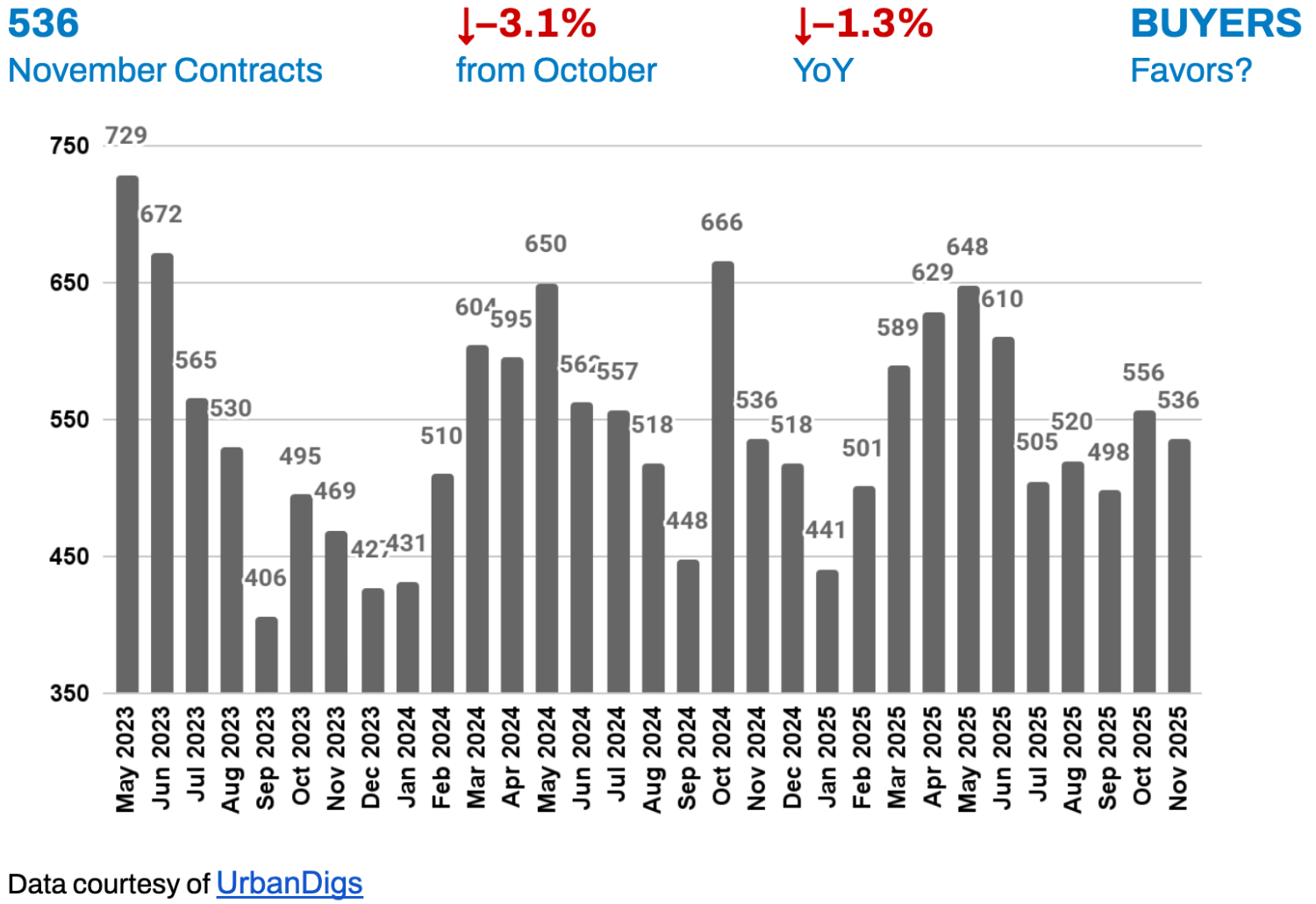

Brooklyn’s residential market saw only a mild seasonal cooldown as 2025 drew to a close. Contract signings dipped just slightly in November to 536 deals – a mere 1.3% slip from October and about 3.1% fewer than last year – signaling sustained buyer engagement even as the holidays approached. Inventory edged down 7.2% month-over-month to 3,385 active listings, a typical late-year decline, but remained 6.9% higher than November 2024.

This gave buyers a bit more choice than a year ago, though not enough to tip the scales. Overall, conditions stayed balanced with a modest edge for sellers: the Howard Hanna NYC Brooklyn Leverage Index² for November was broadly neutral, indicating no overwhelming advantage for either side but a slight tilt in sellers’ favor.

