Resale Rebounds

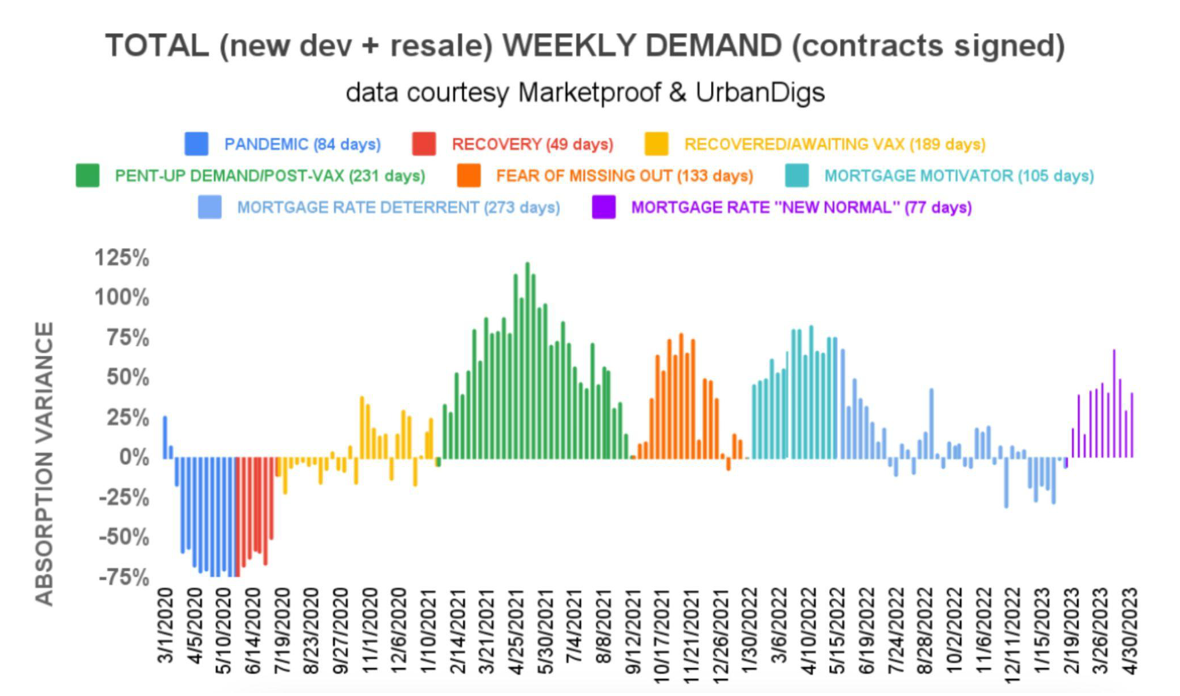

Demand rebounded this week after softening last week in response to the religious and academic holidays. It was, however, bifurcated across the primary (new development) and secondary (resale) markets, with the latter reporting stronger performance. That being said, new development demand this week — as measured by contracts signed — is still on par with its pre-pandemic benchmark.*

Chart Courtesy of UrbanDigs

Also, we’ve updated the bar chart above. The run in mortgage rates, which began in Q1-2022, is now divided into three distinct categories: “MOTIVATOR,” “DETERRENT,” and “NEW NORMAL.”

* The period is January 5, 2015, to March 1, 2020.

