Overall Manhattan Market Update: April 2024

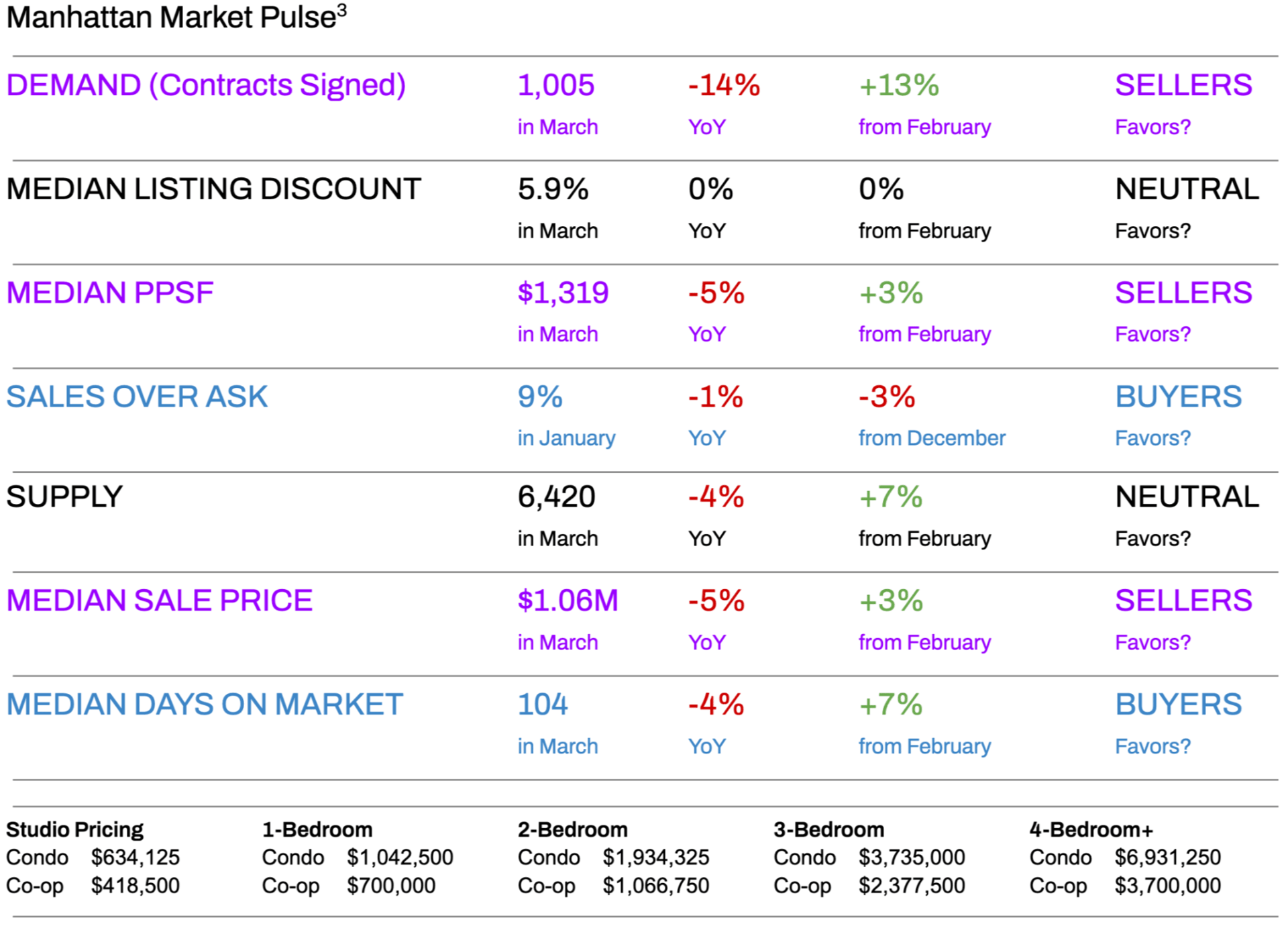

Demand Rises MoM, Falls YoY, and Continues to Outpace Supply

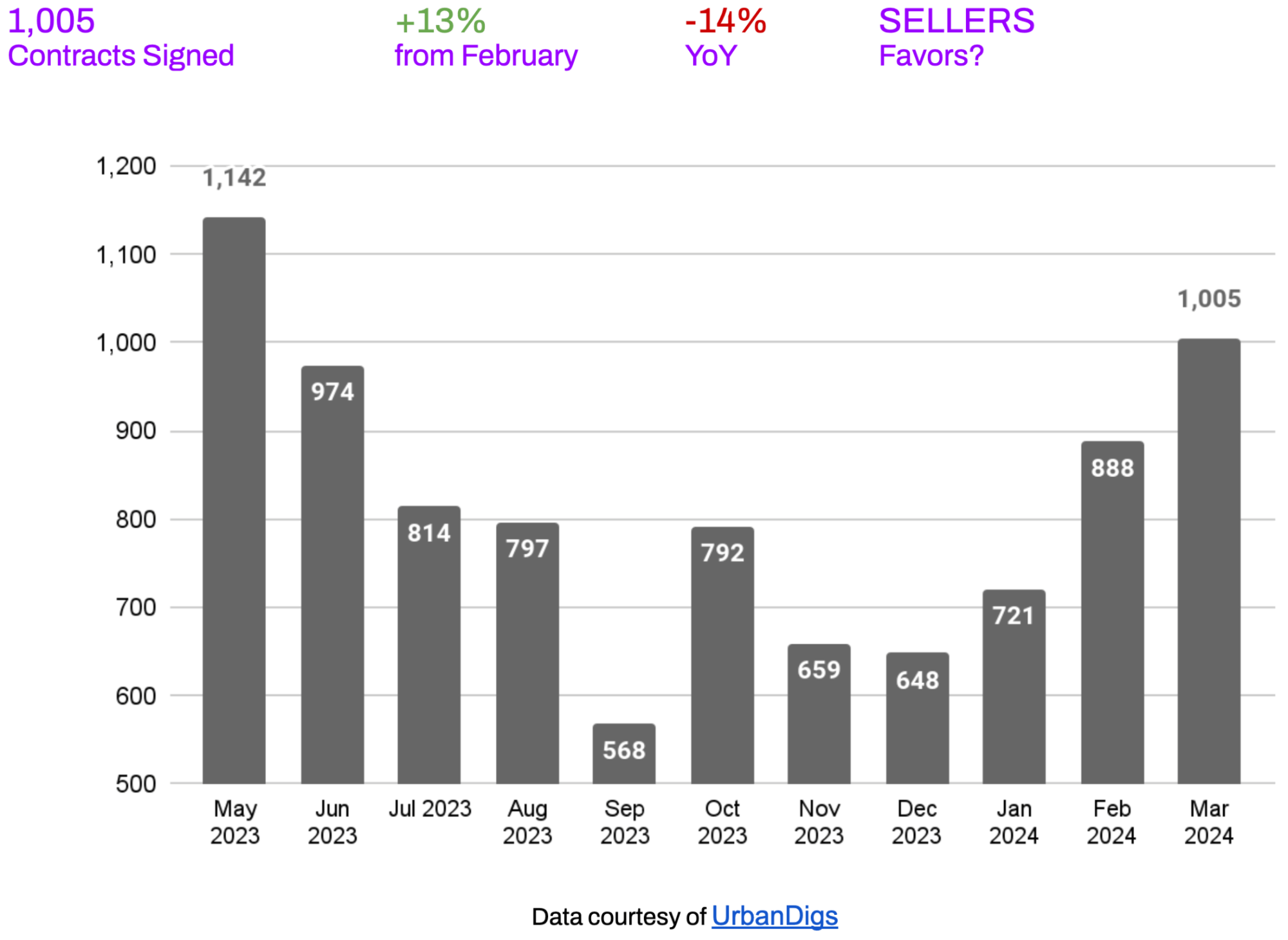

Despite dashed and delayed Fed rate cut expectations and rising interest rates, contract activity in Manhattan increased by 13% in March compared to February. However, it declined by 14% compared to last year.

The luxury market maintains its momentum, outperforming the overall market in terms of velocity and price action. Notably, the share of all-cash purchases has steadily risen, approaching 70% of total transactions.