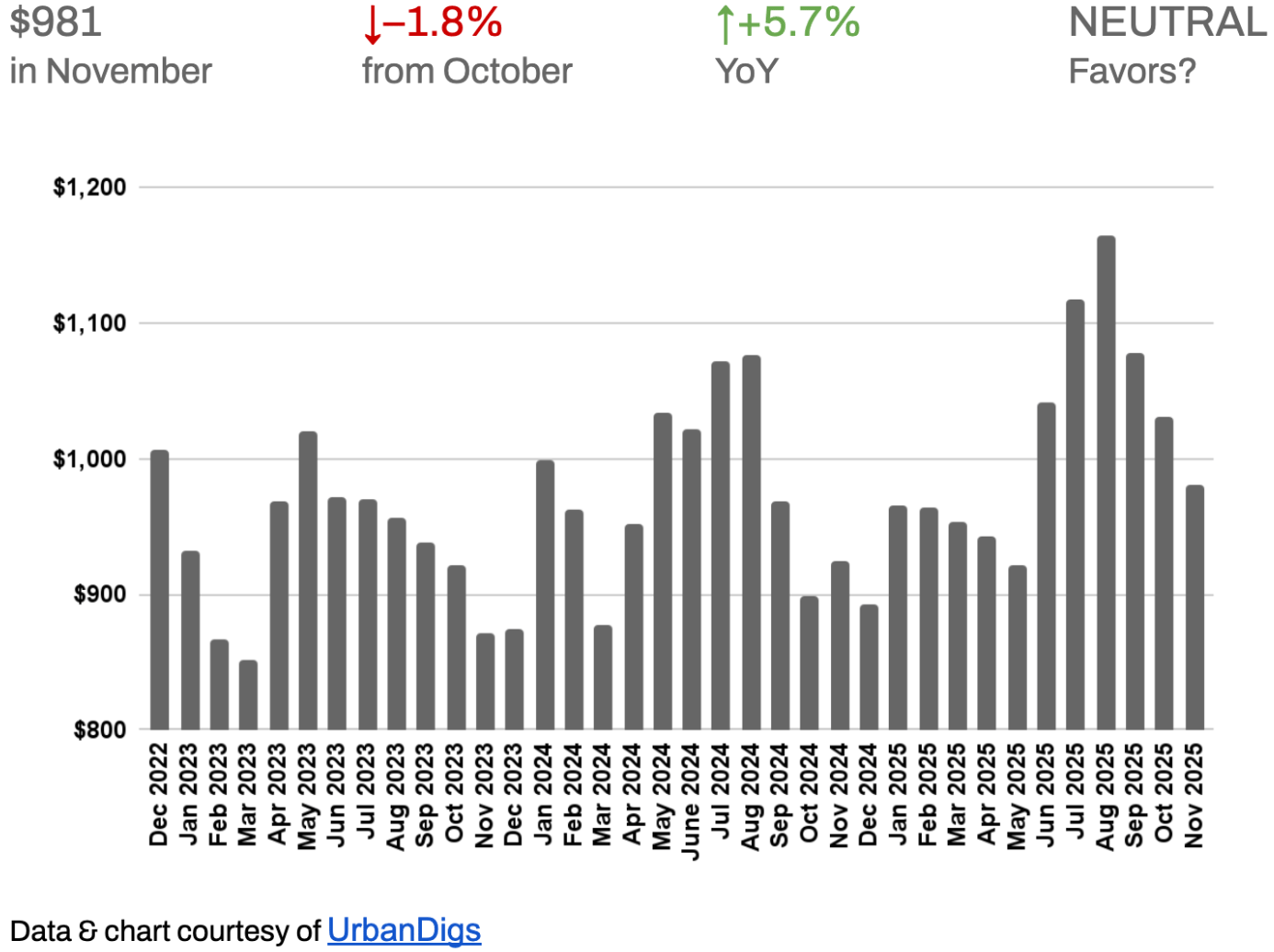

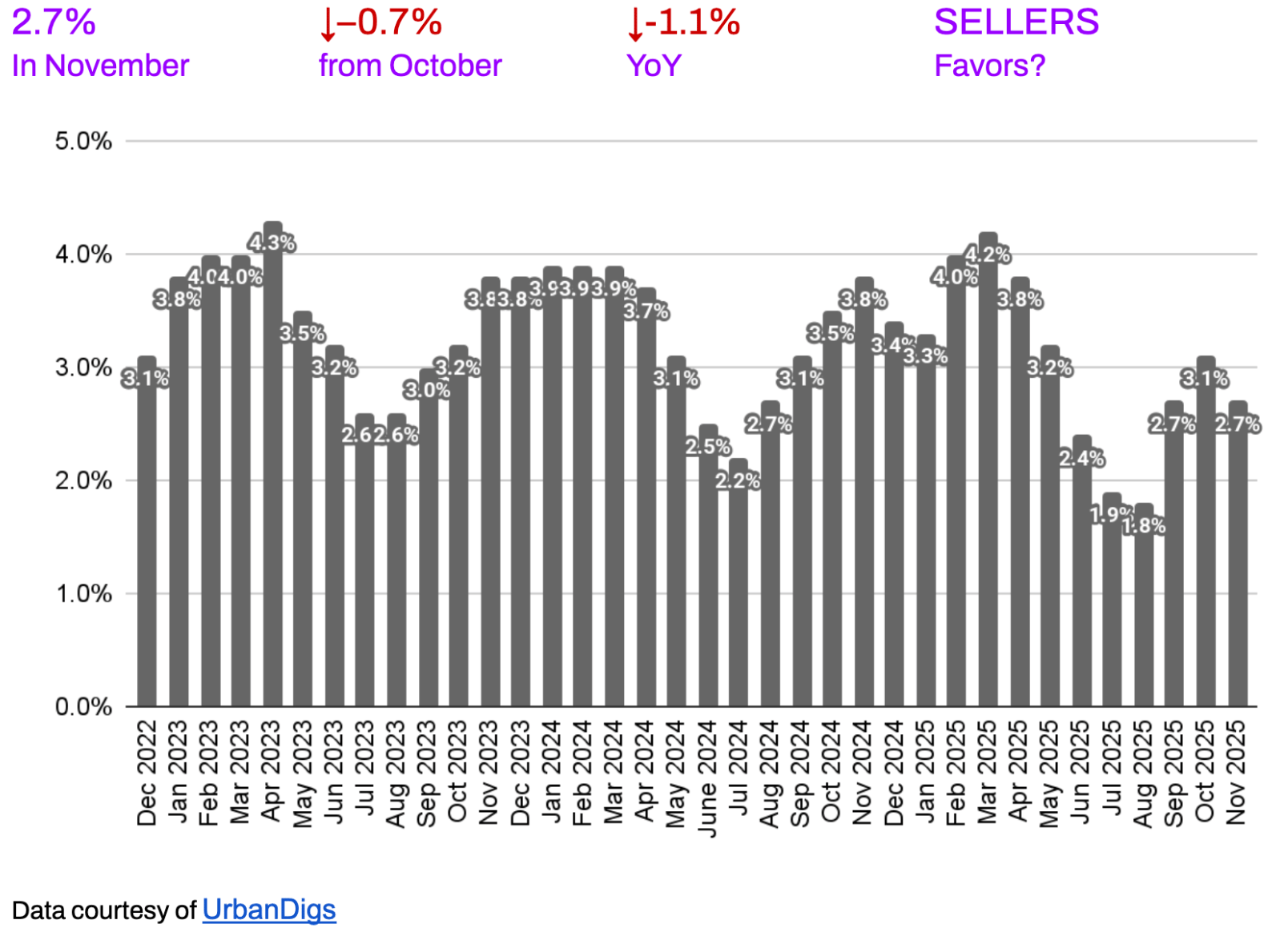

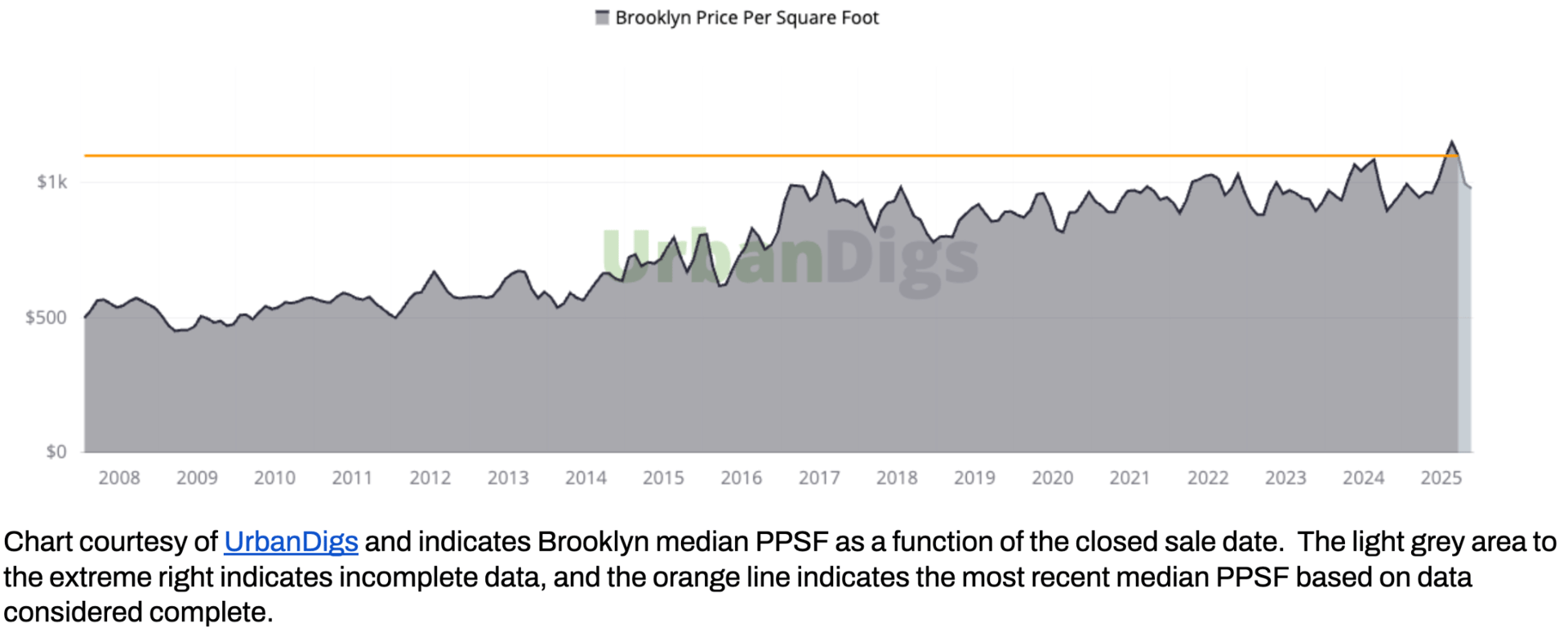

Despite the cooler season, pricing held strong across Brooklyn. The median price per square foot was $981 for November closings – a brief 1.8% dip from October’s record high, yet still 5.7% above last year’s level, highlighting solid annual appreciation. Median sale price hovered around $1.01M, up 1.5% from October and 3.2% year-on-year, marking one of the highest medians on record for the borough. Sellers also maintained significant negotiating power: the median listing discount tightened to just 2.7%, meaning homes sold for roughly 97–98% of their asking price on average.