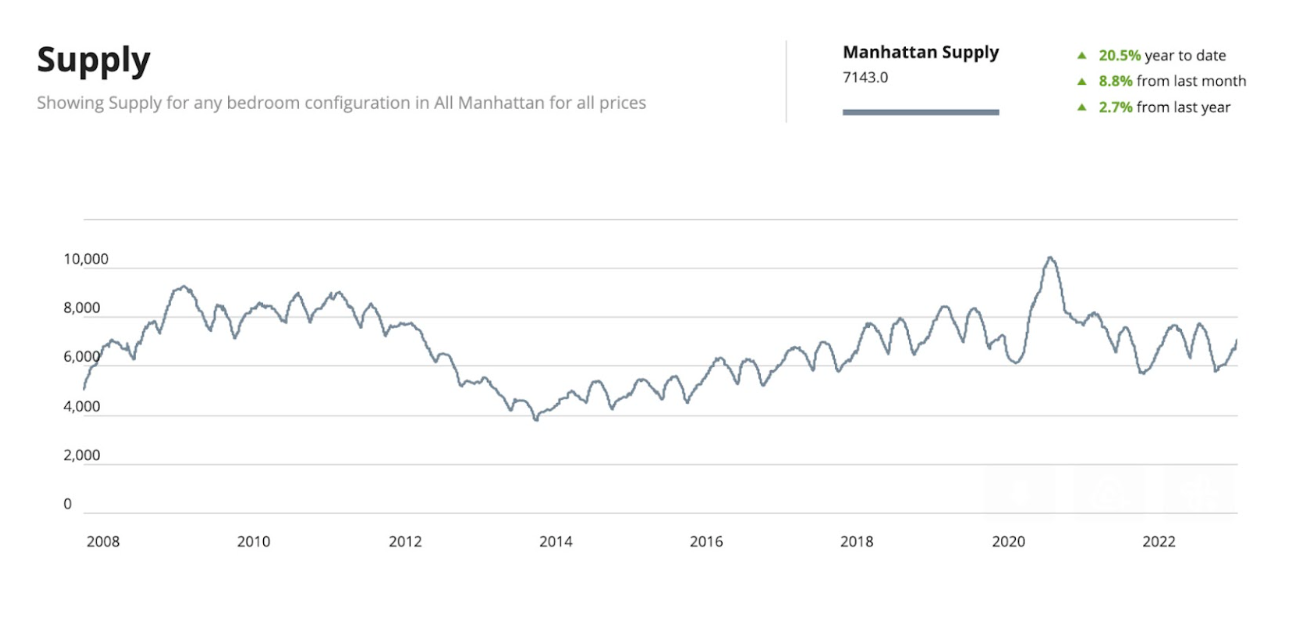

Manhattan Supply

The chart below serves as an almanac, and this year is shaping up just like years past. This week, supply increased from 6,938 to 7,143 units, and that number should continue to increase en route to the June peak.

