Spring 2026: A Steady Market Taking Shape

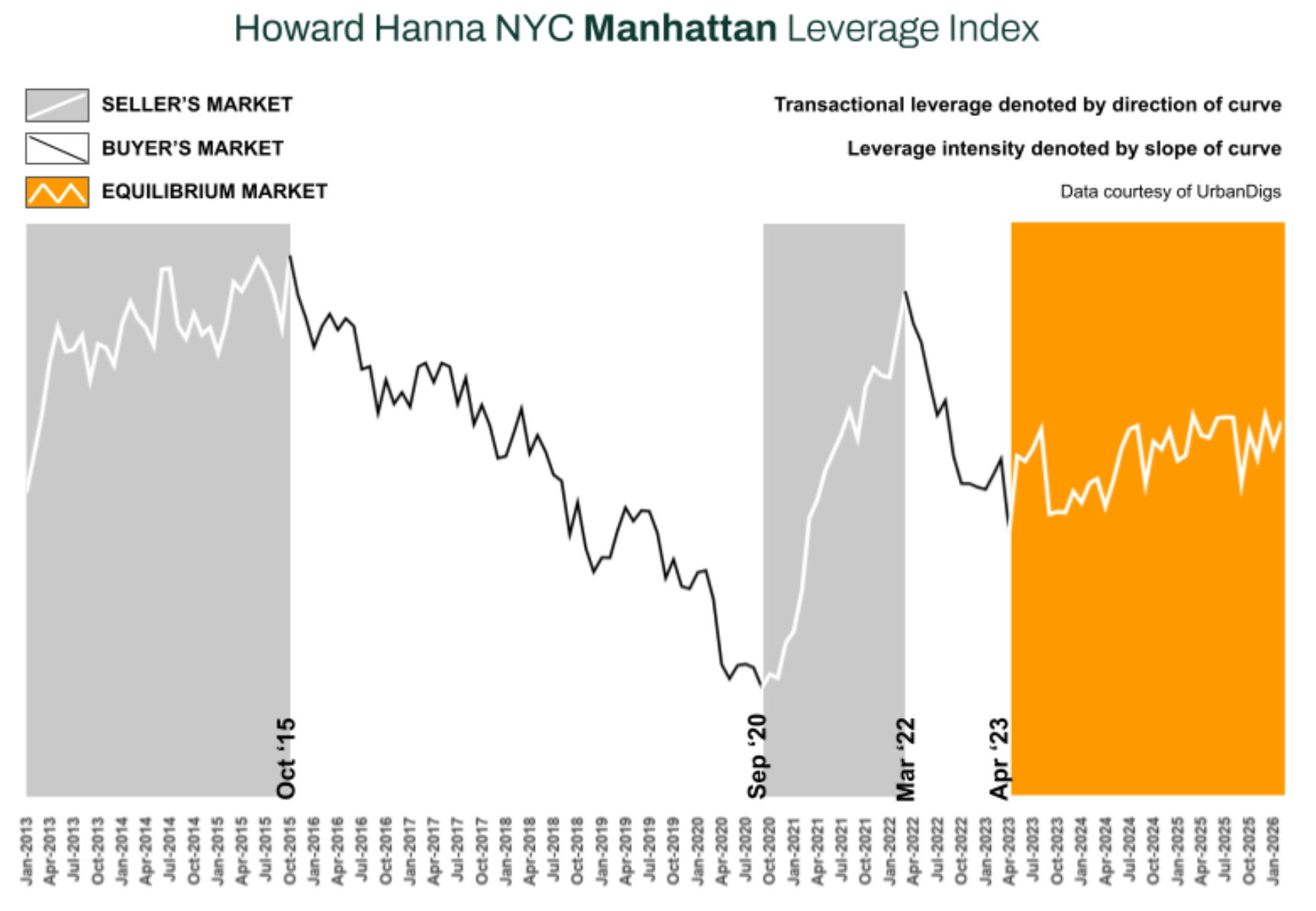

Manhattan entered spring with measured strength. The Howard Hanna NYC Manhattan Leverage Index² edged modestly higher in February and remains in seller-leaning territory. Inventory is still structurally constrained, buyer activity rebounded month-over-month, and pricing continues to hold — all against a backdrop of elevated but stabilizing mortgage rates. This is not a surge market. It is not a correction market. It is a disciplined, normalized market where execution matters more than timing.

