Buyer Leverage Emerges as Demand Softens and Pricing Adjusts

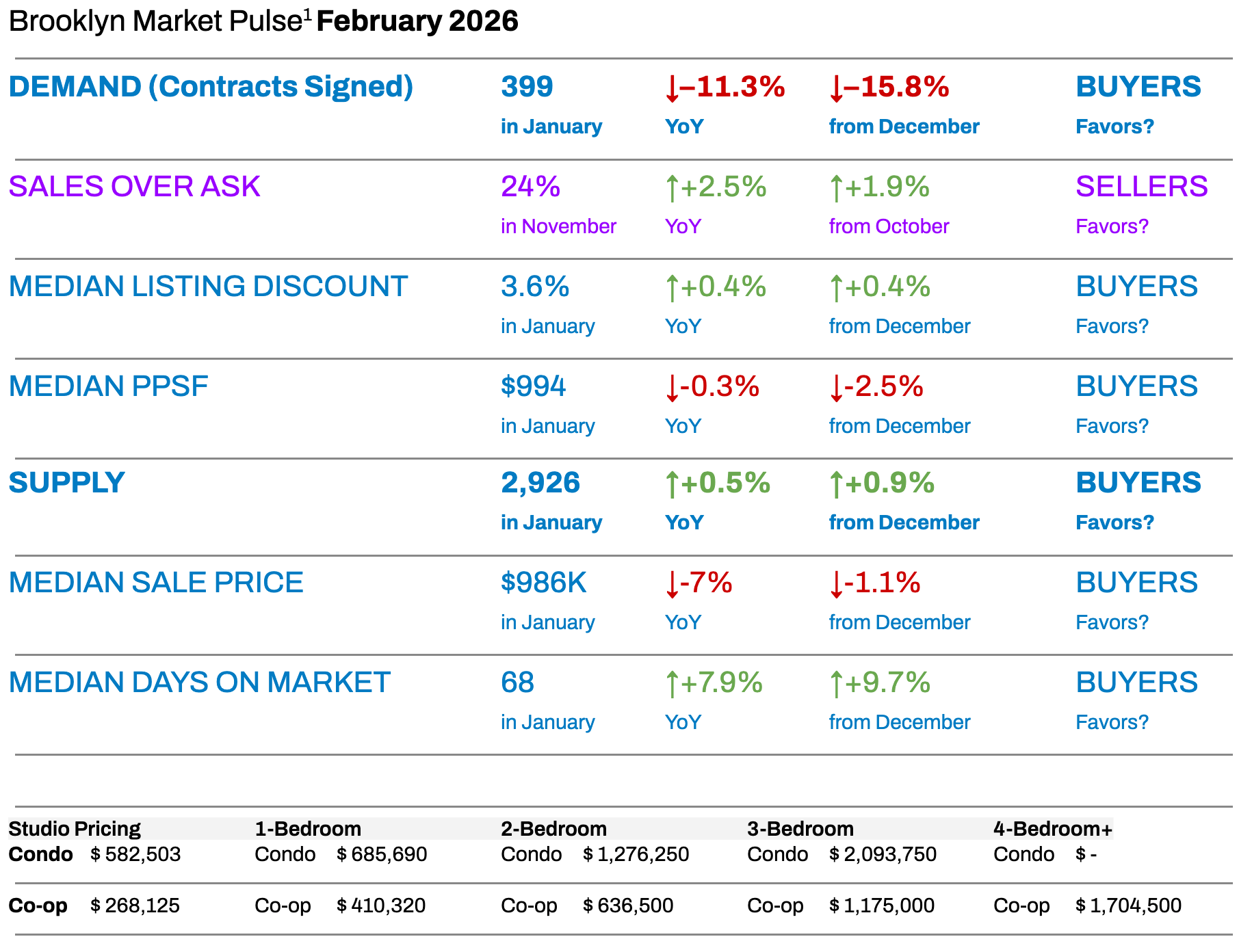

Brooklyn’s residential market entered 2026 on a different trajectory than Manhattan, with buyer leverage re-emerging across nearly all major transactional indicators. While pricing and activity remain orderly, demand has softened materially. Median days on market rose to 68 days in January, up +7.9% year over year and +9.7% from December, signaling slower absorption and strengthening buyer leverage. Combined with modest inventory growth and easing price metrics, these dynamics have pushed Brooklyn firmly into buyer-market territory.

Unlike Manhattan’s equilibrium-driven normalization, Brooklyn is undergoing a pricing and liquidity reset following several years of rapid appreciation. This shift reflects affordability constraints, reduced urgency, and more selective buyer behavior rather than distress or forced selling. Importantly, the adjustment is occurring within a stable macro backdrop, supported by conservative lending standards and resilient rental fundamentals.