In fact, many transactions are still seeing competitive bidding – roughly one-quarter of sales have been closing above the asking price, a testament to Brooklyn buyers’ willingness to compete for desirable, well-priced listings (down slightly from the frenzied pace of late 2024, but still robust). In short, even as sales volume cooled modestly, prices in Brooklyn remained on an upward trajectory and concessions were scarce.

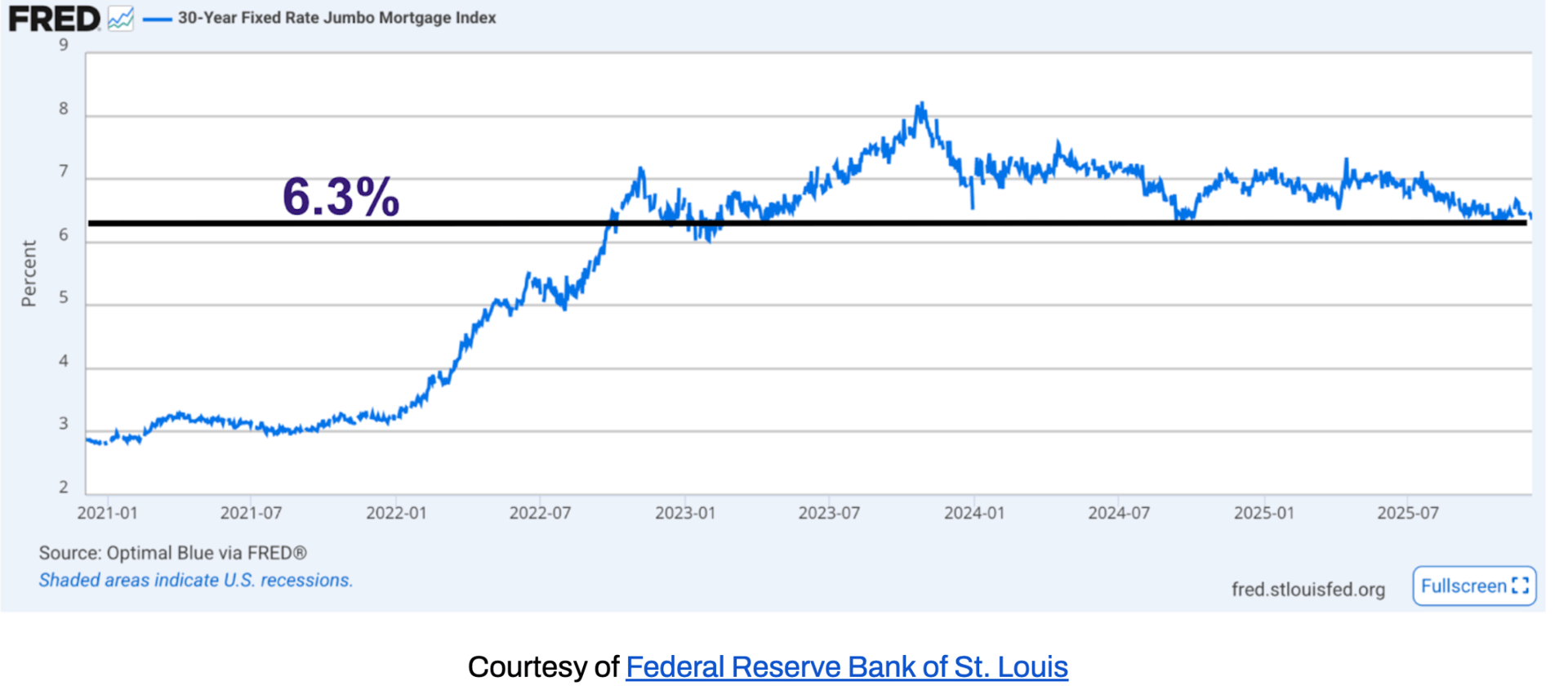

Mortgage rates, meanwhile, remain elevated but are easing off peak levels. Thirty-year jumbo rates now average roughly 6.3%, down from above 7% in Q3. This slight rate relief has yet to significantly boost buying power, but it has kept many existing homeowners “locked in” to their ultra-low pandemic-era loans – a phenomenon that continues to constrain resale inventory. Buyer demand has cooled somewhat under the weight of higher financing costs and record pricing, yet tight supply has prevented any meaningful price corrections.

However, on December 10th, the Federal Reserve lowered its benchmark interest rate to a target range of 3.50%–3.75%, signaling the first meaningful shift toward easing since mid-2023 and setting the stage for improved borrowing conditions in early 2026.

Key Takeaways

-

Mild Seasonal Slowdown: Brooklyn experienced only a modest holiday lull. Contract signings in November were nearly flat from October, declining just ~1%, which is a far gentler drop than the typical year-end cooldown. Buyer engagement remained resilient even as the winter season began.

-

Balanced Market, Seller Slight Edge: The Howard Hanna NYC Leverage Index registered roughly neutral for Brooklyn last month, reflecting a balanced playing field. Supply increased year-over-year (more listings than last November), giving buyers some breathing room, yet pricing and low discounts still lean in favor of sellers. No side has a commanding advantage, but sellers hold a bit more leverage than they did a year ago.