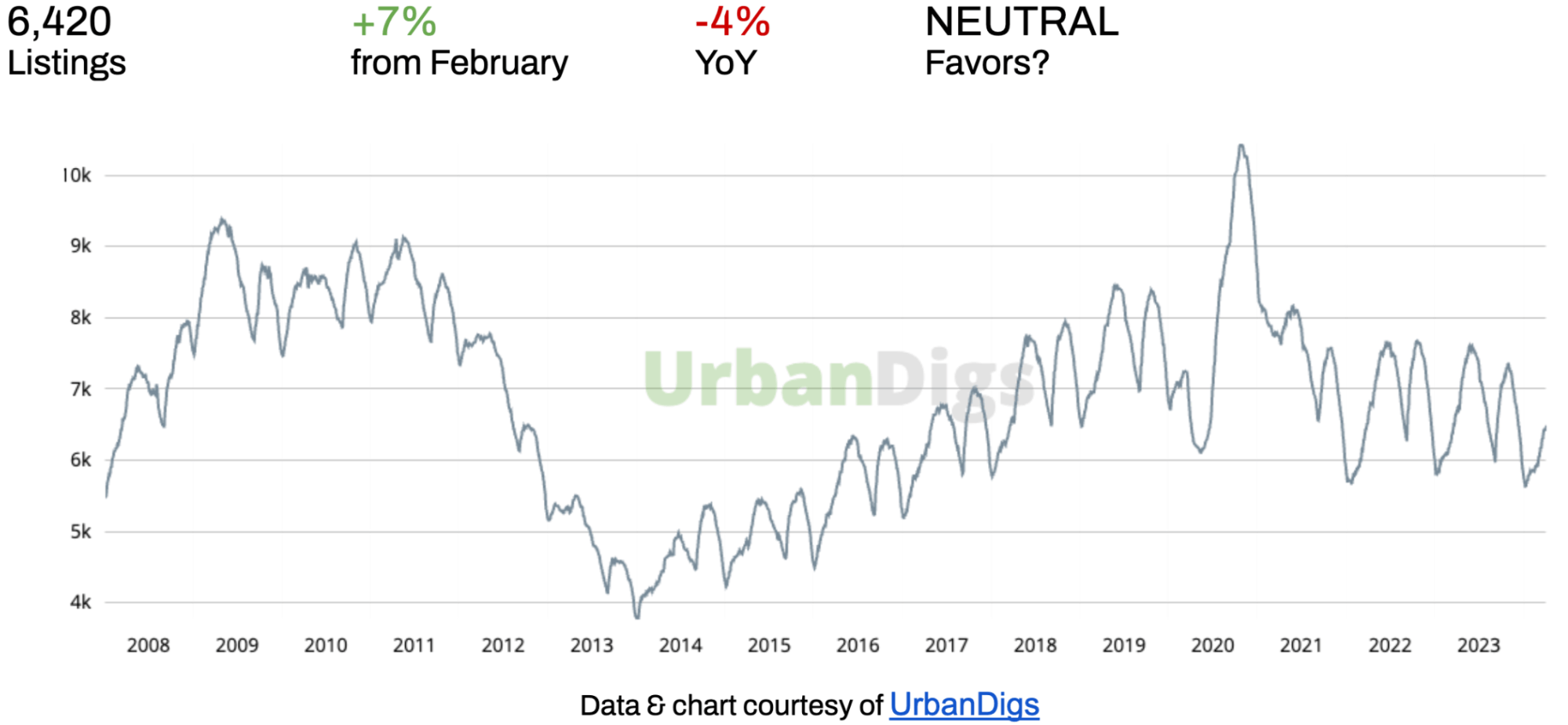

As seasonally expected, supply increased by 7% in March but remained 4% lower than last year. This recent imbalance between supply and demand has fostered a competitive market environment. Signs of stabilization are emerging, with a potential price floor forming in median price per square foot, while a ceiling may also be developing in median listing discounts.