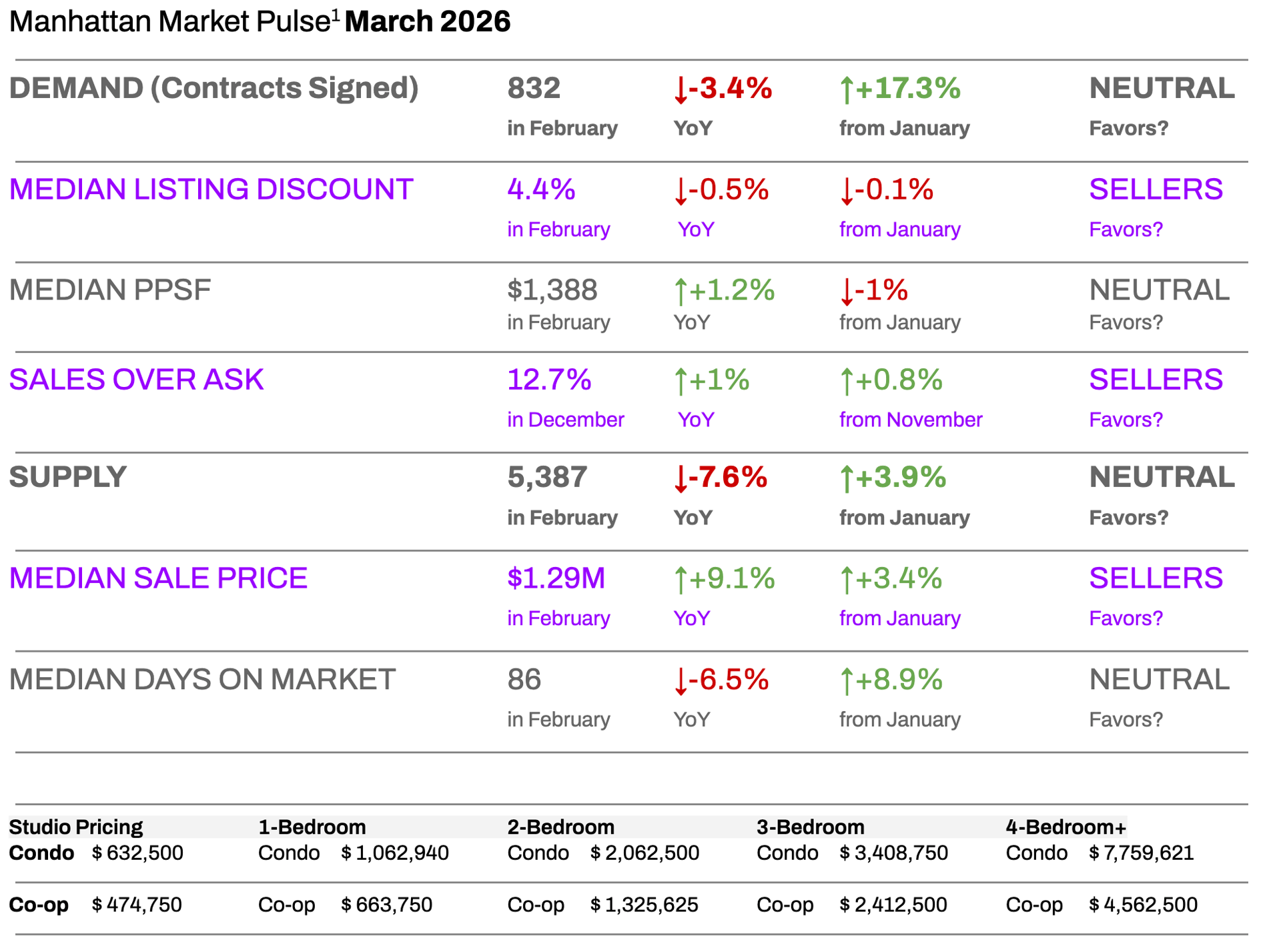

Market Snapshot: Four Numbers That Matter

-

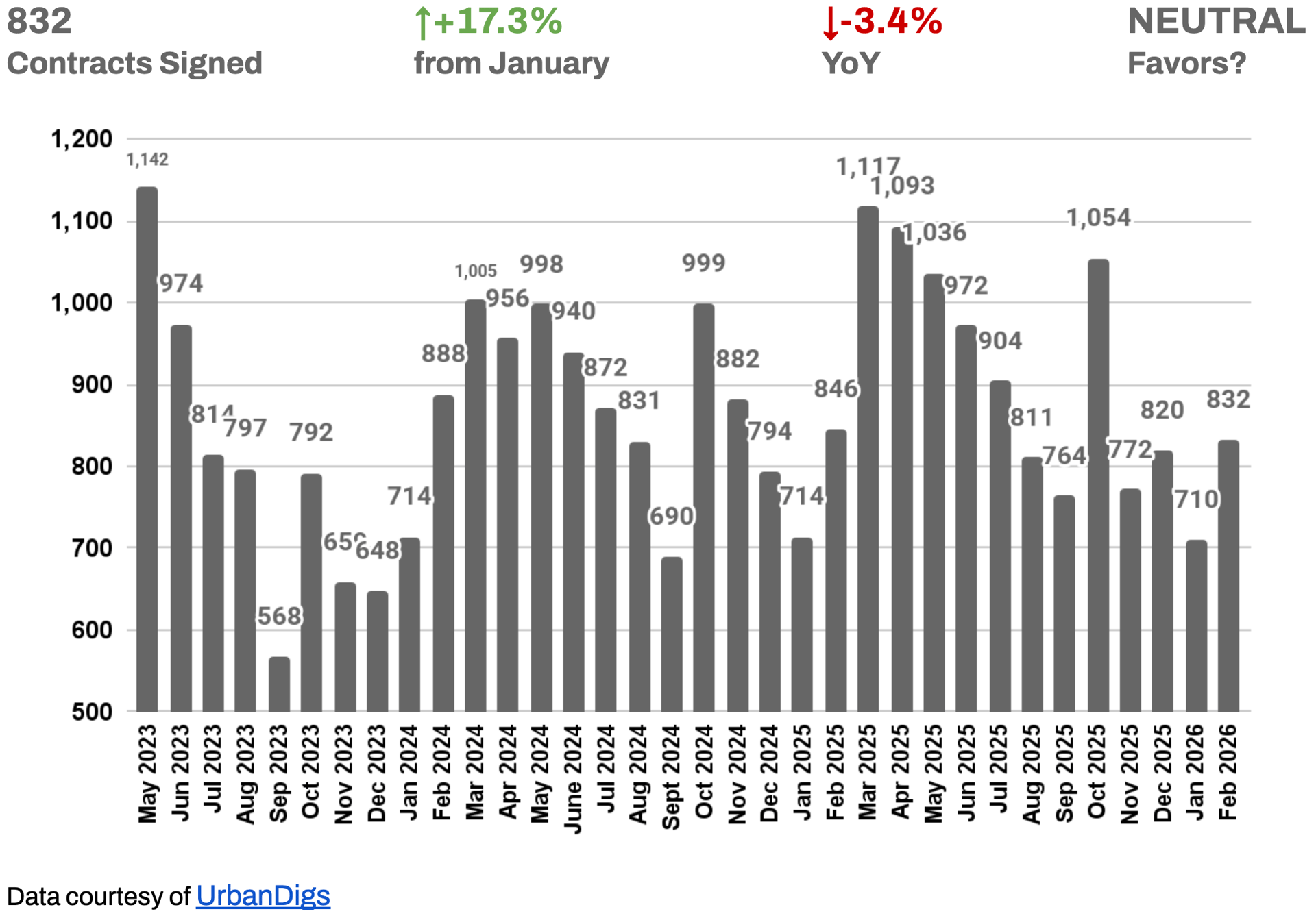

832 contracts signed in February — a 17.3% month-over-month rebound signaling early spring demand.