Chart Courtesy of UrbanDigs

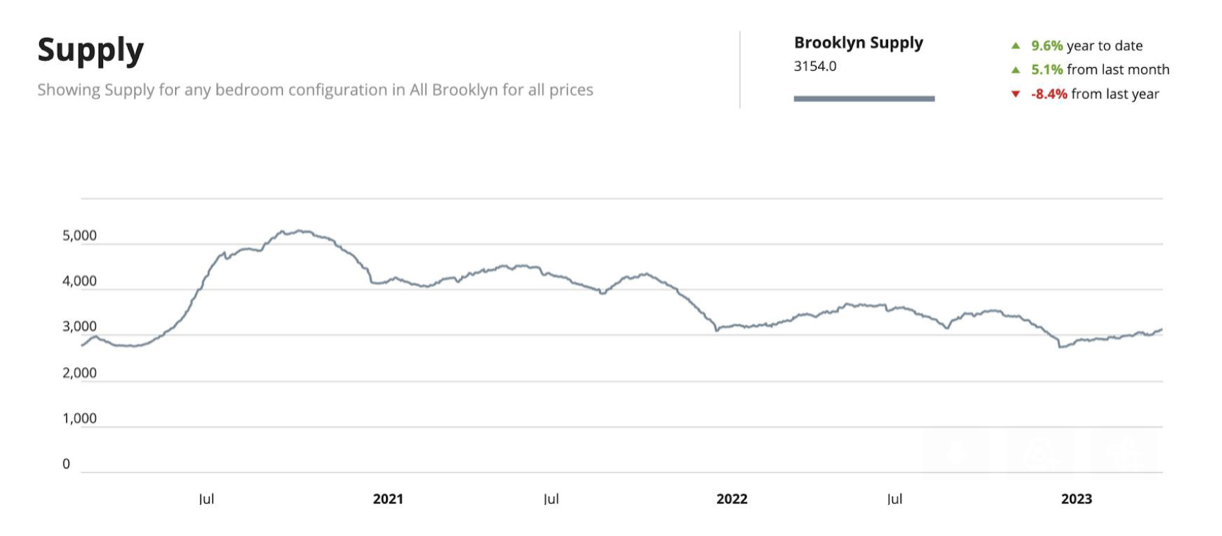

Brooklyn Supply

Exhibits a bi-annual cycle, although it’s not as apparent without Manhattan’s depth of historical data to clearly illustrate the trend. This week, supply in Brooklyn increased from 3,085 to 3,154 units, and that number should continue to increase as we head toward the June peak.

Chart Courtesy of UrbanDigs

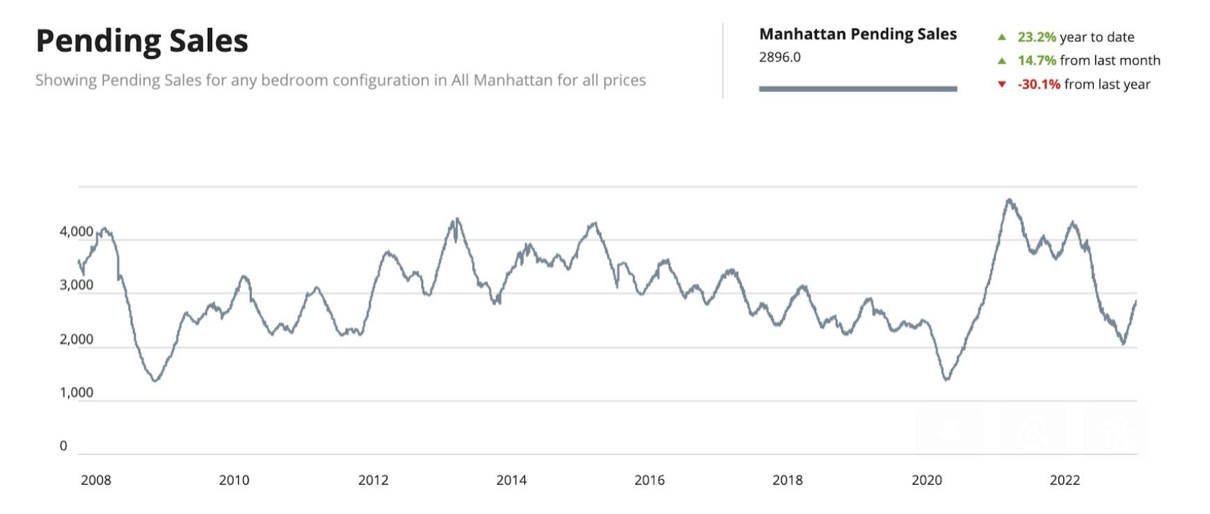

Manhattan Pending Sales

Like the supply “almanac,” the historical pending sales chart gives us a clear picture of what to expect. Any deviation from the large peak in June and the smaller peak in December would certainly qualify as “news” and be reported. As expected, the metric increased week over week from 2,825 to 2,896 units as the borough headed toward its first peak.