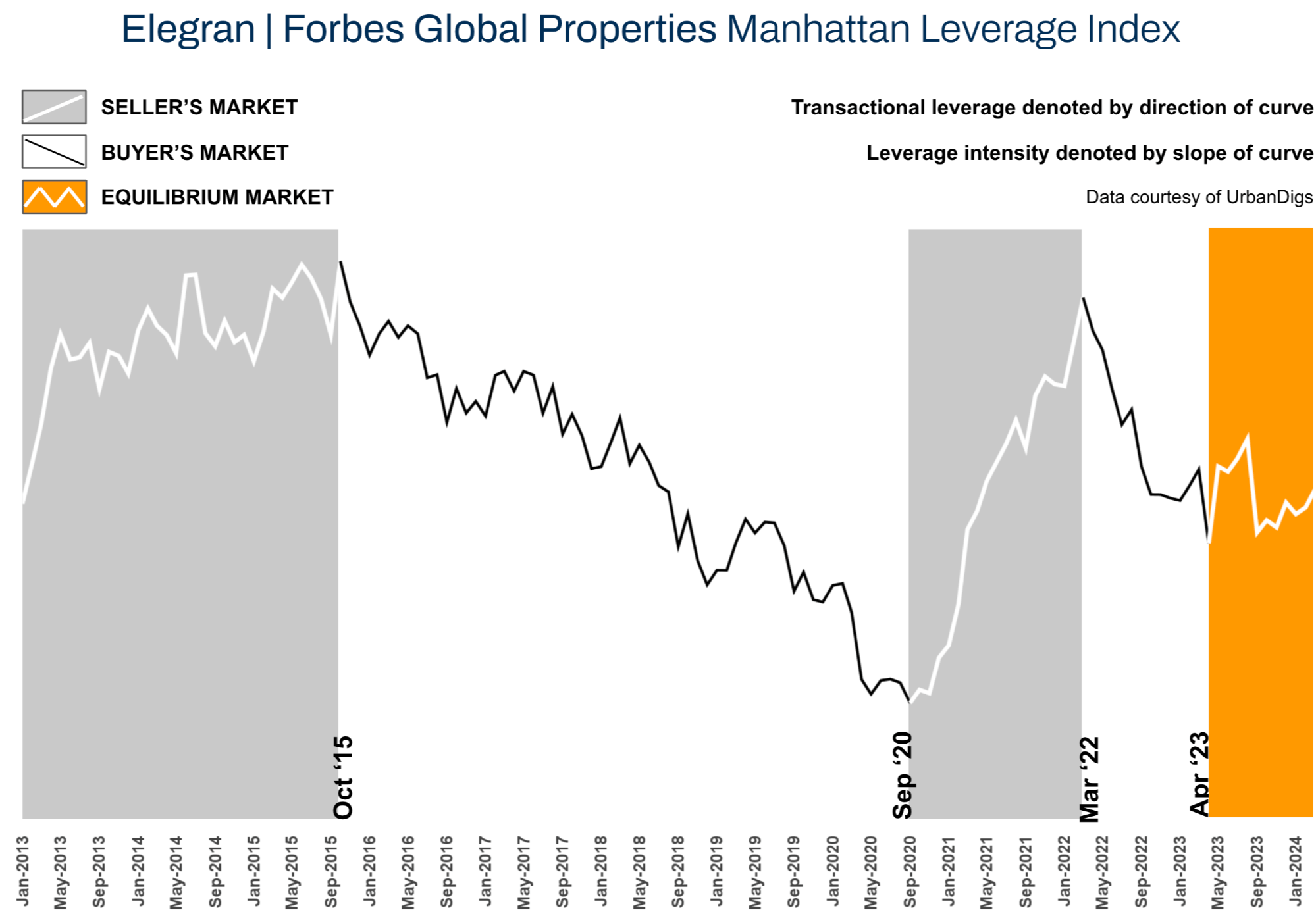

The Elegran | Forbes Global Properties Manhattan Leverage Index indicates a neutral and balanced market with leverage slightly favoring sellers as demand outpaces supply.

Sales

- “Neutral” markets don’t exist because buyers and sellers are constantly playing tug-of-war for leverage

- At times (e.g., the past 11 months), there’s no clear winner as buyers & sellers reach equilibrium.1

- Based on the data, it’s a neutral market, and sellers gained a small advantage in March.

- Demand (measured by contracts signed) increased in the seller’s favor.

- The median listing discount was unchanged compared to February.

- Median PPSF (Price Per Square Foot) increased in the seller’s favor.

- Supply increased compared to the previous month in the buyer’s favor, but YoY remains lower in the seller’s favor.

- Demand (measured by contracts signed) increased in the seller’s favor.

- At times (e.g., the past 11 months), there’s no clear winner as buyers & sellers reach equilibrium.1

Rentals

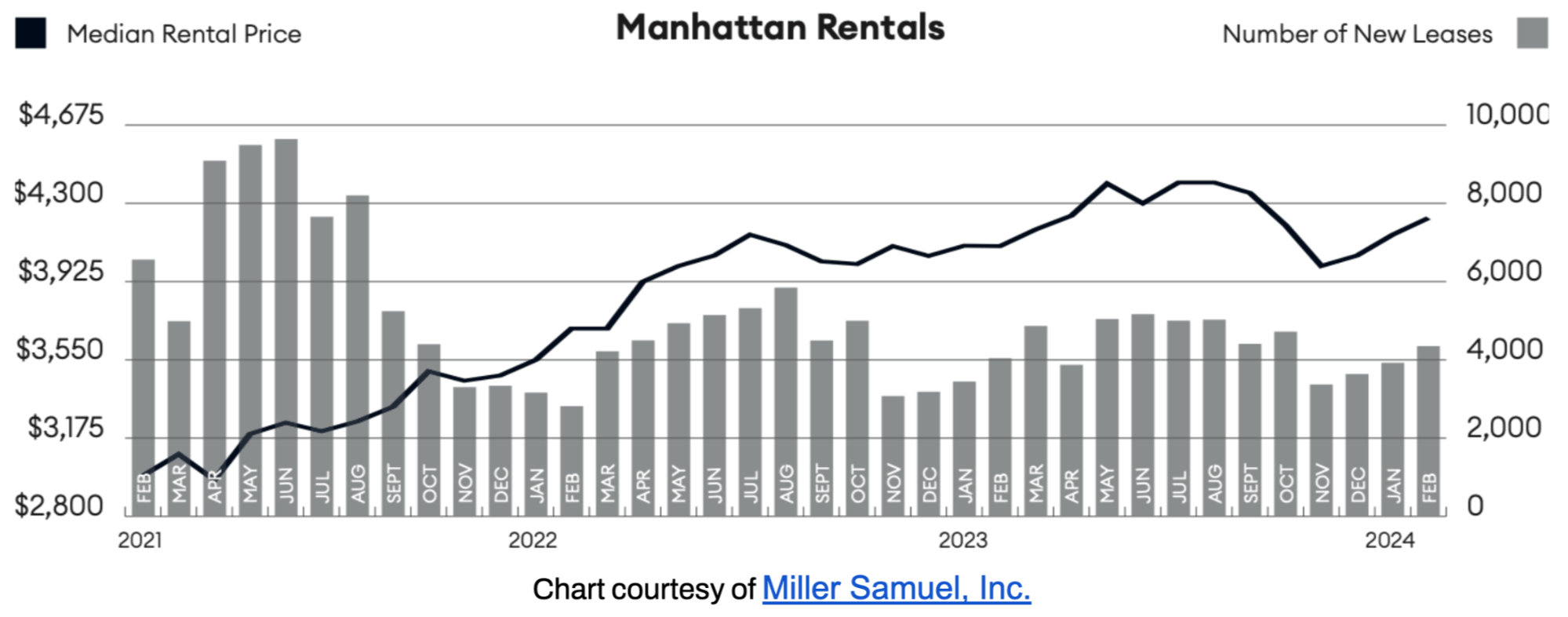

- From the all-time high of $4,300 in May & July 2023, the median rental price has declined to $4,194.