-

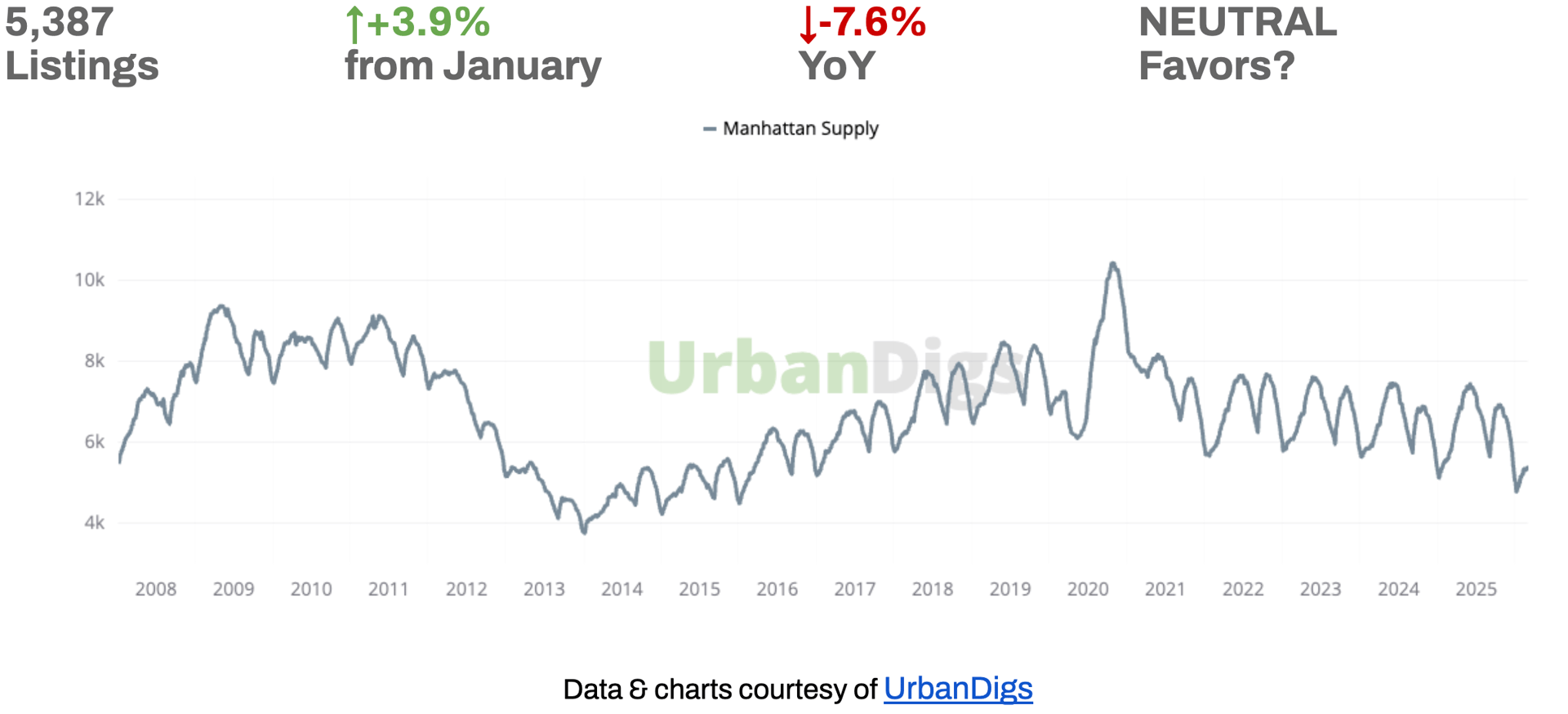

5,387 active listings — 7.6% below last year, reinforcing structural supply constraints.

-

Median Sale Price: $1.29M, up 9.1% YoY — this is your single most powerful pricing signal and it's not on the summary page at all

-

Sales Over Ask: 12.7% — tells buyers competition is real, and tells sellers the market rewards bold pricing

Key Takeaways

-

Supply remains tight at 5,387 listings, well below pre-pandemic norms.

-

Buyer activity rebounded sharply from January, though still 3.4% below February 2025.

-

Median PPSF held at $1,388, up 1.2% year-over-year.

-

Listing discounts tightened to 4.4%, near multi-year lows.

-

Mortgage rates stabilized near 6.1%, reducing volatility and transaction friction.

-

Manhattan median rent hit $4,695 in January, near record highs, making the buy vs. rent calculus increasingly relevant for long-term residents.

Outlook

Spring 2026 is shaping up as a seller-leaning market with nuance. Well-priced, move-in-ready listings are trading efficiently. Buyers with conviction and financing in place are finding selective opportunities, particularly in co-ops and value-oriented condos. A weakening U.S. dollar has made Manhattan real estate meaningfully more affordable for European and other international buyers — an underappreciated tailwind entering spring.

As inventory rises gradually through Q2, competition for quality listings is expected to increase.

Both buyers and sellers who act in the first eight weeks of spring are historically best positioned — and 2026 is no exception.

Photo by Rihards Gederts | Howard Hanna NYC

Howard Hanna NYC Manhattan Leverage Index

The Howard Hanna NYC Manhattan Leverage Index blends four key market signals – supply, demand, median PPSF, and median listing discount – to gauge the balance of power between buyers and sellers in Manhattan. It’s a proprietary index that distills these metrics into one indicator of market leverage. Direction Matters:

-

An upward-sloping curve = seller’s market

-

A downward-sloping curve = buyer’s market

The steeper the slope, the stronger the advantage for either side

In February 2026, the index edged modestly higher and remains in seller-leaning territory. Supply, demand, and pricing registered neutral readings with slight upward bias, while listing discounts clearly favored sellers.

From a historical perspective, this resembles mid-cycle normalization periods such as 2013–2015, when mortgage rates rose modestly but did not trigger broad market correction.

What’s different this cycle is structural undersupply. Manhattan inventory remains well below 2017–2019 averages, limiting the probability of distress-driven repricing.

Manhattan Supply

Inventory Rises Seasonally, But Remains Below Last Year

Active listings increased to 5,387 in February, up 3.9% from January, but still 7.6% below this time last year. As expected, more sellers are beginning to test the market ahead of spring. However, total supply remains well below pre-pandemic norms, which continues to limit downside pricing pressure.

🟦 Buyers: Selection is improving slightly, but overall inventory remains tight. Acting early in the spring cycle may reduce competition.

🟪 Sellers: Structural undersupply continues to work in your favor. Proper pricing from day one remains critical.

Outlook: Inventory should continue rising gradually through Q2, but meaningful oversupply is unlikely.

Manhattan Demand

Contracts Rebound as Spring Activity Begins

February saw 832 signed contracts, a 17.3% increase from January, though still 3.4% below February 2025. The month-over-month rebound confirms buyers are re-engaging as the spring market begins.

At 832 contracts, activity sits comfortably within mid-cycle norms and remains well above late-2023 lows.

🟦 Buyers: Momentum is building. Waiting for a dramatic shift in leverage may not be realistic.

🟪 Sellers: Demand recovery supports disciplined pricing strategies.

Outlook: Contract activity is expected to increase further as more spring inventory comes online.