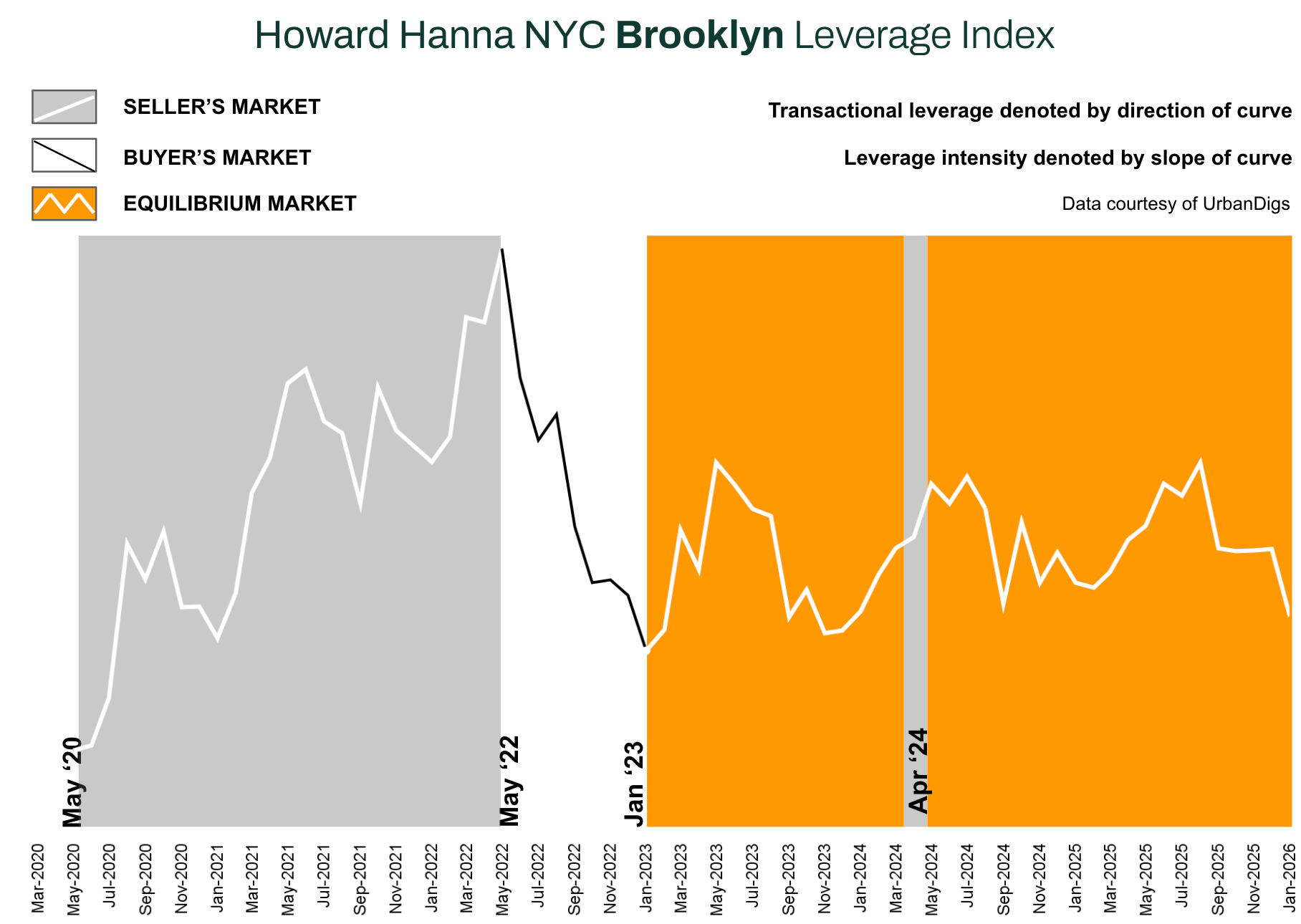

From a leverage perspective, the Howard Hanna NYC Brooklyn Leverage Index moved firmly into buyer territory in January. All four index components — demand, supply, median PPSF, and listing discount — tilted in buyers’ favor, marking the strongest buyer leverage Brooklyn has experienced in nearly three years. The key distinction in the current cycle is that liquidity has weakened faster than pricing, allowing buyers to regain negotiating power without triggering broad price dislocation.