- While median prices remain lower than peaks in 2023, they've increased from this past winter, and with spring approaching, we anticipate further rent increases in both April and May.

Investments

- Total return is generated by net rental income & price appreciation.

- All-cash buyers can expect a cap rate between 2.7% and 3.2%.

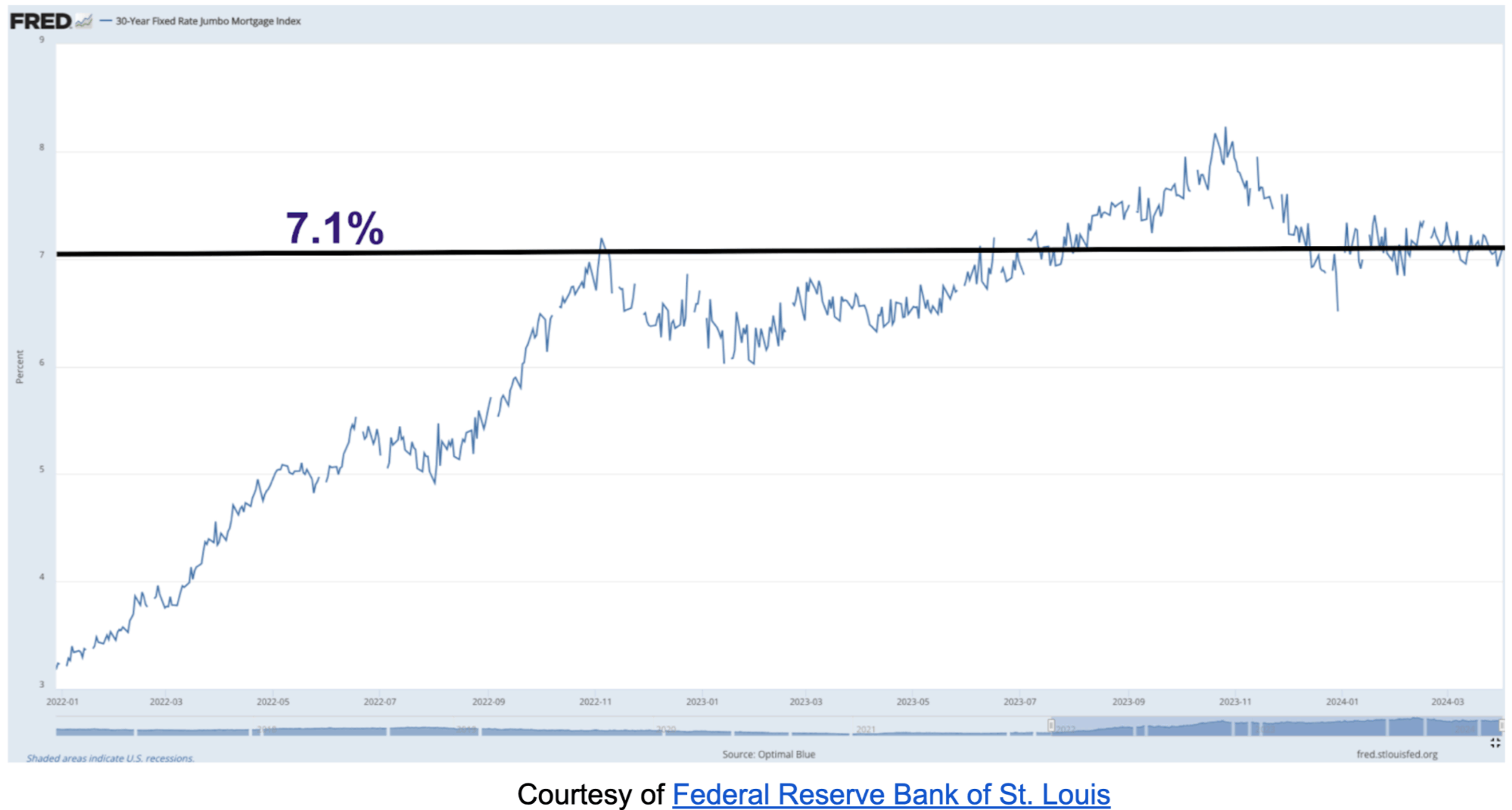

- Since the average JUMBO mortgage rate APR is 6.76%2, there is no net rental income on leveraged purchases.

- All-cash buyers can expect a cap rate between 2.7% and 3.2%.

Elegran | Forbes Global Properties Manhattan Leverage Index

The Elegran | Forbes Global Properties Manhattan Leverage Index is powered by four indicators: supply, demand, median price per square foot (PPSF), and median listing discount.