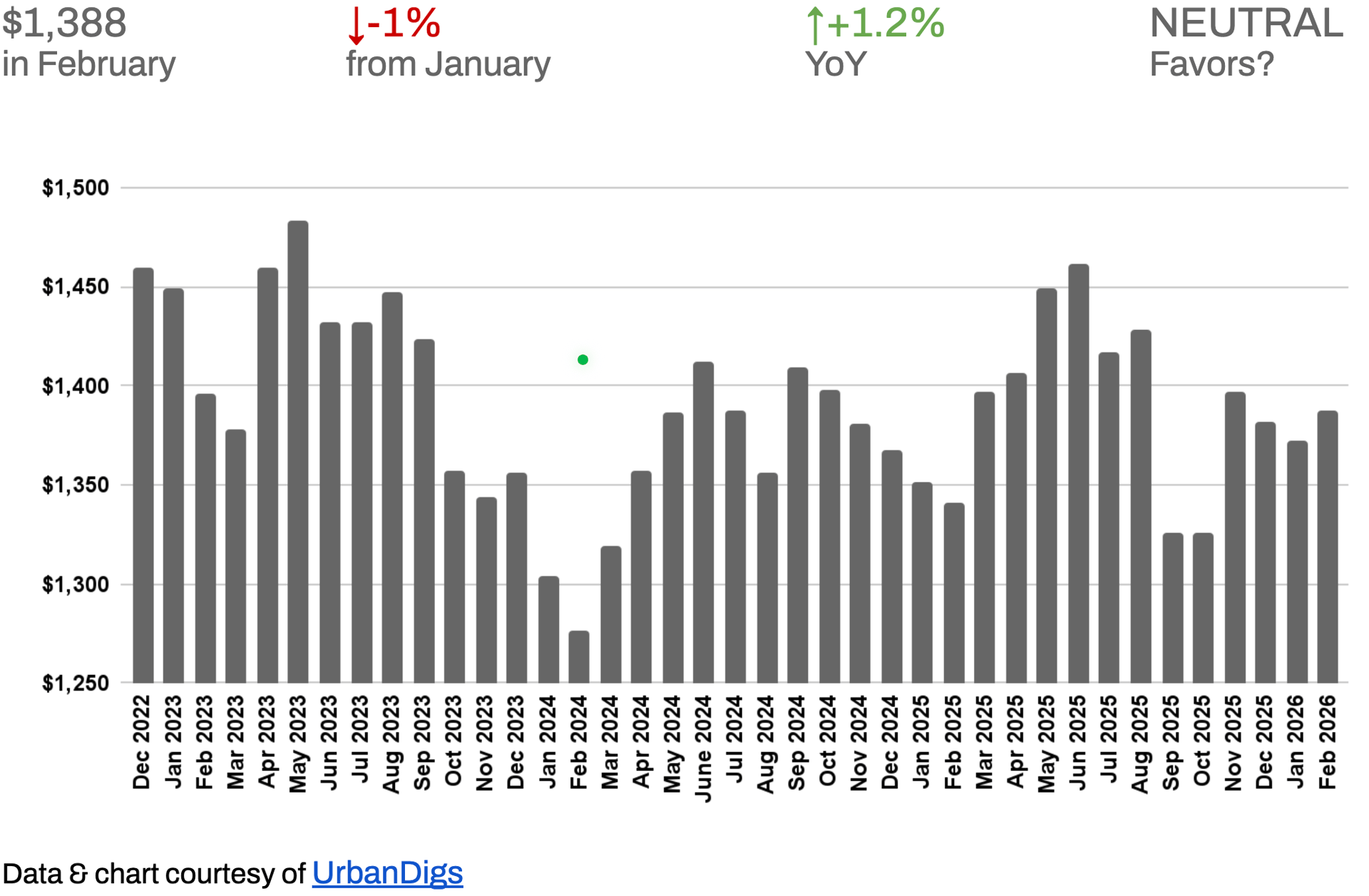

Manhattan Median PPSF

Pricing Holds Steady Despite Seasonal Dip

Median price per square foot registered $1,388 in February, down 1.0% from January but up 1.2% year-over-year. The slight monthly decline reflects normal winter seasonality rather than structural repricing.

Pricing stability continues to define Manhattan’s market, especially in well-located, move-in-ready properties.

🟦 Buyers: Broad price declines are not supported by current supply-demand fundamentals. Value remains asset-specific.

🟪 Sellers: The pricing floor remains intact. Market-aligned properties are achieving strong outcomes.

Outlook: PPSF is expected to firm modestly through Q2 as spring demand absorbs available inventory.