Two Numbers That Define the Market

-

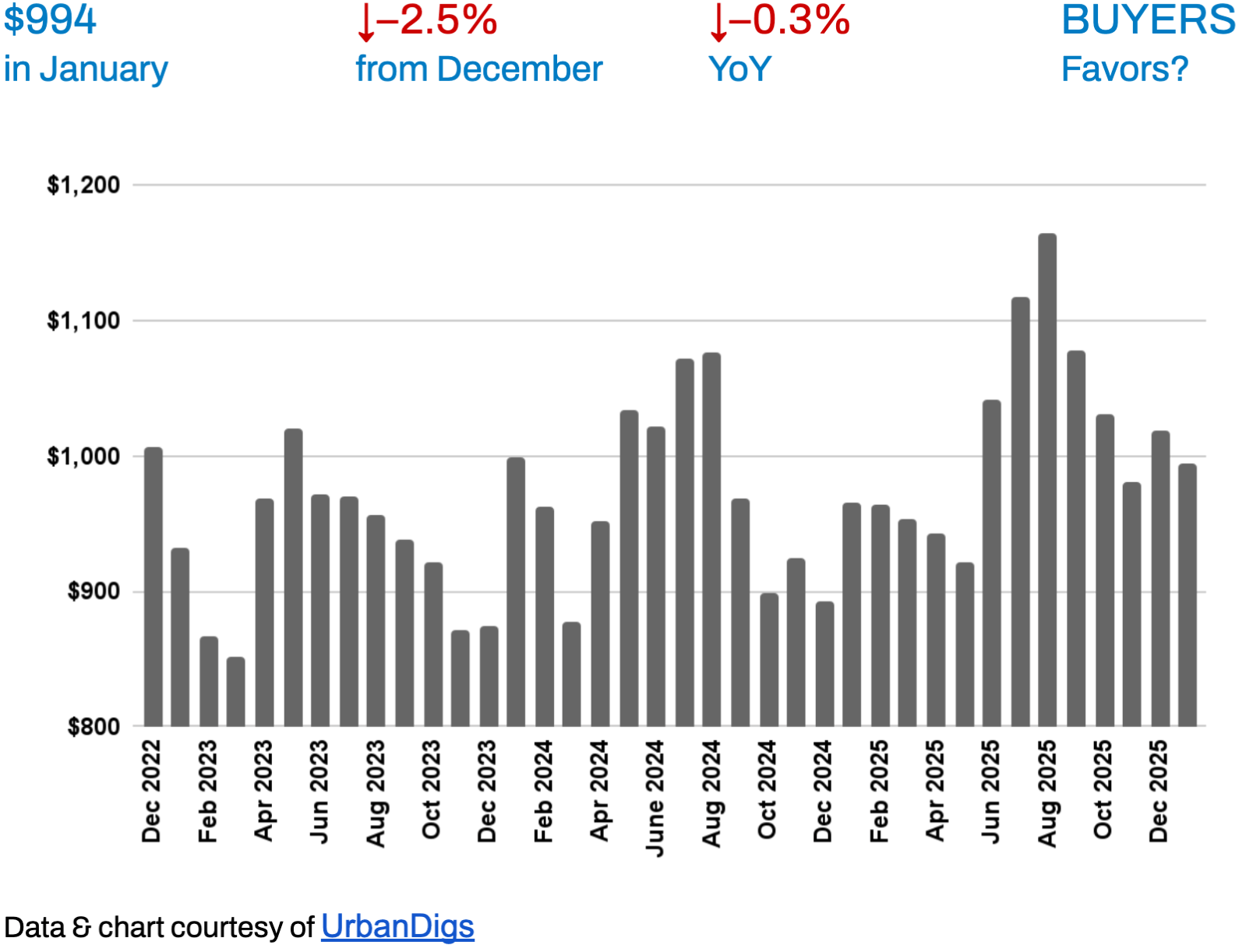

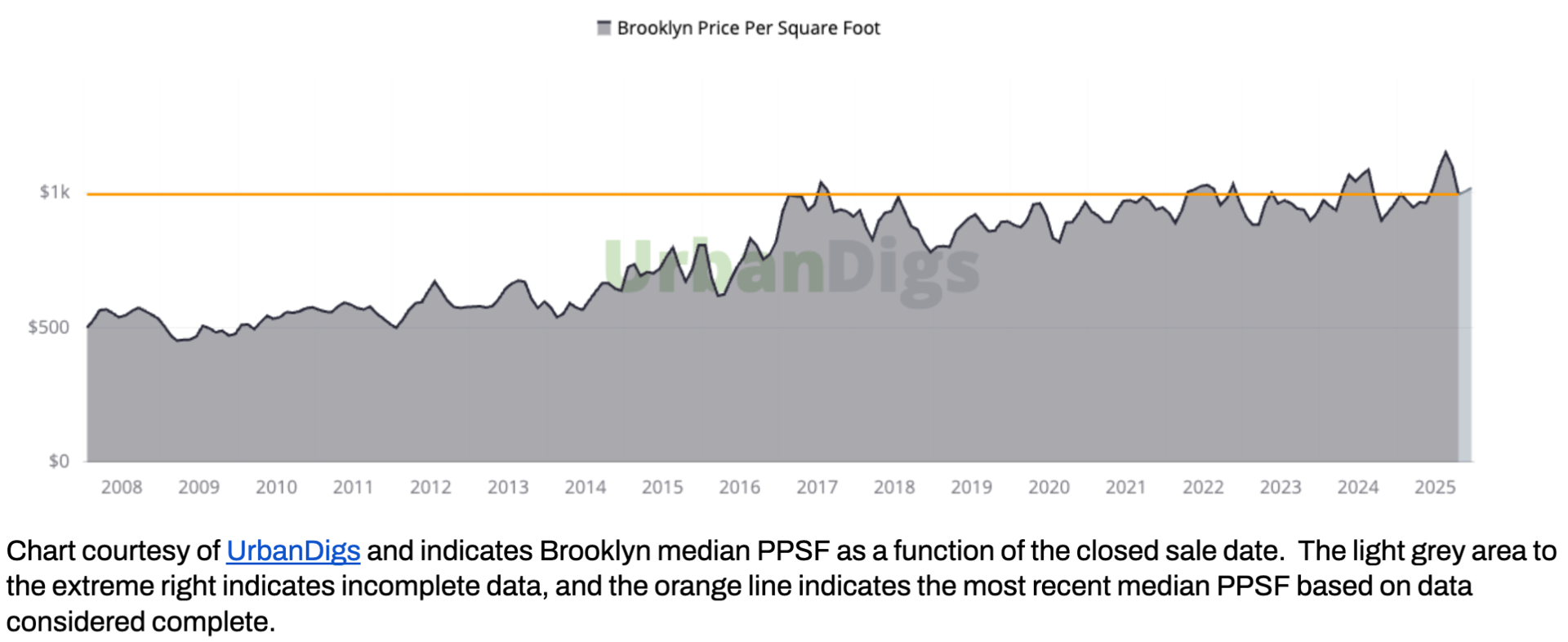

$994 Median Price per Square Foot

Down –2.5% month over month and –0.3% year over year, signaling meaningful price cooling after outsized gains in 2024–2025. -