It informs us whether the current is a buyer’s or a seller’s market, i.e., which party possesses transactional leverage. Looking at the graph below, this is indicated by the direction of the curve, where:

- An increasing trend from left to right indicates a seller’s market

- A decreasing trend from left to right indicates a buyer’s market

Our indicator also informs us regarding the relative strength of that leverage, indicated by the slope of the curve, where:

- A gentle slope indicates a weak advantage by one party over the other

- A sharp slope indicates a strong advantage

But the numbers are not important. What is important is the direction and slope of the curve. For the last few months, there has been a stalemate between buyers and sellers in a relatively balanced market. Sellers gained a slight edge as demand rose faster than supply. This trend will likely continue in the coming months, with leverage increasingly favoring sellers as demand outpaces supply.

Manhattan Supply

Manhattan supply has followed a similar cadence—pandemic excluded—for the past decade, as the chart above clarifies. Supply increased by 7% in March compared to February, tracking seasonal trends, but it remains 4% lower than last year.

What This Means for:

- BUYERS: Available inventory has increased compared to previous months, providing more choice, but overall inventory levels are still lower than last year.

- SELLERS: More inventory means more competition among sellers for buyers, but sellers who price their homes appropriately maintain a slight advantage as demand outpaces supply.

Anticipate a steady increase in supply through May, providing buyers with more options.

Manhattan Demand

Contracts signed saw a notable 13% increase from February to March, indicating an acceleration in demand for the spring market. However, equally as notable, in contrast to January and February, where demand surpassed the previous year, this March witnessed a 14% decline in signed contracts compared to the same period last year.

What This Means for:

- BUYERS: More competition.

- SELLERS: More activity.

Overall, contract volumes should continue to increase over the next few months as the traditionally busy spring listing season is underway. As demand continues to rise faster than supply, the market feels more competitive, and leverage is tilting in favor of sellers.