-

Pricing Near Record Highs: Prices held firm and even rose. November’s median sale price (~$1.01M) climbed above the $1M mark for one of the first times, up 3%+ year-on-year. Price per square foot is up ~6% annually, and about a quarter of deals are closing above ask. Homes are generally trading at 97–98% of asking price, with the median discount just 2.7%. This means well-priced properties are still attracting strong offers with minimal negotiation.

Market Outlook for 2026

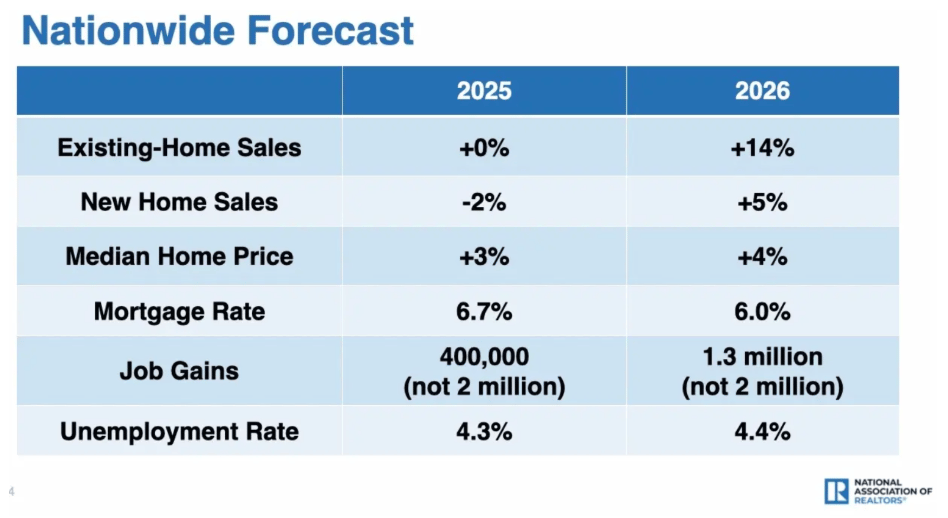

Brooklyn heads into 2026 on steady ground, with expectations of a moderate rebound. The National Association of Realtors projects a 14% increase in existing-home sales and ~4% price growth nationwide, driven by slightly lower mortgage rates and ongoing job gains.

Any drop in rates toward the mid–5% range could reignite demand among buyers sidelined in 2025. Q1 is expected to stay quiet seasonally, but activity may pick up by spring.

Price-wise, expect a stable-to-gently-rising environment. Several key factors – Federal Reserve policy, the new Mamdani administration’s stance on development and affordability, and broader macro trends – will shape market sentiment.

All signs point toward a measured market in 2026: fewer extremes, balanced activity, and continued resilience for those navigating with strategy and insight.