399 Contracts Signed in January

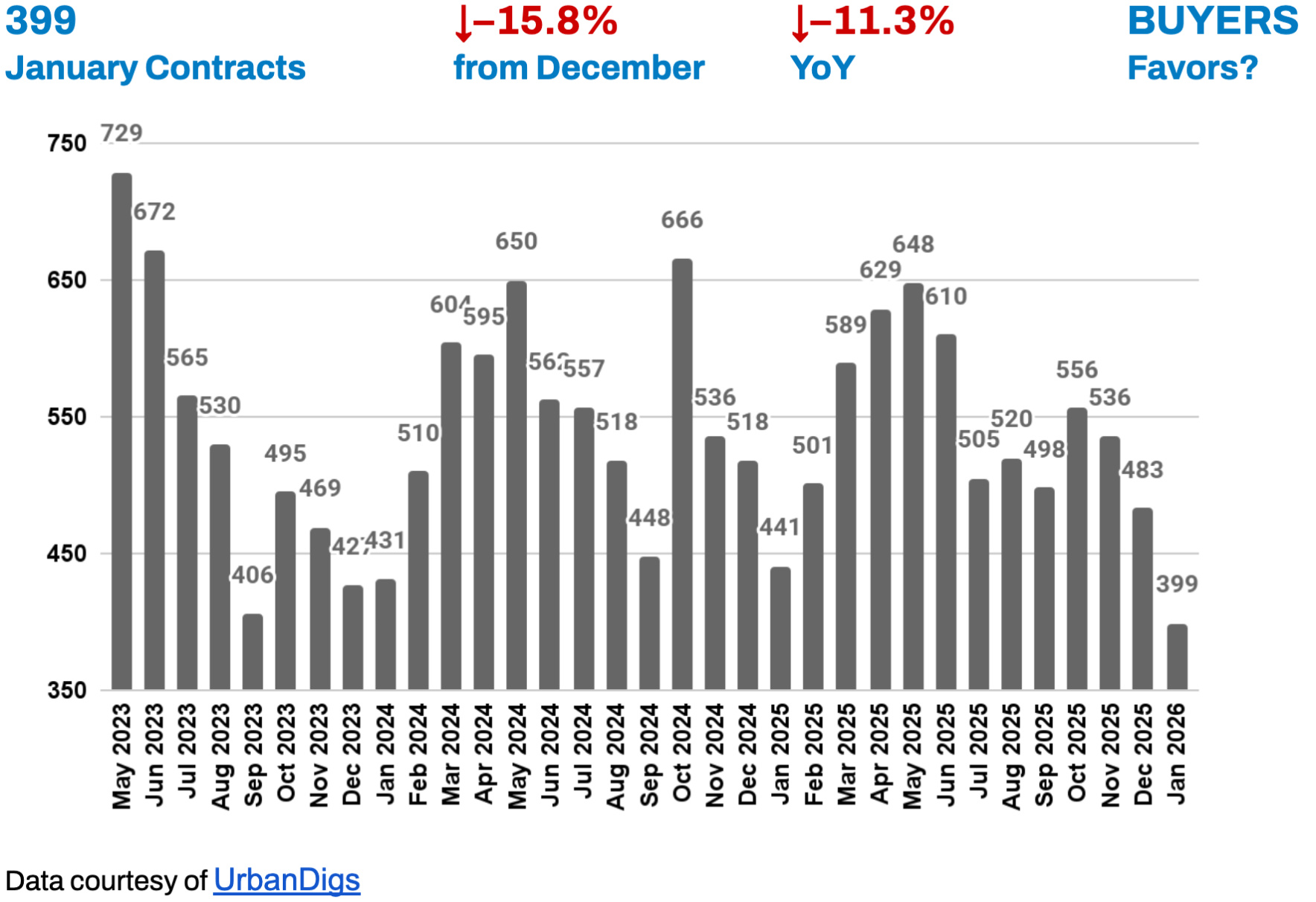

Down –15.8% from December and –11.3% year over year, the lowest monthly contract volume since 2021.

Together, these figures confirm a classic early-stage buyer-market dynamic: transaction velocity is adjusting first, while prices follow more gradually.

Key Insight: Brooklyn has entered a buyer-led phase of normalization, where pricing, demand, and leverage are resetting after years of outsized growth — not collapsing, but rebalancing.

Outlook for Spring 2026: Absent a sharp rate decline or macro shock, Brooklyn is likely to remain a buyer-friendly market into spring 2026. Well-capitalized buyers should find increasing opportunity as sellers adjust expectations, while successful sellers will need to prioritize pricing accuracy, presentation, and execution speed in a slower, more selective environment.

Photo by Rihards Gederts | Howard Hanna NYC

Howard Hanna NYC Brooklyn Leverage Index

The Howard Hanna NYC Brooklyn Leverage Index² blends four market signals - supply, demand, median price per square foot, and median listing discount - to capture the balance of power between buyers and sellers.

Direction Matters:

-

An upward-sloping curve = seller’s market

-

A downward-sloping curve = buyer’s market

-

The steeper the slope, the stronger the advantage for either side

In January, the index moved decisively into buyer-market territory. Contract activity fell sharply, inventory expanded modestly, median PPSF declined, and listing discounts widened. Unlike Manhattan, where offsetting forces keep leverage balanced, Brooklyn’s indicators aligned in the same direction.

This shift does not signal stress. Instead, it reflects a post-appreciation normalization cycle, where buyers regain leverage as affordability caps pricing momentum.

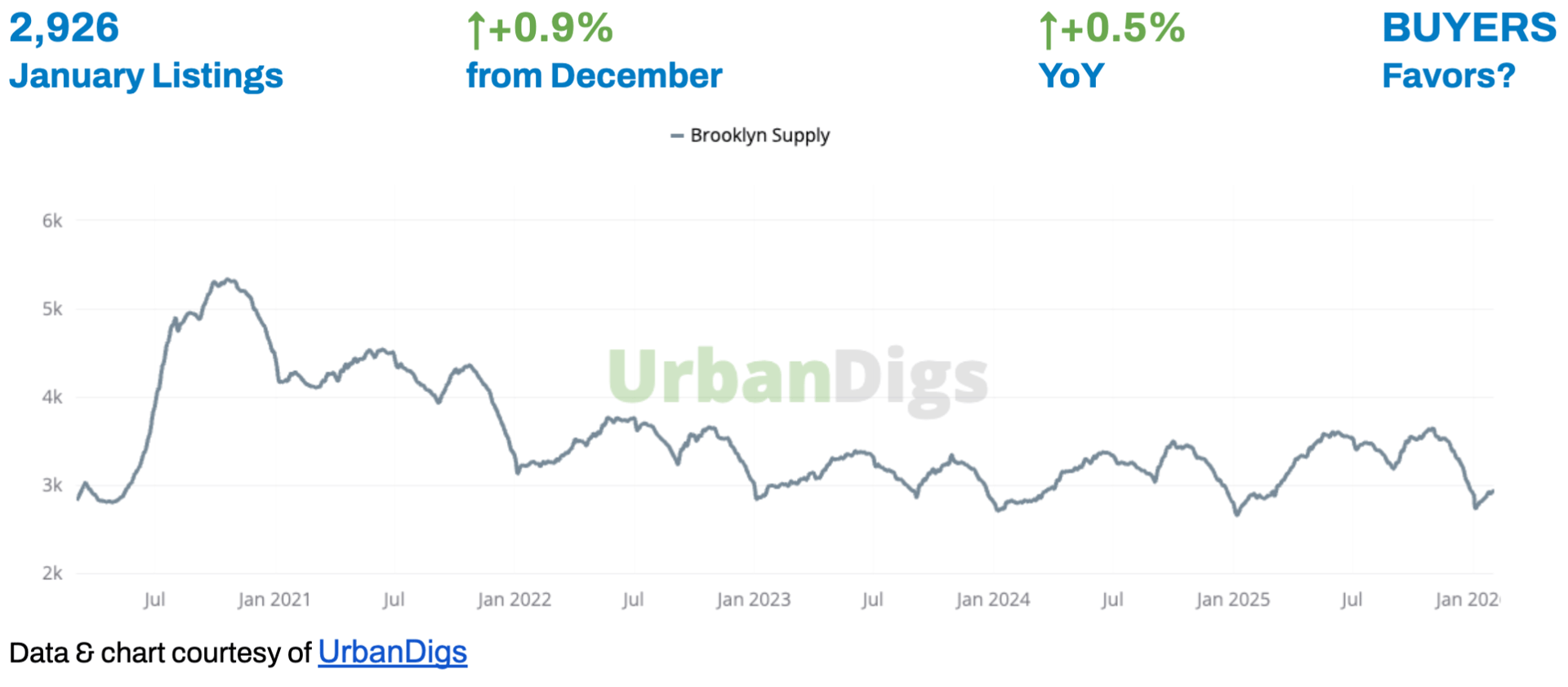

Brooklyn Supply

Brooklyn Supply: Inventory Expands Modestly, Improving Buyer Choice

Brooklyn inventory rose modestly in January following the holiday slowdown, reaching 2,926 active listings — up 0.5% month over month and 0.9% year over year. This modest expansion gives buyers more options than at any point since early 2023.