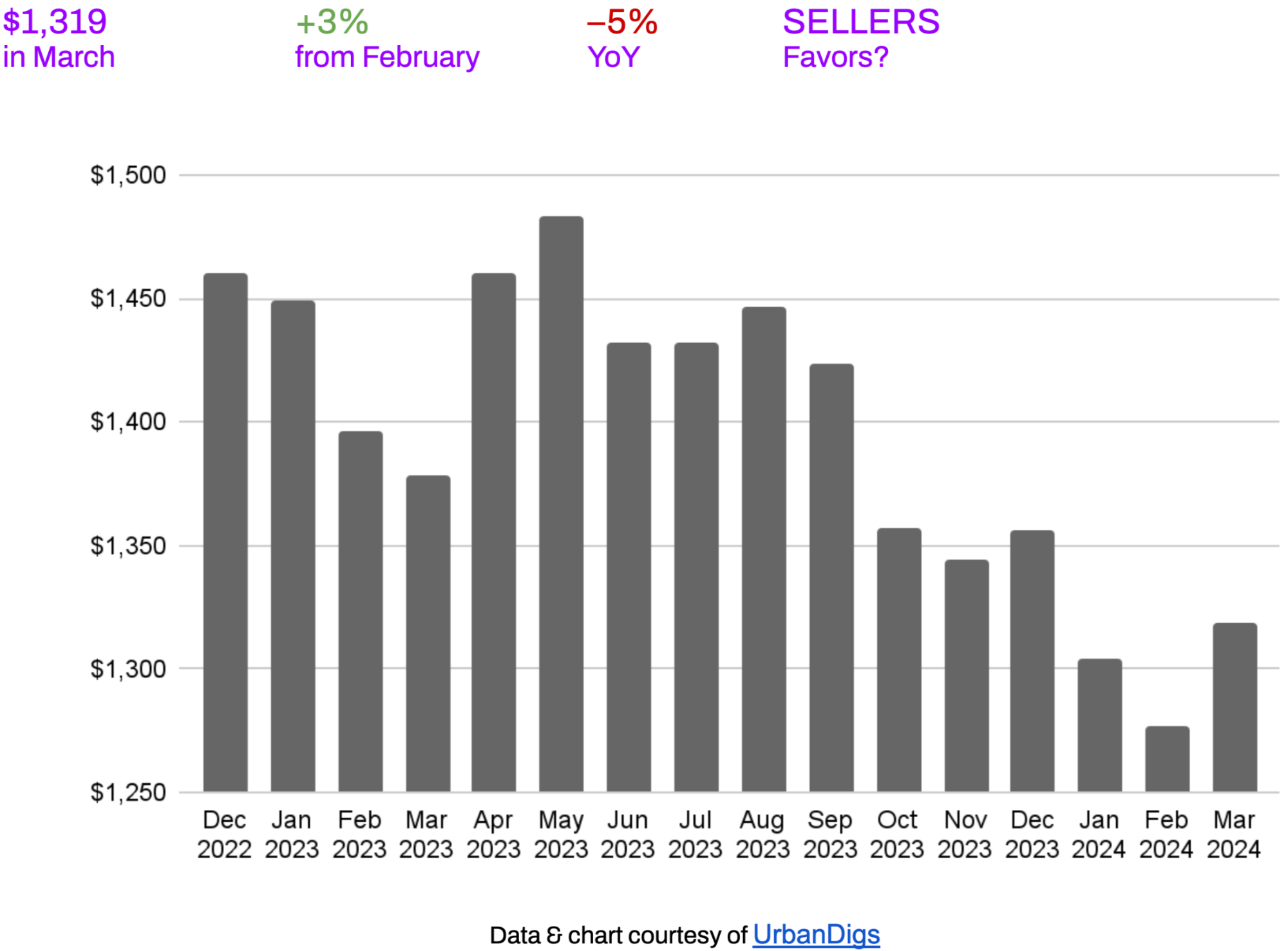

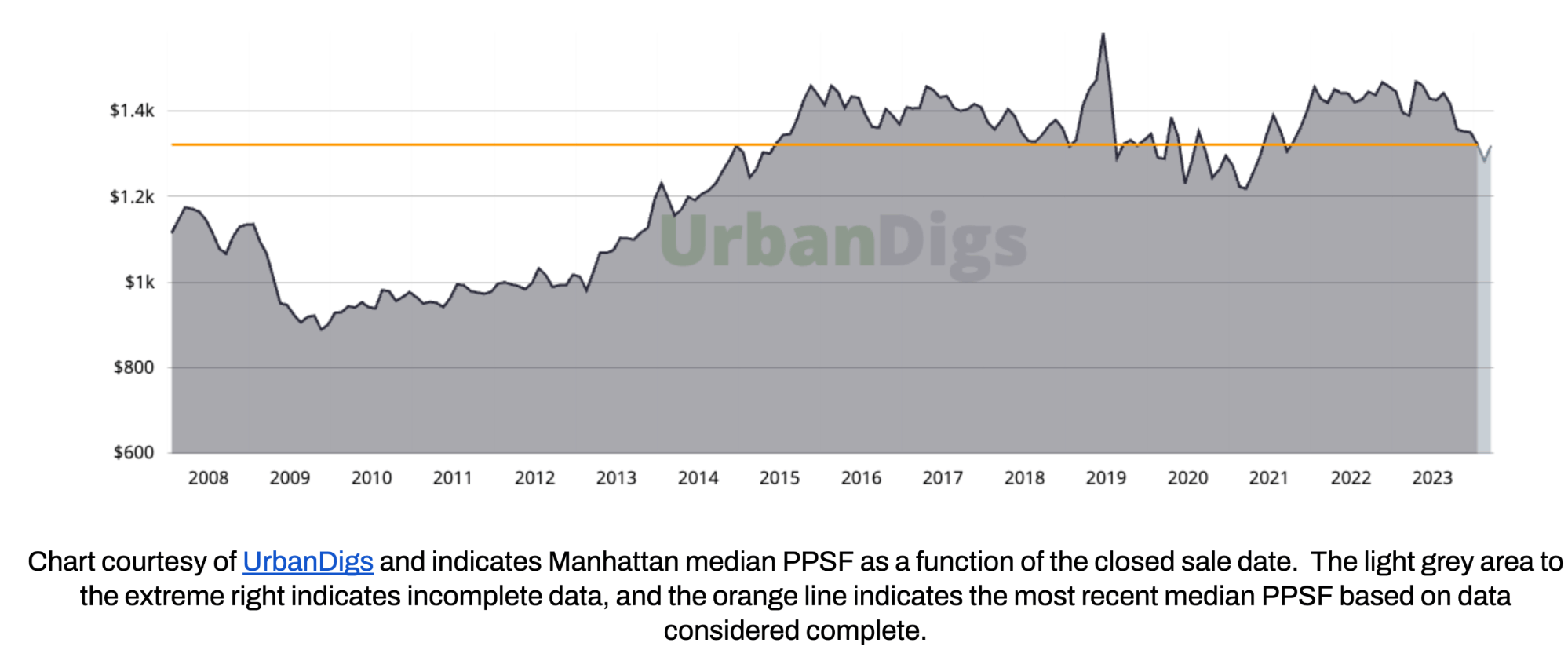

Manhattan Median PPSF

Following a low point in February, the median price per square foot (PPSF) has rebounded, showing a 3% increase compared to last month. This suggests a market shift that could benefit sellers.

What This Means for:

- BUYERS: Prices are moving against their interests.

- SELLERS: Prices are moving in their interests.

Keep a close eye on this metric in the upcoming months. Anticipate a stabilization indicating a bottom has formed, laying the groundwork for price upticks in the latter half of 2024.