Chart Courtesy of UrbanDigs

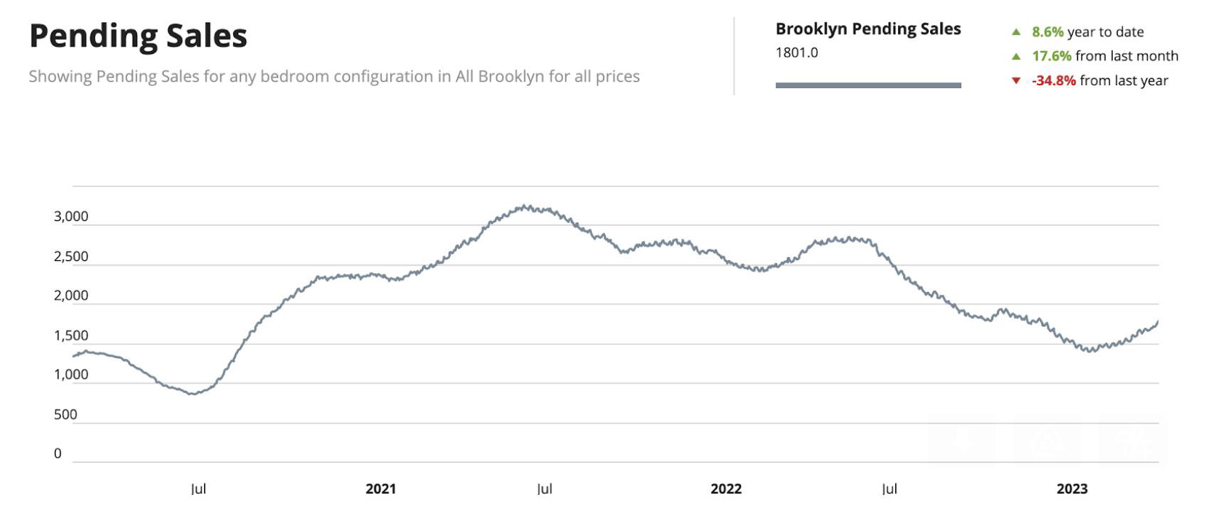

Brooklyn Pending Sales

This week’s observation is the same as what we witnessed in Manhattan where, right on cue, the metric reached its seasonal February trough and then reversed direction. We can also predict that the first of two peaks this year should occur in June and that the metric is about halfway there. This week, pending sales increased from 1,700 to 1,801 units.

Chart Courtesy of UrbanDigs

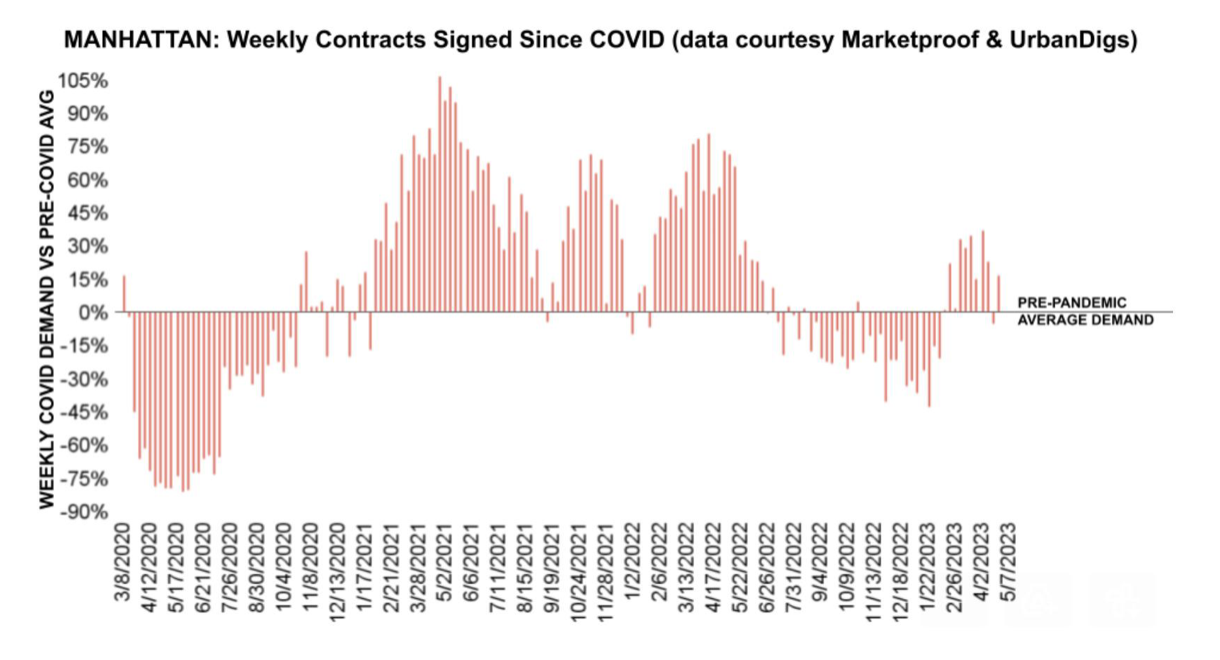

Manhattan Contracts Signed

After a brief relapse last week to below its pre-pandemic benchmark (the average weekly number of signed contracts from Jan 5, 2015, to Mar 1, 2020), the metric rebounded this week with 231 contracts signed.