🟦 Buyers: Expanded choice and longer marketing times improve negotiating leverage, especially above $1M.

🟪 Sellers: Competition has increased, making pricing accuracy critical.

Outlook: Inventory is likely to continue building gradually into spring, reinforcing buyer leverage.

Brooklyn Demand

Brooklyn Demand: Contract Activity Hits Multi-Year Lows

January marked Brooklyn’s lowest monthly contract count in nearly three years, with 399 contracts signed, representing a 15.8% decline month over month and an 11.3% drop year over year. While seasonal effects played a role, the magnitude of the decline points to genuine demand cooling.

🟦 Buyers: More deliberate, patient, and price-sensitive.

🟪 Sellers: Only well-priced listings are clearing efficiently.

Outlook: Demand may stabilize later in Q2, but urgency is unlikely to return without rate relief.

Brooklyn Median PPSF

Brooklyn Median PPSF: PPSF Retreats After Years of Rapid Growth

Brooklyn’s median price per square foot stood at $994 in January, down –2.5% from December and –0.3% year over year, a movement that clearly favors buyers and reflects an early-cycle price adjustment rather than a broad market decline.

🟦 Buyers: Pricing softness creates entry opportunities, particularly in discretionary segments such as luxury condos, new developments, and higher-end brownstones where sellers have more flexibility and buyer urgency has eased.

🟪 Sellers: Recent peak pricing is proving difficult to sustain.

Outlook: Further modest price discovery is likely before stabilization, meaning sellers may need to adjust asking prices slightly lower until buyers and sellers reach a new equilibrium. Once that balance is found, pricing should flatten and transaction activity can begin to recover.

Brooklyn Median Listing Discount

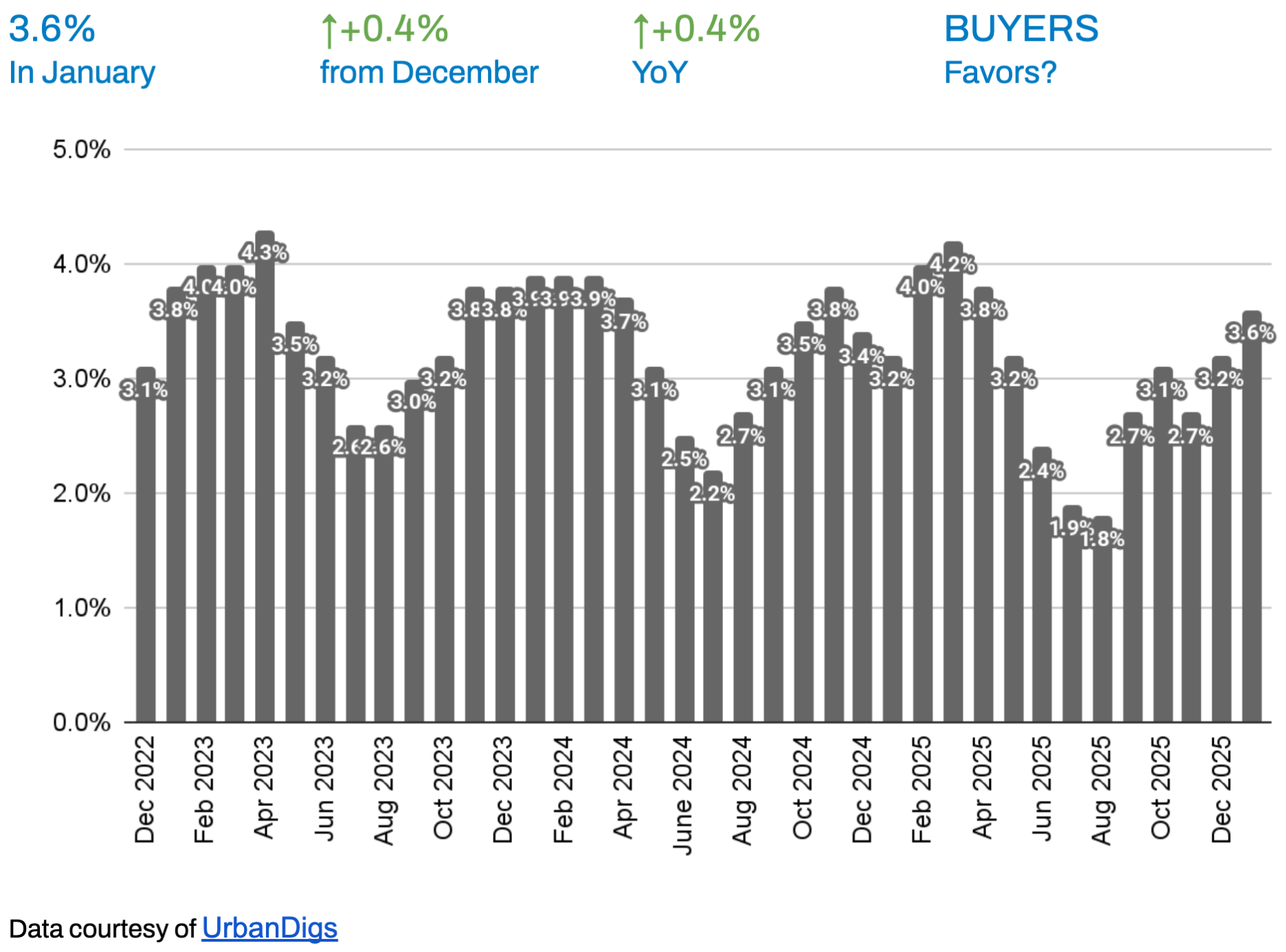

Brooklyn Median Listing Discount: Listing Discounts Widen as Leverage Shifts

Discounts widened to 3.6%, up from roughly 3.2% in December. Homes are now selling for about 96.4% of last asking price. This indicates that sellers are conceding more during negotiations, reflecting a market where buyers have gained meaningful leverage.

🟦 Buyers: Negotiating room has meaningfully improved, with more listings lingering on the market and sellers increasingly open to price adjustments or closing-cost concessions. Buyers now have the flexibility to compare options, negotiate contingencies, and secure more favorable terms than they could just a few months ago.

🟪 Sellers: Concessions are increasingly required to transact, or minor price adjustments to maintain buyer engagement and ensure deals move forward.

Outlook: Discounts may widen further if demand remains soft.