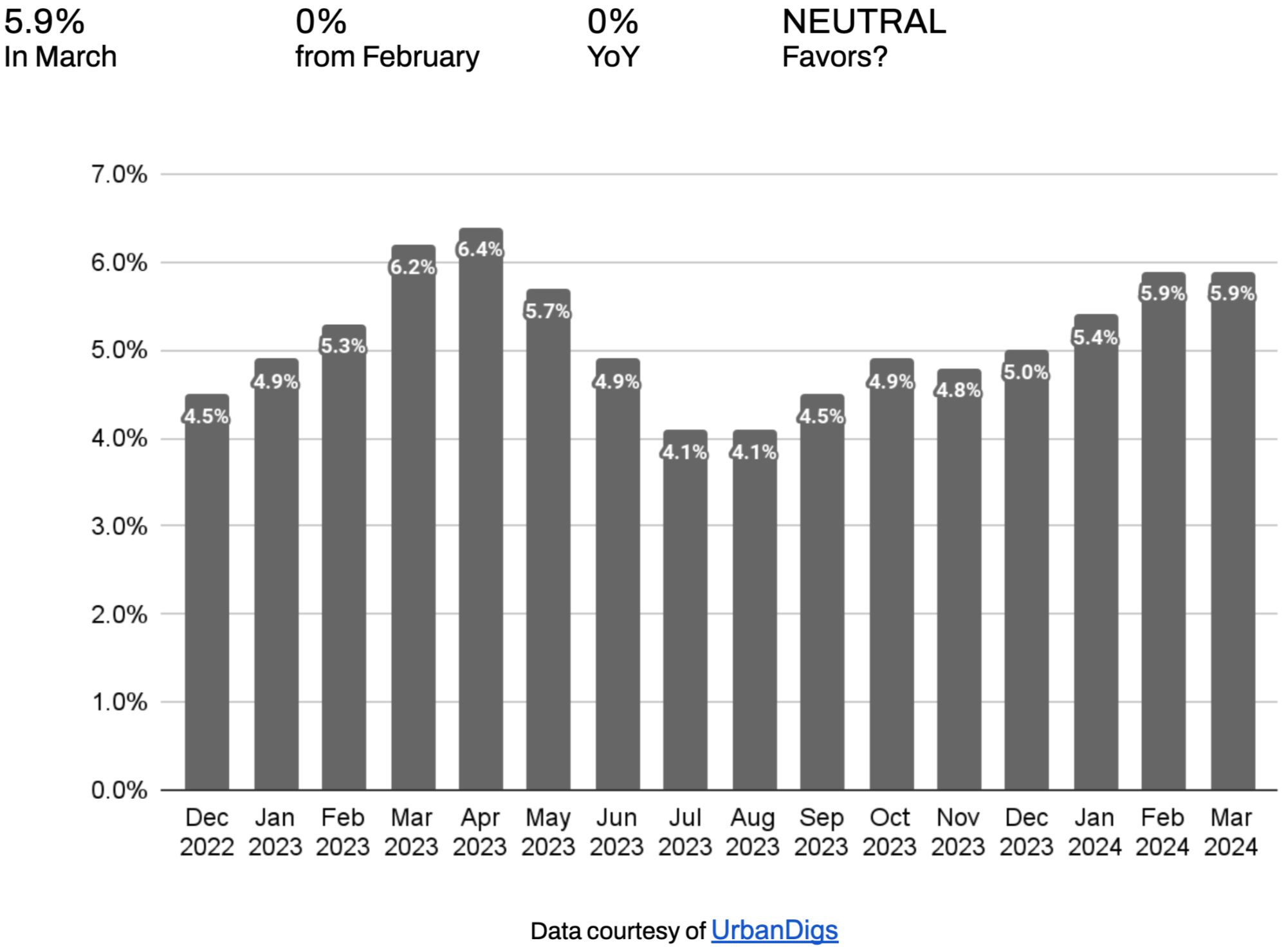

Manhattan Median Listing Discount

The median listing discount in March has remained the same compared to February, indicating a potential peak in listing discounts.

What This Means for:

- BUYERS: Despite the listing discount remaining unchanged from February, buyers face a slightly more challenging environment due to heightened competition. We may have reached the peak in listing discounts for this cycle.

- SELLERS: In general, sellers hold a slight advantage over buyers this month, and the listing discount may be peaking.

Monitor this metric in the coming months, and look for a ceiling to be established, followed by a decrease in the median listing discount. Declining discounts typically foreshadow rising prices.

Rental Remarks

In February4, the median rent in Manhattan increased by 2.4% and remained near record highs, and is poised to increase further heading into peak rental season this summer. The 30-Year Fixed Rate JUMBO Mortgage Index5 is trending at 7.1%, and the average JUMBO APR is 6.76%6. So, it’s a “catch-22” for renters, as the rent versus buy scale may feel equally punitive on both sides.

Investor Insights

The total return is driven by net rental income and capital appreciation. For all-cash investors, Manhattan cap rates are currently 2.7 - 3.2%. Unfortunately, there is no net income potential for those investors using a large percentage of leverage, with the average JUMBO mortgage APR at 6.76%. Timing and a strong USD may afford foreign investors, depending on their native currency, the opportunity to realize significant capital gains upon selling their assets.

References

- According to the Elegran | Forbes Global Properties Brooklyn Leverage Index

- JUMBO mortgage rate APR data courtesy of Bank of America, Chase, and Wells Fargo

- Data courtesy of UrbanDigs

- Data courtesy of Miller Samuel, Inc.

- Data courtesy of Federal Reserve Bank of St. Louis

- JUMBO mortgage rate APR data courtesy of Bank of America, Chase, and Wells Fargo