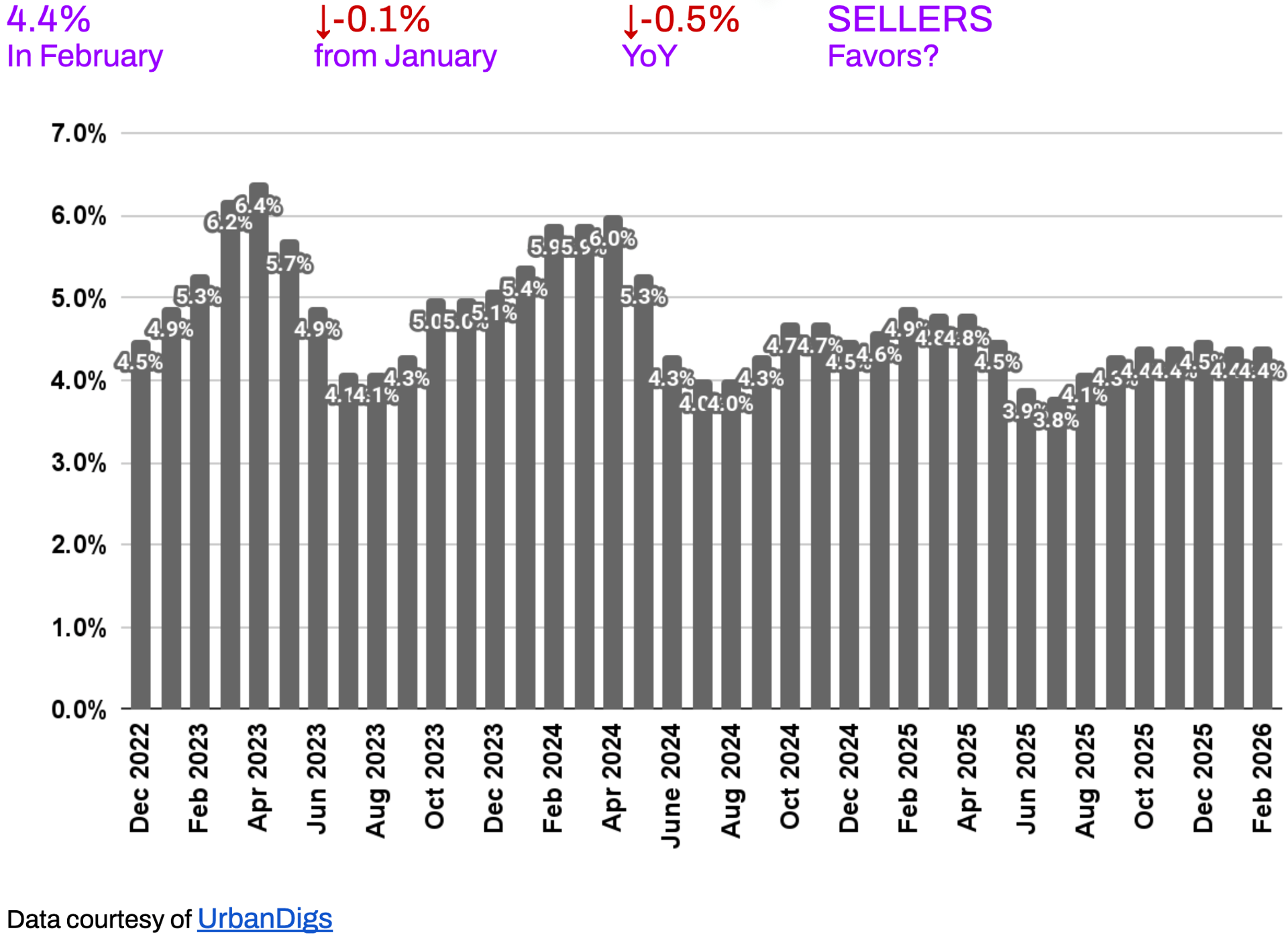

Manhattan Median Listing Discount

Negotiation Room Remains Limited

The median listing discount tightened to 4.4% in February, down 0.1% from January and 0.5% year-over-year. That keeps negotiation margins near multi-year lows and signals continued seller confidence.

Discount compression is often one of the earliest indicators of leverage, and current levels clearly lean toward sellers.

🟦 Buyers: Competitive, well-structured offers remain the most effective strategy.

🟪 Sellers: The market continues validating realistic asking prices.

Outlook: Discounts may compress slightly further if spring demand strengthens.

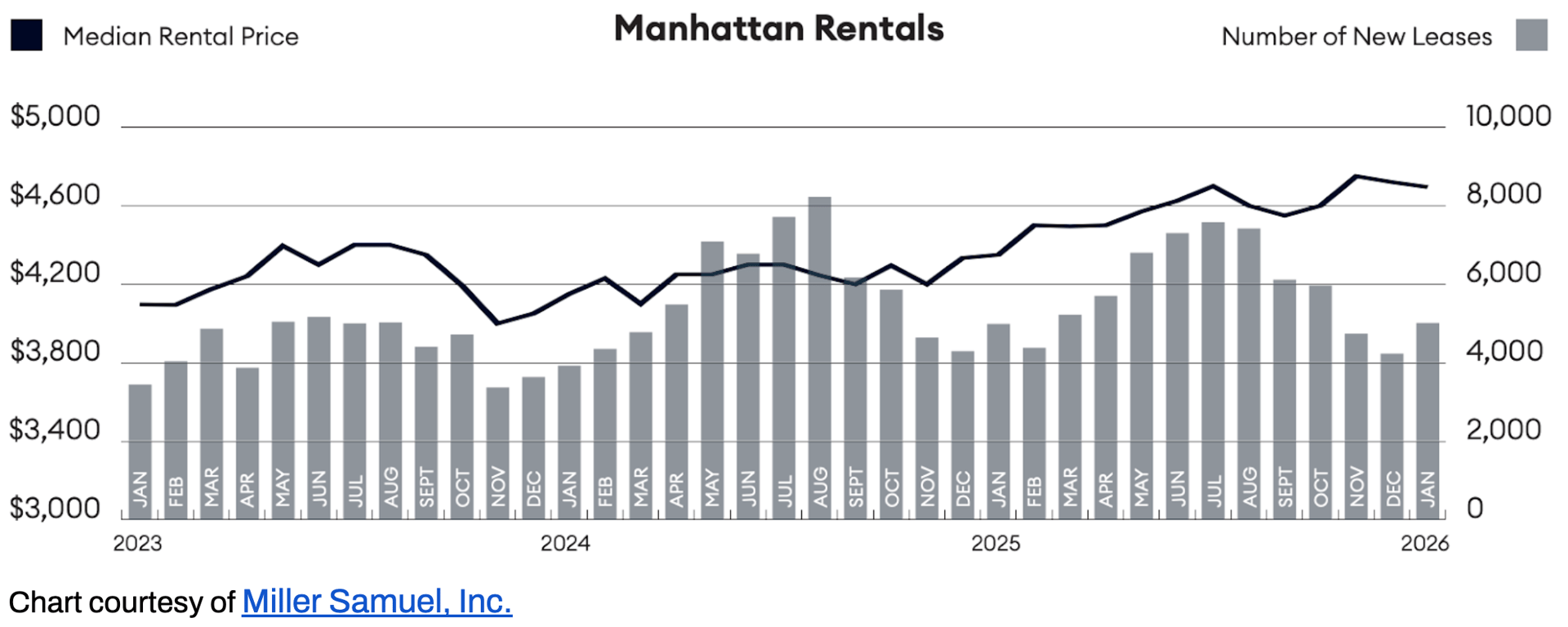

RENTAL REMARKS

Rents Remain Elevated as Inventory Stays Tight

Manhattan’s rental market started the year near record levels, with the January median rent at $4,695, up 7.9% year-over-year. Inventory stood at 7,965 listings, marking the seventh consecutive annual decline, while vacancy remained well below the decade average. Despite the typical seasonal softness in January, average rents reached a new high — reinforcing how tight conditions remain.³

Strong rental pricing continues to support overall asset values and reinforces ownership demand, particularly at the entry level where monthly mortgage payments increasingly compete with elevated rents.

🟦 Renters: Affordability remains the primary challenge. Preparation and speed are essential, especially for studios and one-bedrooms in prime locations.

🟪 Landlords: Fundamentals remain favorable. Tight vacancy and rising average rents support stable income and hold strategies.

Outlook: Unless inventory expands meaningfully in spring, rental pricing is expected to remain firm through mid-2026.