RENTAL REMARKS

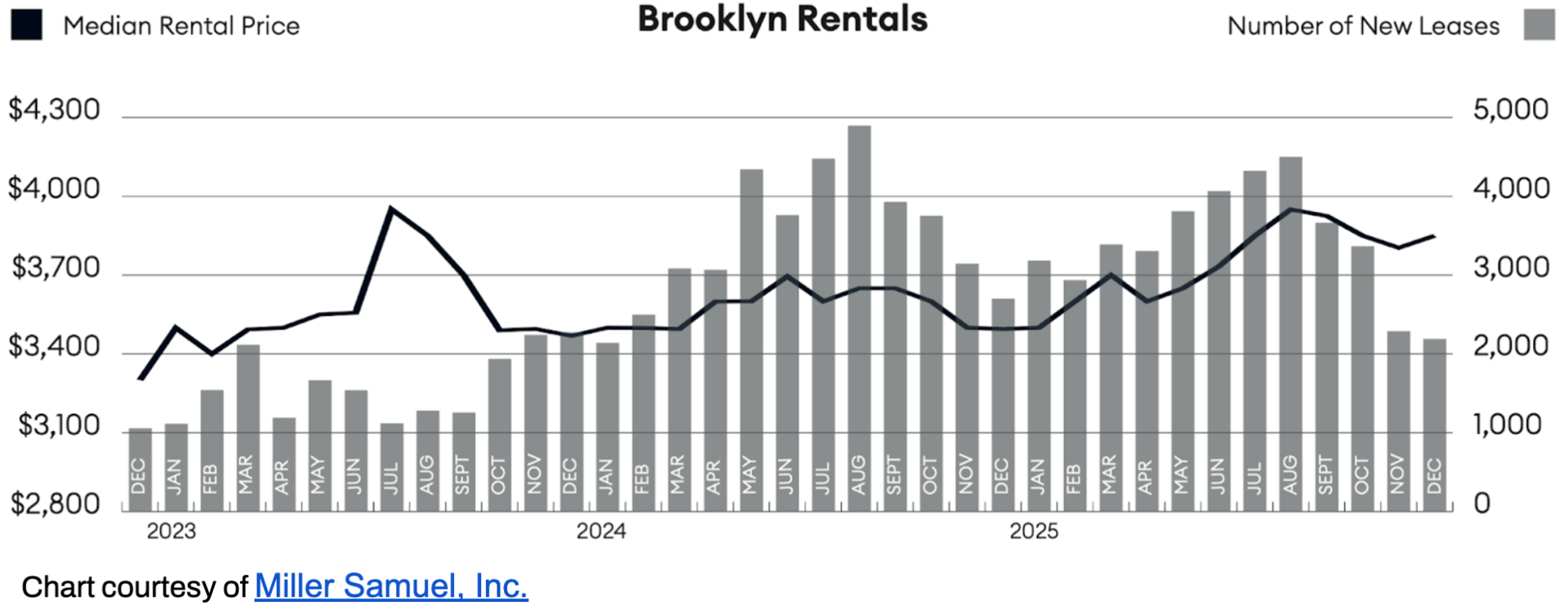

Rental Strength Offsets Ownership Softness

Brooklyn’s rental market remained historically tight through the year-end. December median rent reached approximately $3,850, up +10.2% year over year. Inventory declined and bidding wars persisted, with more than 30% of leases closing above ask³.

🟦 Renters: Affordability pressure remains acute, with many households allocating a growing share of income to rent and facing limited relief from rising utility and maintenance costs.

🟪 Landlords: Strong rent growth and low vacancy support cash-flow stability, providing consistent income streams and reinforcing confidence in long-term property performance.

Outlook: Rental strength continues to underpin long-term ownership demand by providing landlords with stable income streams and reinforcing confidence in housing market fundamentals. For renters, conditions remain challenging: constrained supply and persistent demand are likely to keep rents elevated through much of 2026, with only modest relief unless new inventory materializes or ownership demand softens meaningfully.