Chart Courtesy of UrbanDigs

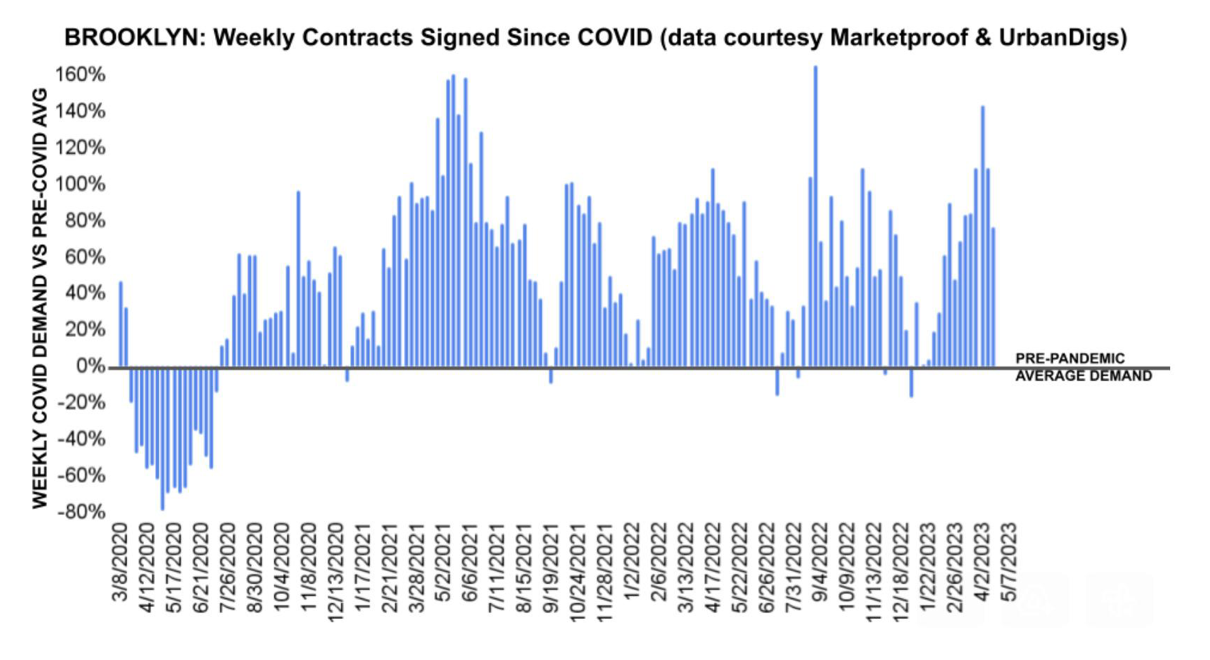

Brooklyn Contracts Signed

Brooklyn is peaking again since the pandemic. After briefly touching the pre-pandemic average (the average weekly number of signed contracts from January 5, 2015, to March 1, 2020) in mid-January, which has become the metric’s support level for the past two years, signed contracts have skyrocketed above that average. This week, 159 contracts were signed.

Chart Courtesy of UrbanDigs

New Development Insights

As reported by Marketproof, 54 new development contracts were reported across 44 buildings this week. The following were the top-selling new developments of the week:

- THE CORTLAND (West Chelsea)

- 300 WEST 30 STREET (Chelsea)

- 450 WASHINGTON (Tribeca)

- 611 W 56TH ST (Clinton)

- 1064 HANCOCK ST (Bushwick)

- NOVA (Long Island City)