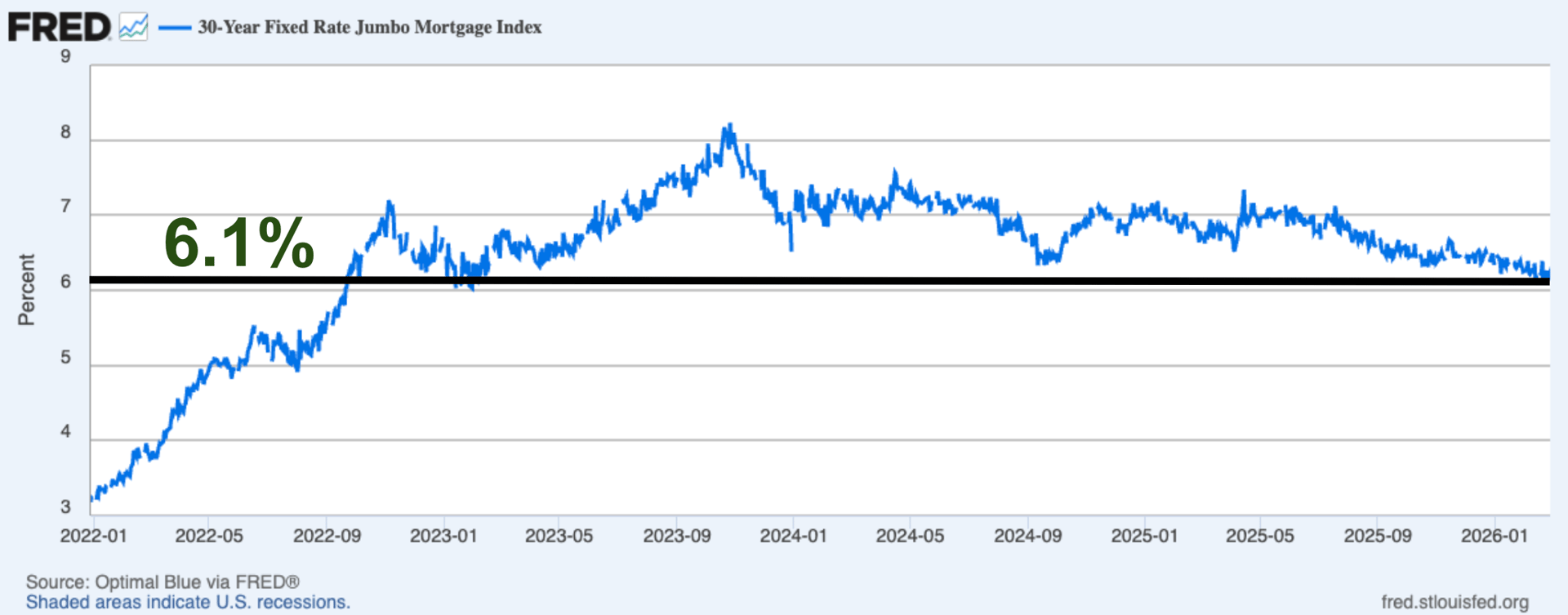

MORTGAGE REMARKS

Mortgage Rate Stability Is Reducing Friction

Mortgage conditions have become more predictable. By the end of February, average 30-year jumbo rates were hovering around 6.1%⁴, with effective APRs close to 6.0%⁵. That is meaningfully lower than the peaks above 7% seen in 2025 and, more importantly, far less volatile.

While rates remain elevated compared to the ultra-low period of 2020–2021, the stabilization near the 6% range has reduced the “rate shock” psychology that defined much of 2023 and early 2024. Buyers today are adjusting expectations rather than waiting for a dramatic drop, and transaction timing is increasingly driven by life decisions rather than attempts to anticipate Federal Reserve policy.

Outlook: Absent a material change in inflation or labor data, rates are likely to remain range-bound near current levels through mid-2026. Stability — not sharp declines — is the more probable scenario.

INVESTOR INSIGHTS

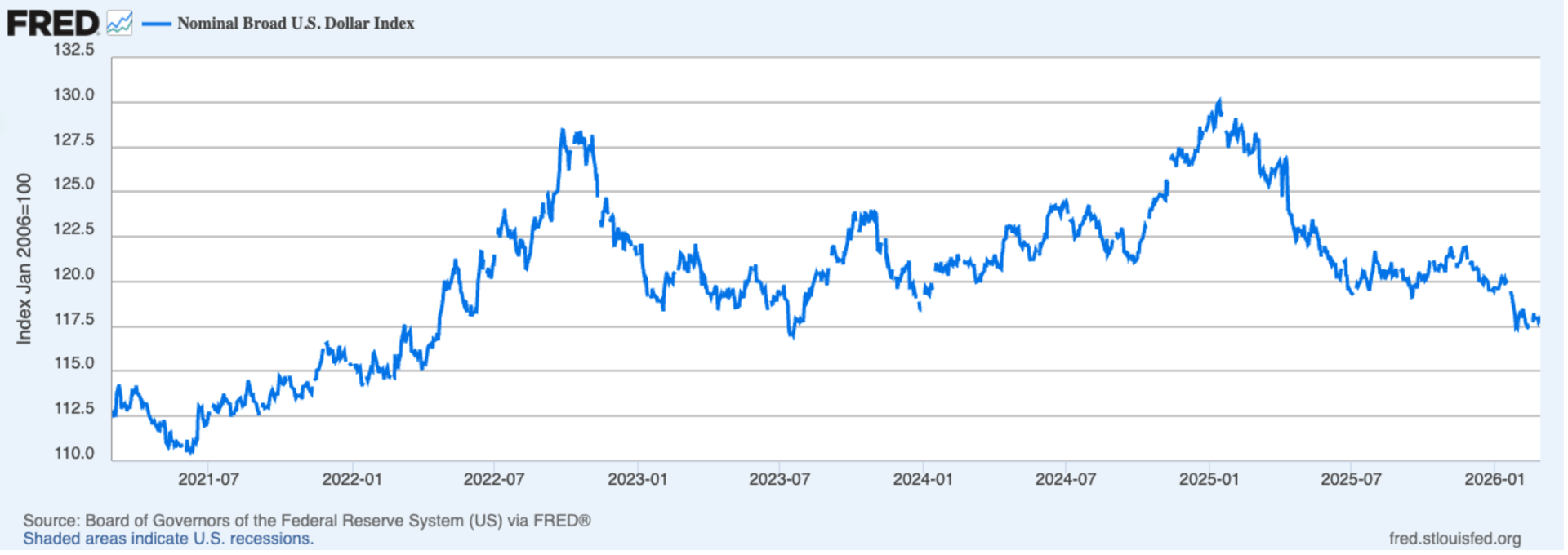

A weakening U.S. dollar is quietly improving the purchasing power of international buyers — particularly those from the Eurozone, the U.K., and other major economies where currencies have strengthened 10%+ against the dollar over the past year. For a European buyer, Manhattan real estate has effectively become more affordable in local-currency terms without any change in asking prices. This is a meaningful, underappreciated tailwind for international demand in Manhattan's luxury and ultra-luxury segments.