MORTGAGE REMARKS

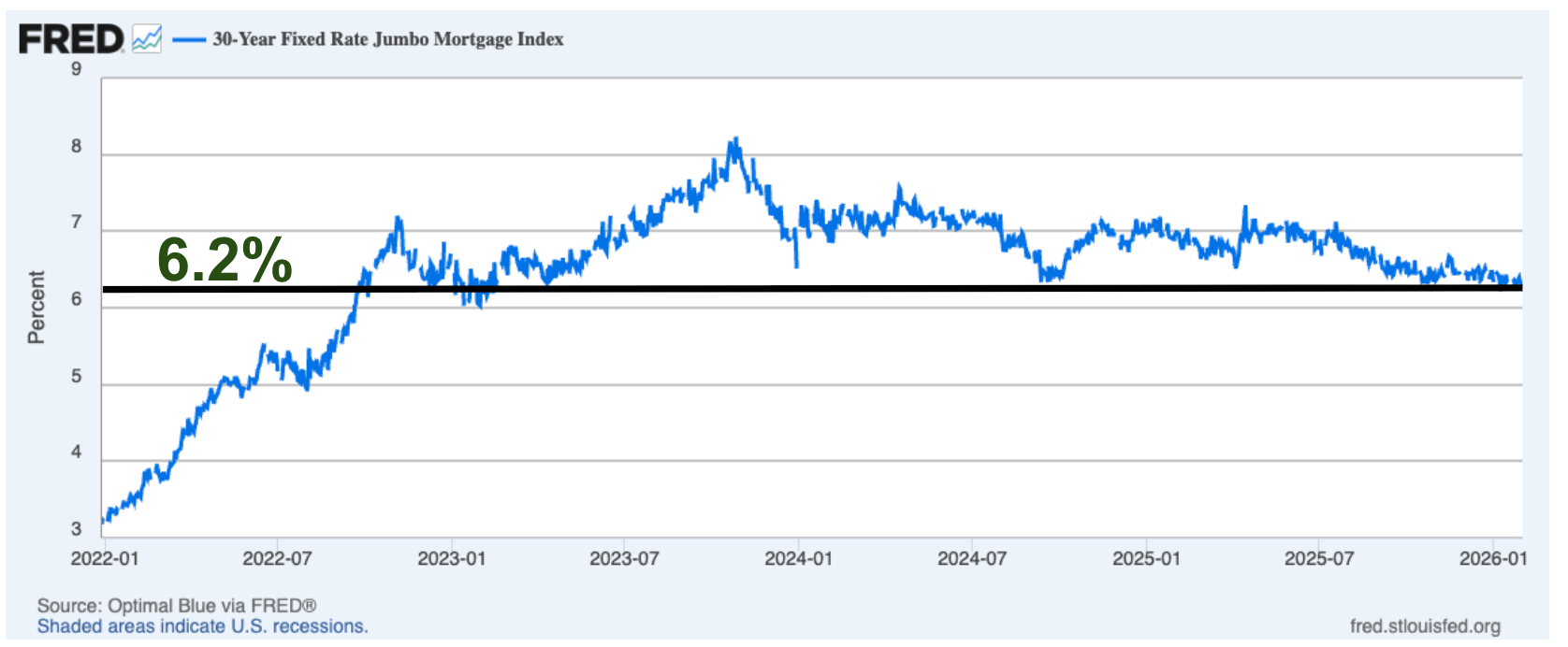

Mortgage Rates: Rates Stabilize, Reducing Shock Risk

By year-end, average 30-year jumbo rates settled near 6.23%⁴, down from 2025 peaks above 7%. The APR for jumbo loans (which factors in some fees) settled near 6.28%⁵ in January. While still elevated, rate stability has reduced transaction friction and improved planning confidence.

Market Drivers: While jumbo mortgages are not directly tied to the Fed funds rate, the Federal Reserve’s decision to hold policy rates in the 3.5%–3.75% range has reduced rate volatility by stabilizing long-term yields and bank credit spreads, helping anchor pricing for higher-balance loans.

Outlook: Even modest rate declines could disproportionately benefit Brooklyn due to lower absolute price points compared to Manhattan.

INVESTOR INSIGHTS: Normalization, Not Distress

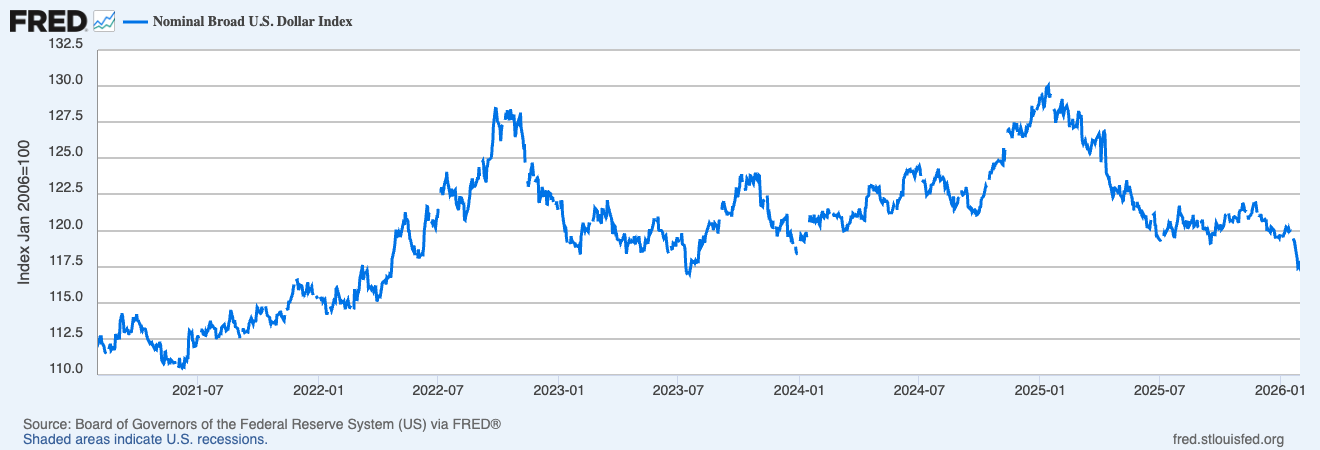

The trade-weighted U.S. dollar remains elevated relative to long-term norms, though it has moderated in recent months. While this continues to weigh on international purchasing power, it modestly favors U.S.-based buyers whose capital and income are dollar-denominated. Importantly, it has not translated into market stress in Manhattan or Brooklyn, reinforcing a normalization phase defined by selective demand, pricing discipline, and balanced leverage.

Domestic investors, by contrast, remain cautious. With investment mortgage rates hovering around 6.3% and stabilized rental yields in the 3–4% range, risk-adjusted returns for traditional condo and co-op investments are currently uninspiring. As a result, capital deployment is increasingly disciplined and underwriting-driven rather than momentum-based.

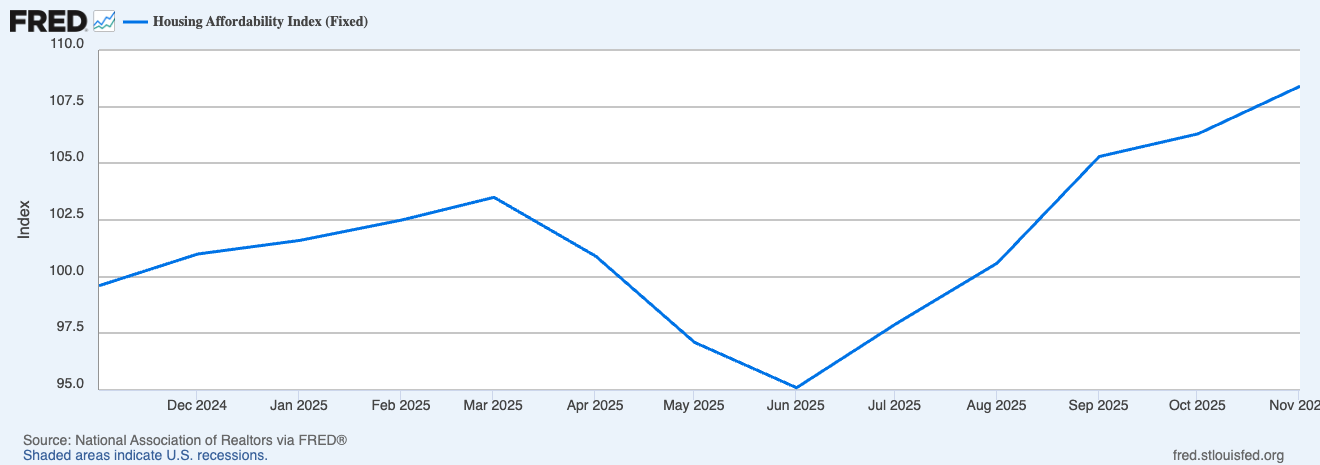

The chart below shows affordability bottoming in mid-2025 and improving into late 2025, meaning buyers can afford slightly more today - an effect felt more in Brooklyn than in Manhattan, where high prices still dominate affordability.