Photo by Rihards Gederts | Howard Hanna NYC

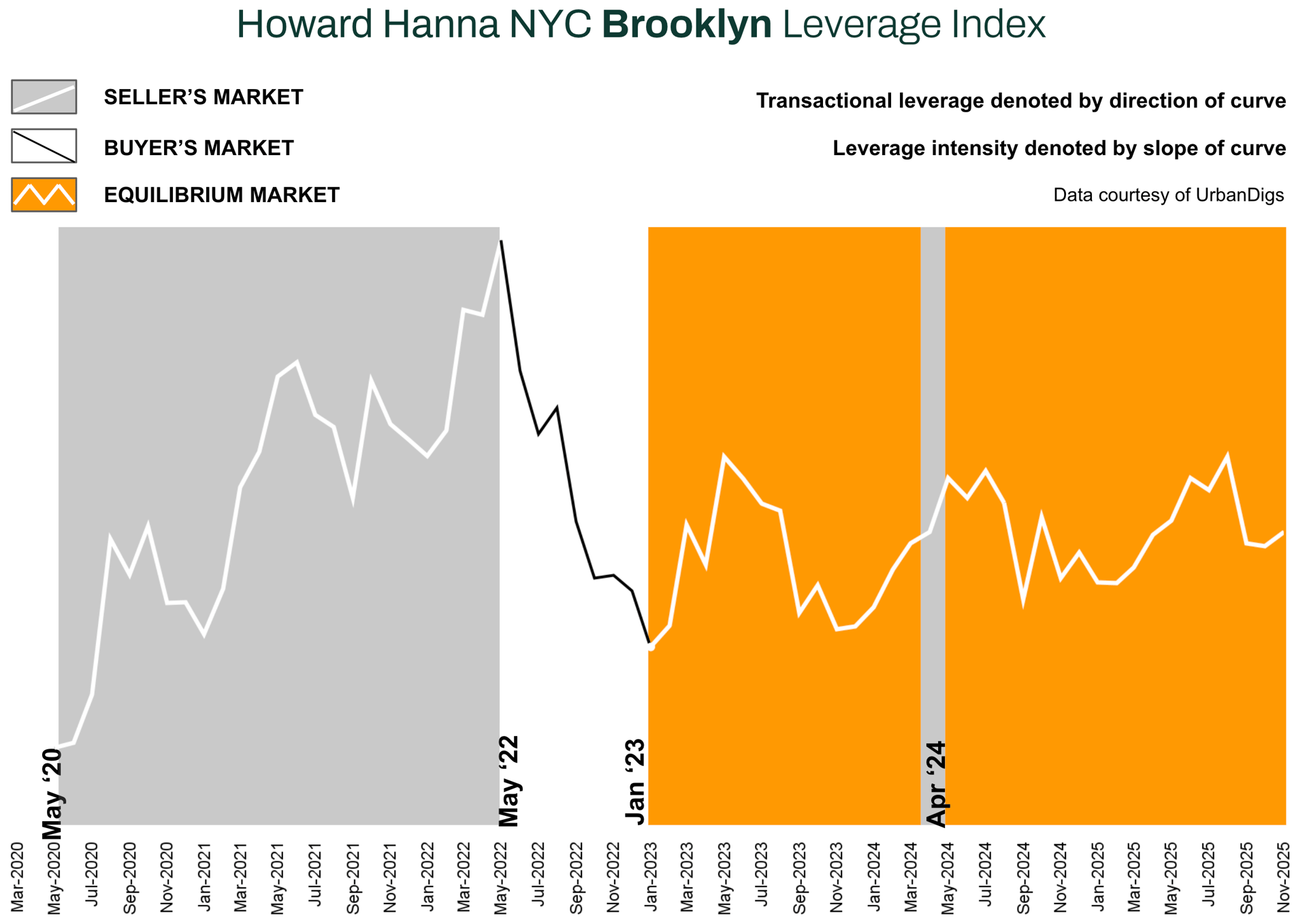

Howard Hanna NYC Brooklyn Leverage Index

The Howard Hanna NYC Brooklyn Leverage Index blends four market signals - supply, demand, median price per square foot, and median listing discount - to capture the balance of power between buyers and sellers.

Direction Matters:

-

An upward-sloping curve = seller’s market

-

A downward-sloping curve = buyer’s market

-

The steeper the slope, the stronger the advantage for either side

November’s Reading: Brooklyn’s index remained broadly neutral, with a slight uptick favoring sellers. Two of the four components moved in sellers’ favor (median listing discount tightened and median sale price rose), one stayed effectively neutral (supply, given seasonal decline but higher YOY), and one leaned toward buyers (contract demand was softer). The net result was a modest seller’s advantage for the month, though overall conditions were relatively balanced.

Buyers gained some relief from higher inventory compared to last year, but not enough to flip negotiating power entirely. Sellers still benefited from firm pricing and low discounts, giving them a subtle edge as the year ended.

Brooklyn Supply

Brooklyn Supply: Seasonal Dip, But Up Year-on-Year

Brooklyn’s active inventory contracted in November, finishing the month with approximately 3,385 listings on the market. This marked about a 7.2% decrease from October, a typical pullback as many sellers take listings off the market during the holidays or delay new listings until the new year. However, supply was still up 6.9% compared to November 2024, meaning buyers had a bit more to choose from than they did a year ago. The year-over-year rise in inventory signals that, despite the seasonal dip, Brooklyn’s available housing stock has expanded over the past 12 months – a contrast to Manhattan, where inventory was flat year-on-year.

🟩 Buyers: You have slightly more options than last year. The increase in listings versus 2024 gives you a broader selection and potentially a bit more negotiating room.

🟥 Sellers: Less competition for now. Many sellers have pulled back until after New Year’s, so those remaining on the market face fewer competing listings this month. This seasonal scarcity can work in your favor – buyers out looking in December have fewer alternatives, which can bolster your pricing power. Keep in mind, though, that compared to last year there are more homes on the market, so buyers won’t feel as pressured as they did in late 2024.

Outlook: Expect lean inventory through the winter. With numerous owners “locked in” to low mortgage rates, we don’t anticipate a flood of new listings early in 2026. Supply should stay tight into the first quarter, which will continue supporting prices.

Brooklyn Demand

Brooklyn Demand: Contracts Steady Despite Holiday Lull

Buyer demand eased only mildly in November. There were 536 contracts signed across Brooklyn for the month, representing roughly a 1.3% decline from October’s pace and about 3.1% fewer deals than in November 2024. In contrast to Manhattan – which saw a sharp post-October drop – Brooklyn’s contract activity was relatively resilient. November is typically slower after the fall rush, and 2025 followed that script, but the pullback was quite modest. Many buyers remained active through the early holiday period, perhaps taking advantage of slightly improved inventory and hoping to secure homes before year-end. The net result: November 2025 was one of Brooklyn’s slowest months of the year for sales, yet it still outperformed the prior year’s November in many respects and avoided the steep falloff seen in Manhattan.

🟩 Buyers: You saw a bit less competition than in the height of fall. With demand down slightly, there have been instances of improved negotiating leverage for buyers – particularly on homes that have sat on the market since summer.

🟥 Sellers: Serious buyers are still in the market, but expect a slower pace. Many casual shoppers have hit pause until after the holidays, so showings may be fewer.

Outlook: Anticipate a quiet December and a pickup in spring. The final weeks of the year are likely to see minimal contract activity, in line with seasonal norms. Come January and February, we expect a gradual uptick in buyer interest, but the real resurgence should arrive by spring 2026.