Domestic investors remain cautious. With investment mortgage rates hovering around 6.1% and stabilized rental yields in the 3–4% range, risk-adjusted returns for traditional condo and co-op investments are currently uninspiring. As a result, capital deployment is increasingly disciplined and underwriting-driven rather than momentum-based.

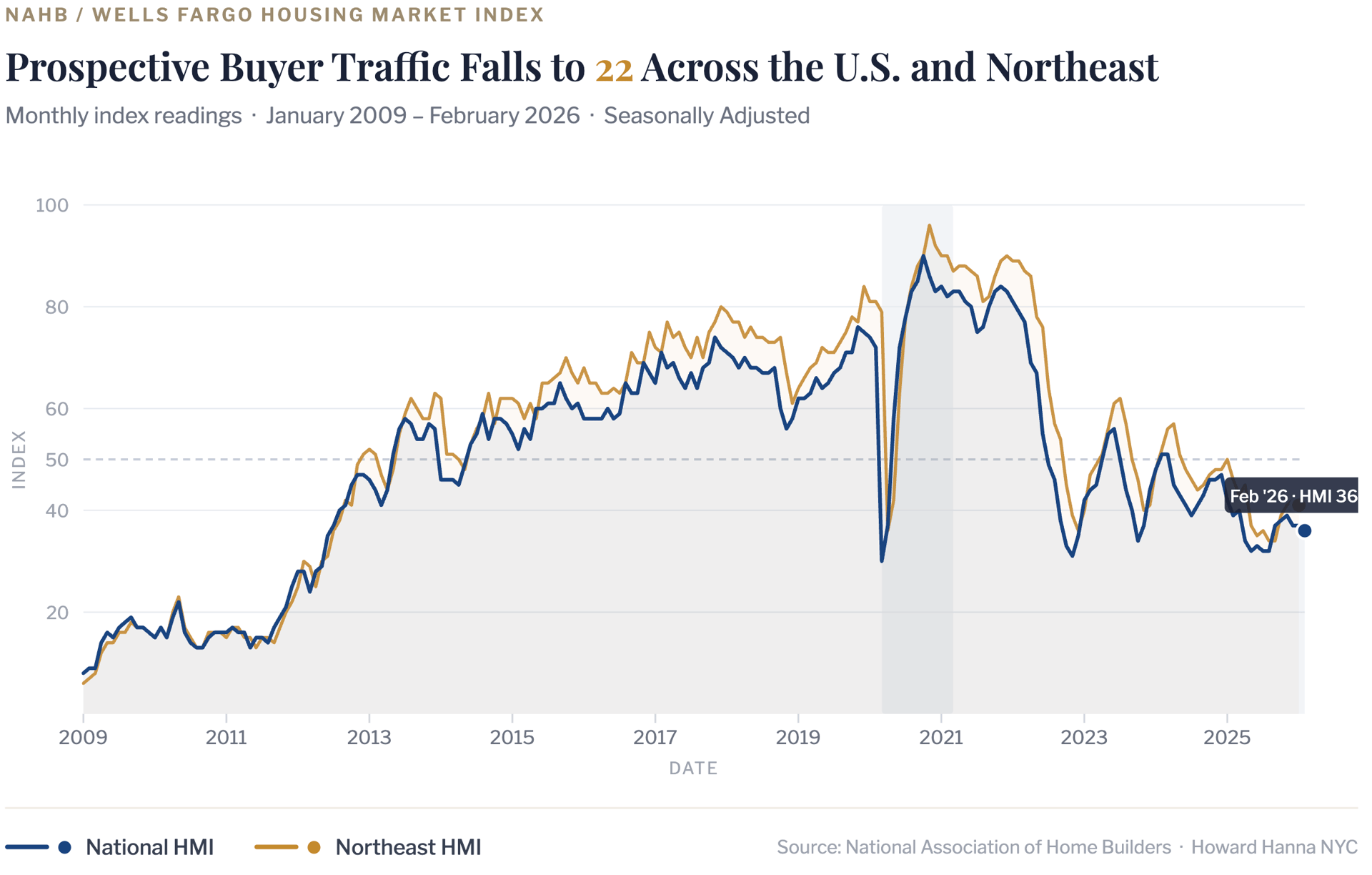

The NAHB/Wells Fargo Housing Market Index edged down to 36 in February 2026 (preliminary), its lowest reading since late 2023, as elevated mortgage rates and affordability headwinds continued to weigh on builder confidence nationally. Prospective buyer traffic fell to 22 — a particularly telling subcomponent, as foot traffic at new construction sites is often the earliest leading indicator of demand momentum. Current sales conditions held at 41 while six-month expectations slipped to 46, suggesting builders see limited near-term relief without a meaningful rate move.

In the Northeast, sentiment has mirrored the national softening, with the regional HMI retreating alongside broader affordability pressures.

For Manhattan residential real estate, the signal is nuanced. The HMI measures new single-family construction sentiment, a market segment that is largely absent in Manhattan. What the data does reflect is the broader psychology of the buyer pool: caution, rate sensitivity, and a preference for patience over urgency. That said, Manhattan's resale and luxury condo markets continue to be driven more by equity wealth, global capital flows, and limited trophy inventory than by mortgage-rate-dependent demand. The current environment favors well-priced, move-in-ready listings and creates selective opportunities for buyers who have been waiting on the sidelines — particularly as sellers recalibrate expectations in line with today's cost-of-capital reality.