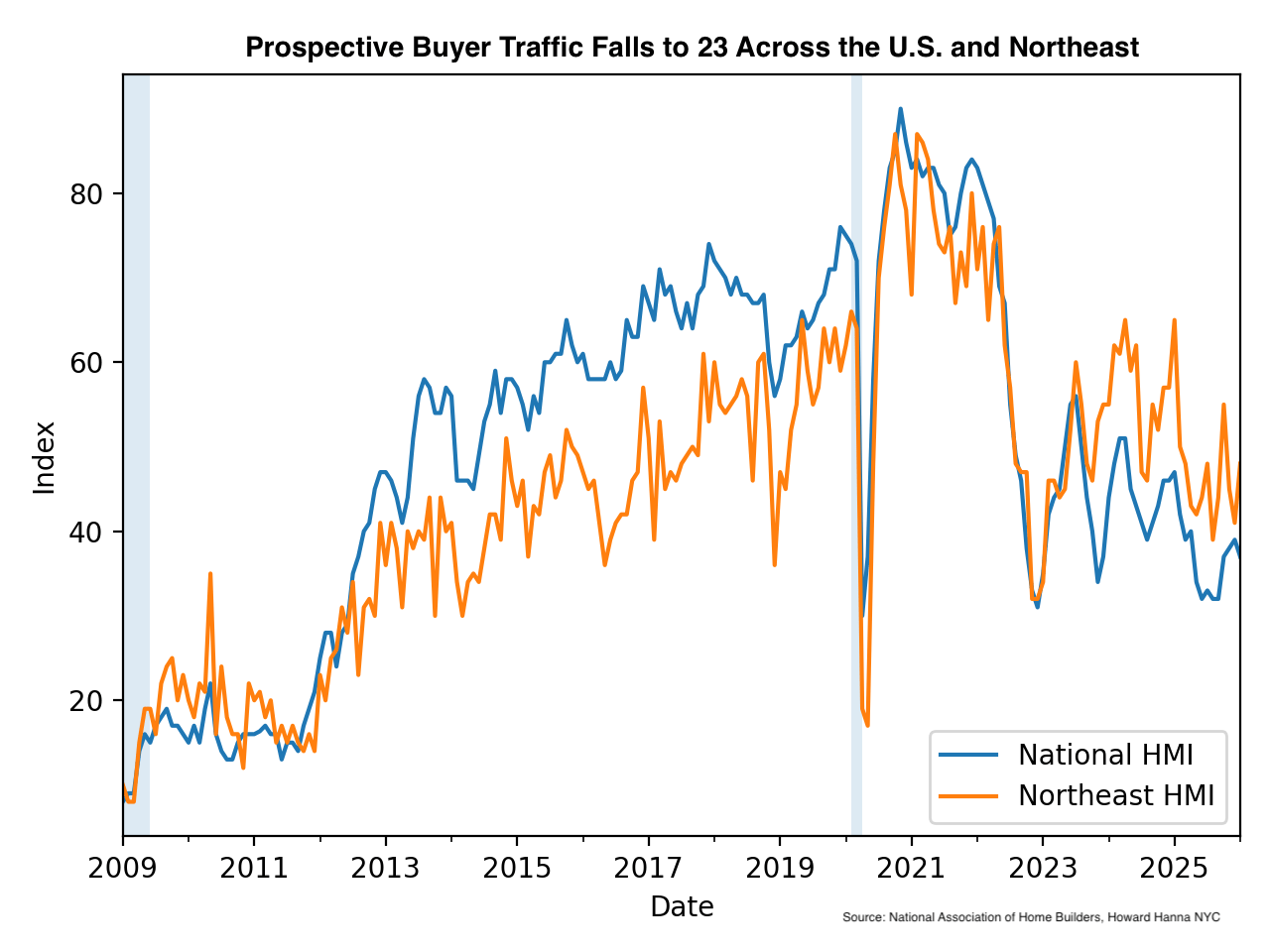

National and regional indicators reinforce this cooling but orderly backdrop. The NAHB/Wells Fargo Housing Market Index declined to 37 in January, reflecting weaker builder sentiment amid elevated rates. Subcomponents also softened, with:

-

current sales conditions at 41

-

six-month sales expectations at 49

-

and prospective buyer traffic falling to 23.

These readings signal pressure on new development activity rather than systemic housing stress.

Importantly, while national and Northeast builder sentiment has weakened, Brooklyn’s transaction-based leverage metrics reflects price discovery, not systemic imbalance.

Unlike prior downturns driven by excess leverage or credit dislocation, today’s environment is defined by affordability constraints and higher capital costs. This is a fundamentally different risk profile and one that supports the view of normalization rather than distress.

Key Insight: Higher rates and a strong dollar are filtering demand, not breaking it. Capital is patient, pricing discipline is intact, and market balance remains largely stable.

Outlook: Absent a material macro shock or sharp rate move, investor activity is likely to remain selective through early 2026, with renewed interest skewed toward well-priced assets, income durability, and long-term hold strategies.

References

1. Data courtesy of UrbanDigs

2. According to the Howard Hanna NYC Brooklyn Leverage Index

3. Data courtesy of Miller Samuel, Inc.

4. Data courtesy of Federal Reserve Bank of St. Louis

5. JUMBO mortgage rate APR data courtesy of Bank of America, Chase, and Wells Fargo

6. Cover Photo by Rihards Gederts - Howard Hanna NYC.

If you would like to chat about the most recent market activity,

feel free to contact us at [email protected] or

connect with one of our Advisors.

About Us

Howard Hanna NYC brings the nation’s largest independent and family-owned brokerage to New York City, uniting the strength of a national network with the insight and sophistication of a local firm. Formed through joining forces with Elegran Real Estate, Howard Hanna NYC delivers a seamless, full-service experience backed by more than 15,000 agents across 500 offices in 14 states. The firm’s forward-thinking, agent-first culture continues to shape the future of real estate across Manhattan and the Tri-State area.

Learn more at www.howardhannanyc.com.