Brooklyn Median PPSF

Brooklyn Median PPSF: Prices Cool Slightly from Peak

Brooklyn’s median price per square foot (PPSF) for closed sales in November was $981. This figure pulled back about 1.8% from October, when PPSF hit a record high for the year. In other words, prices per square foot cooled just a touch as the market transitioned into winter. Importantly, however, PPSF remains 5.7% higher than it was a year ago – a substantial annual gain that underscores how much Brooklyn values climbed during 2025. Even with the late-year breather, Brooklyn’s pricing has shown notable resilience. The slight month-to-month dip likely reflects a shift in the mix of sales (fewer high-priced deals closing post-summer) and a natural stabilization after a vigorous run-up. By and large, sellers held firm on pricing and buyers were willing to pay near 2025’s elevated levels.

🟩 Buyers: The good news - prices aren’t spiraling upward at the moment. After a steep rise earlier in the year, Brooklyn’s PPSF has leveled off this fall. You’re not facing a runaway market in terms of pricing – November’s values were actually a bit lower than October’s.

🟥 Sellers: Prices remain on your side. Even with demand cooling, Brooklyn prices are near record highs. The surge in values over the past year has kept a firm floor under what buyers are willing to pay.

Outlook: Expect stability, not a spike, in early 2026. With inventory likely remaining tight, it’s hard to envision Brooklyn’s PPSF dropping significantly in the coming months. We anticipate flat to gently rising prices per square foot as we head into spring.

Brooklyn Median Listing Discount

Brooklyn Median Listing Discount: Negotiations Tighten Further

In November, the median listing discount – the percentage by which the final sale price lagged below the last asking price – narrowed to just 2.7% in Brooklyn. This is down from roughly 3.4% in October and about 3.8% a year ago (November 2024). In practical terms, sellers received about 97–98% of their asking price at the median, which is an exceptionally small discount by historical standards. It’s the lowest median discount Brooklyn has seen in recent memory.

This tightening of negotiation room indicates that most sellers are pricing their homes close to market value and buyers, despite being price-conscious, are not finding much scope to haggle. Compared to Manhattan’s ~4.4% median discount, Brooklyn’s market has been allowing far less wiggle room. Deals in Brooklyn are, on average, very close to asking price, reflecting the persistent competition and strong pricing environment in the borough.

🟩 Buyers: Don’t expect big bargains. On most Brooklyn listings, paying within a few percentage points of the asking price is the norm. Deep discounts are largely limited to homes that were overpriced to begin with or have sat on the market for a long time.

🟥 Sellers: Brooklyn is not a “discount” market right now. On average, sellers are achieving around 97–98% of list price, which means you hold considerable negotiating power.

Outlook: Minimal discounts likely to persist. We anticipate that listing discounts will remain tight through the winter and into early 2026. Unless there’s a major shift – for instance, a surge of new listings or a sudden drop in buyer demand – there’s little reason to expect Brooklyn’s negotiation margins to widen significantly.