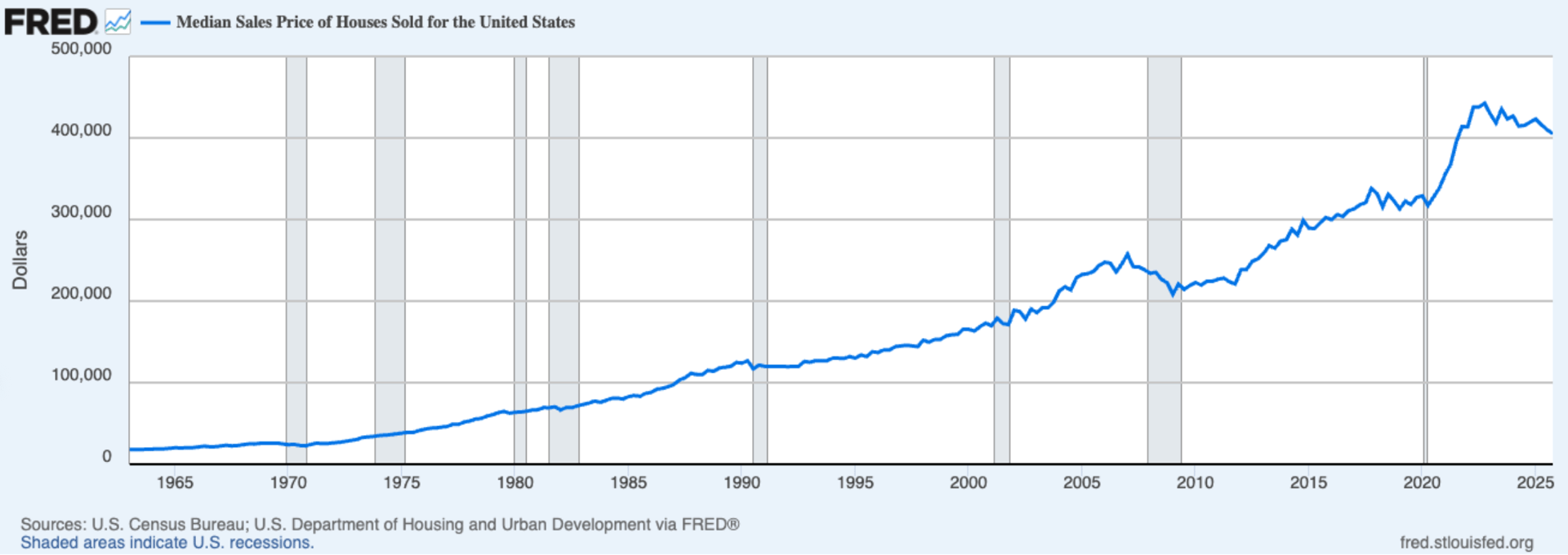

The chart below illustrates that U.S. national median home prices have risen significantly over the past five years, while Manhattan prices have remained notably more stable — insulated from the broader appreciation cycle and therefore not facing the same correction risk seen in other markets.

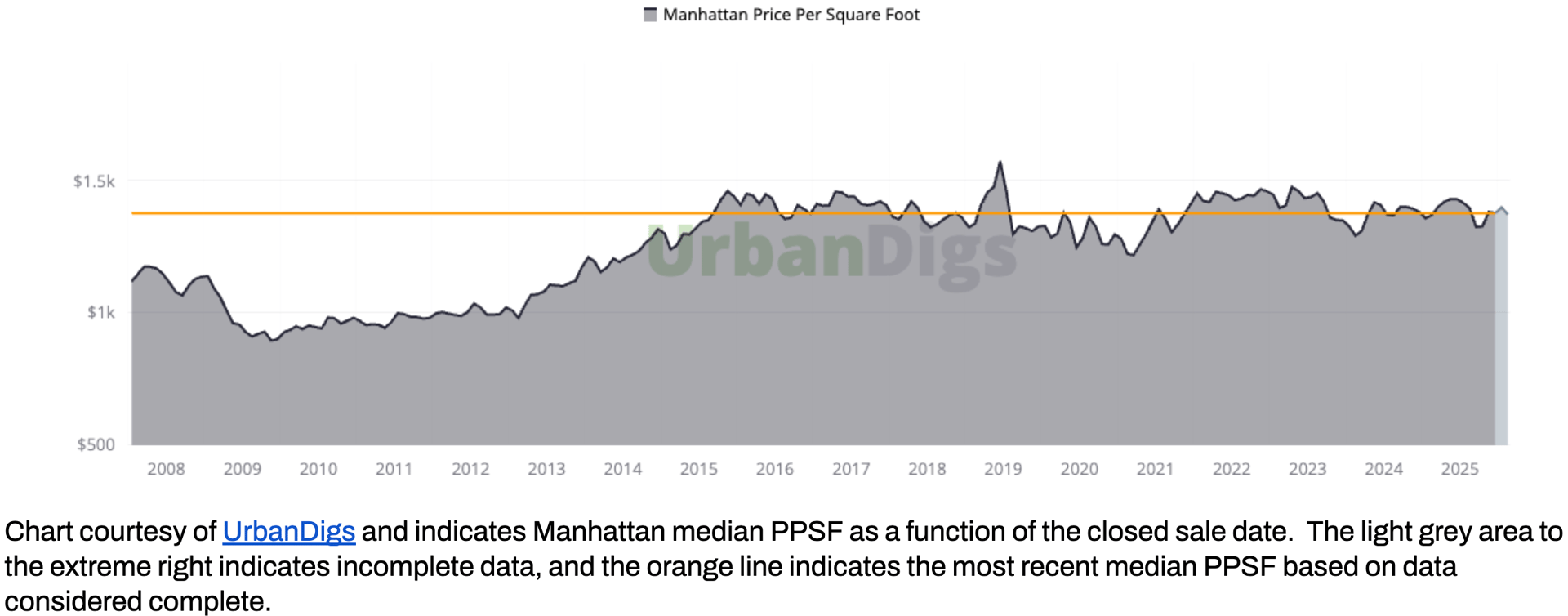

Notably, after rising from a post-financial-crisis trough near $950/sf to approximately $1,350/sf by 2015, Manhattan’s median PPSF has traded in a remarkably tight range for over a decade — a testament to the market’s structural price stability and resistance to the kind of boom-bust volatility seen in other U.S. metros.

Key Insight: Manhattan is performing exactly as a mature, supply-constrained luxury market should: absorbing rate pressure without distress, rewarding well-priced listings, and offering selective opportunities for buyers who are prepared to act. This is not a buyer’s market or a seller’s market — it is a quality market, where execution matters more than timing.

Outlook: Spring 2026 is expected to bring a gradual increase in both listings and signed contracts. Rate stability, improving buyer confidence, and persistent supply constraints point toward steady price support rather than sharp moves in either direction. Buyers who have been waiting for a “better moment” may find that this spring offers the clearest window in two years — inventory is rising before competition peaks. For sellers, the first eight weeks of spring remain the optimal listing window.

References

1. Data courtesy of UrbanDigs

2. According to the Howard Hanna NYC Manhattan Leverage Index

3. Data courtesy of Miller Samuel, Inc.

4. Data courtesy of Federal Reserve Bank of St. Louis

5. JUMBO mortgage rate APR data courtesy of Bank of America, Chase, and Wells Fargo

6. Cover Photo by Rihards Gederts.

If you would like to chat about the most recent market activity,

feel free to contact us at [email protected] or

connect with one of our Advisors.

Howard Hanna NYC brings the nation’s largest independent and family-owned brokerage to New York City, uniting the strength of a national network with the insight and sophistication of a local firm. Formed through joining forces with Elegran Real Estate, Howard Hanna NYC delivers a seamless, full-service experience backed by more than 15,000 agents across 500 offices in 14 states. The firm’s forward-thinking, agent-first culture continues to shape the future of real estate across Manhattan and the Tri-State area.Learn more at www.howardhannanyc.com.