Rental Remarks

Rents Near Record Highs, Tenants Still Squeezed

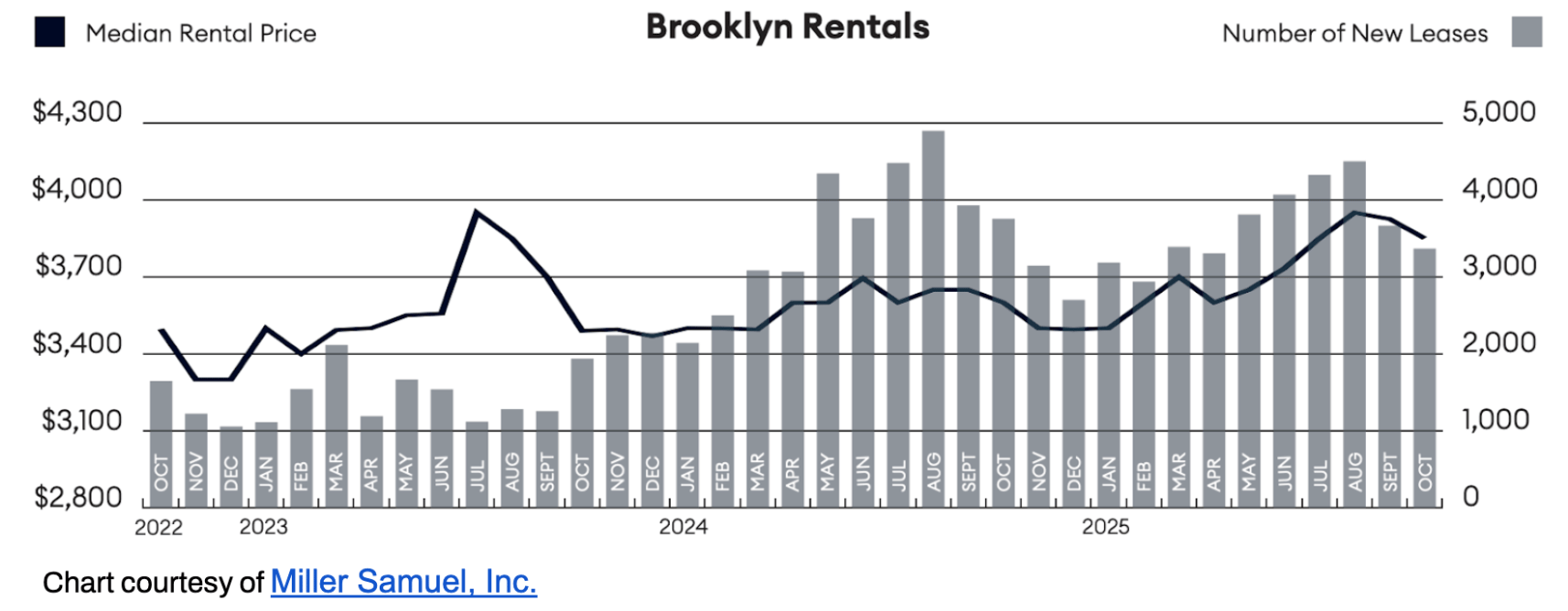

Brooklyn’s rental market remained historically tight in October, with median rent at $3,850 – down 1.9% from September, yet still 6.9% higher than a year ago, marking the third-highest level on record.³ Both median and average rents climbed annually, outpacing the U.S. inflation rate of roughly 3%. Meanwhile, new lease signings fell year-over-year for the fourth consecutive month, reflecting affordability constraints and lease renewals by tenants reluctant to re-enter a competitive market.

The average apartment size leased shrank for the seventh straight month, as renters adjusted expectations to stay within budget. Notably, the listing discount remained negative for the 26th consecutive month, meaning the typical unit continues to rent at or above asking price – a strong signal of landlord leverage and tight inventory conditions.

-

Renters: Brooklyn renters are still under heavy cost pressure as near-record pricing, shrinking unit sizes, and negative listing discounts signal an environment where affordability keeps eroding and negotiation leverage remains minimal.

-

Landlords: Continue to operate from a position of strength, with units renting at or above ask for more than two years straight and sustained demand allowing owners to hold pricing power even as lease activity cools.

-

Outlook: The rental market is poised to stay tight through early 2026, with limited new supply and entrenched affordability constraints keeping rents elevated while offering no meaningful relief for tenants.

Mortgage Remarks

Mortgage Rates: Slight Rate Relief, But the “Rate Lock” Effect Lingers

Slight Rate Relief, But the “Rate Lock” Effect Lingers – Mortgage rates remain elevated but are drifting lower from their 2023 peaks. As of December, the average 30-year jumbo loan rate hovers around 6.3%⁴, down from the 7%+ levels seen in early autumn. The jumbo APR (annual percentage rate) settled near 6.1%⁵ in November. This gradual easing has provided some relief to buyers’ monthly payment calculations, but rates are still high by historic standards – a reality that continues to weigh on affordability.

One notable consequence of these elevated rates is the persistent “rate lock” effect. Thousands of Brooklyn (and NYC) homeowners refinanced or purchased homes at 3% or 4% rates in years past; now, with mortgages in the 6–7% range, those owners are reluctant to sell and give up their ultra-low rates. This dynamic keeps many would-be sellers on the sidelines, directly contributing to the limited supply of homes for sale. In turn, buyer demand has been somewhat weaker than it would be with cheaper financing, as higher borrowing costs squeeze budgets and sideline some first-time buyers. Affordability pressures – driven by the combination of elevated prices and higher mortgage rates – have become a top concern, especially for entry-level buyers. Even factors like softer immigration flows into NYC (post-pandemic) play a role, modestly reducing demand at the margins.

Outlook: On December 10th, the Federal Reserve lowered its benchmark interest rate to a target range of 3.50%–3.75%, signaling the first meaningful shift toward easing since mid-2023 and setting the stage for improved borrowing conditions in early 2026. Don’t expect sub-5% rates without a recession.

Investor Insights

Currency Shifts Offer a Hidden Discount: 2025 brought a quieter but meaningful tailwind for international real estate investors: a weakened U.S. dollar. The dollar declined roughly 4–5% year-to-date against major world currencies. For overseas buyers, this currency movement translates into an immediate cost advantage. A property priced at $1 million in New York now effectively costs a European buyer about €875,000–€880,000, compared to roughly €920,000 a year ago – purely due to exchange rate changes. Similar math applies to purchasers using British pounds, Japanese yen, and other currencies that strengthened versus the dollar.

This ~5% FX edge makes Brooklyn real estate more affordable for global investors than it was at the start of the year. Coupled with Brooklyn’s robust fundamentals – high rental demand, growth potential, and relative value next to Manhattan – the currency discount has been an added incentive for international buyers. We expect Brooklyn to continue attracting foreign capital into 2026, as long as the dollar remains at these more favorable exchange rates.

ReferencesEmpty heading

1. Data courtesy of UrbanDigs

2. According to the Howard Hanna NYC Brooklyn Leverage Index

3. Data courtesy of Miller Samuel, Inc.

4. Data courtesy of Federal Reserve Bank of St. Louis

5. JUMBO mortgage rate APR data courtesy of Bank of America, Chase, and Wells Fargo

6. Cover Photo by Rihards Gederts - Howard Hanna NYC.

If you would like to chat about the most recent market activity,

feel free to contact us at [email protected] or

connect with one of our Advisors.

About Us

Howard Hanna NYC brings the nation’s largest independent and family-owned brokerage to New York City, uniting the strength of a national network with the insight and sophistication of a local firm. Formed through joining forces with Elegran Real Estate, Howard Hanna NYC delivers a seamless, full-service experience backed by more than 15,000 agents across 500 offices in 14 states. The firm’s forward-thinking, agent-first culture continues to shape the future of real estate across Manhattan and the Tri-State area.

Learn more at www.howardhannanyc.com.