BROOKLYN SPRING 2026: STRONG ASSETS STILL SELL — EVERYTHING ELSE NEGOTIATES

Brooklyn entered spring 2026 with a market that is more balanced than Manhattan's. The Howard Hanna NYC Brooklyn Leverage Index² moved modestly toward buyer territory in March, reflecting a mixed but coherent picture: supply is rising year-over-year, days on market are lengthening, and contract volume remains below 2025 levels. At the same time, median price per square foot surged 13.4% year-over-year, and nearly one in four sales is closing above asking price.

This is not a buyer's market or a seller's market. It is a market where the signals point in different directions depending on which metric you look at — and where understanding that nuance is the difference between a well-executed transaction and a mispriced one. For buyers, there is more room to negotiate than in Manhattan. For sellers with strong assets in desirable locations, pricing power remains real.

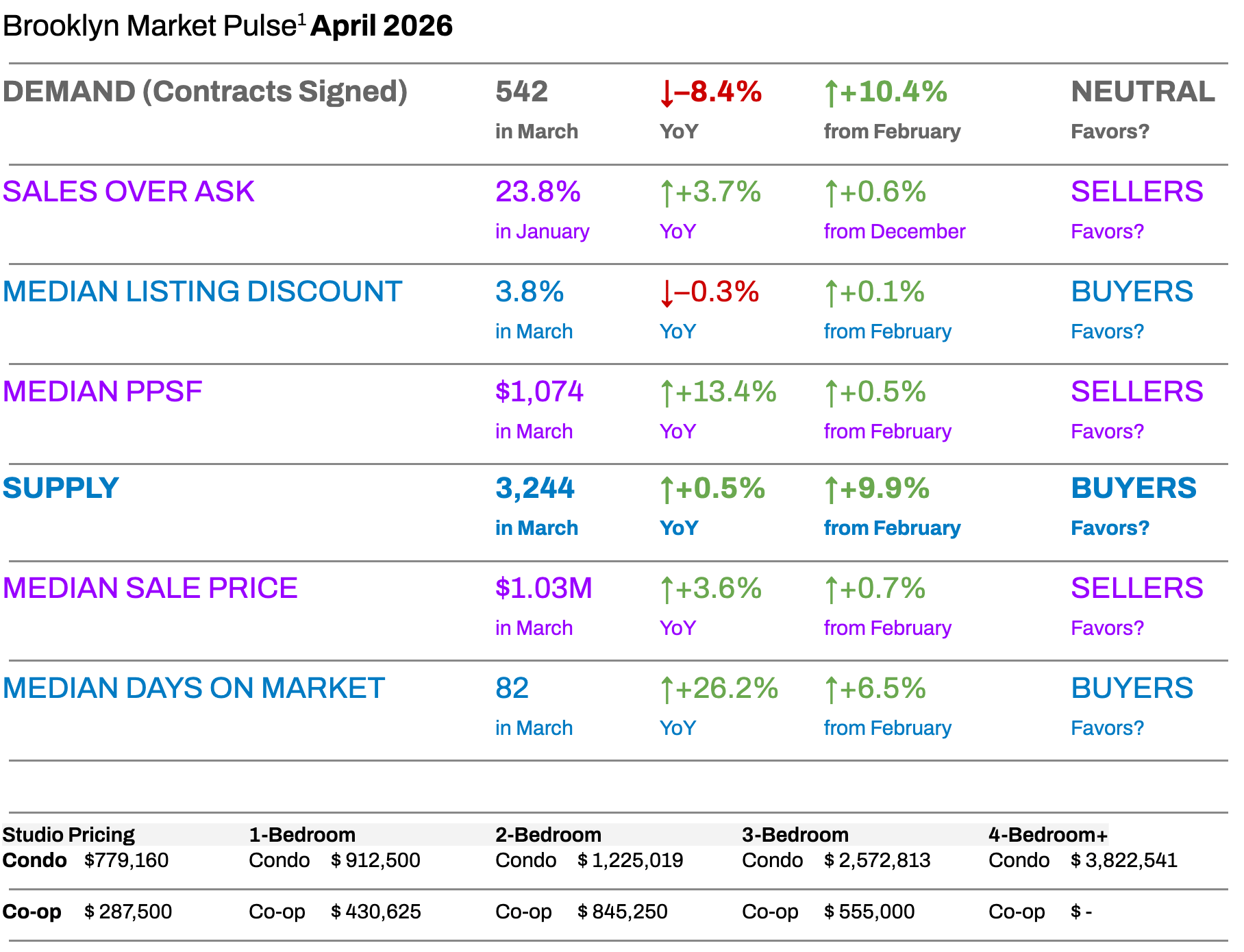

MARKET SNAPSHOT: FIVE NUMBERS THAT MATTER

-

542 contracts signed in March — up 10.4% from February, confirming spring engagement, though still 8.4% below March 2025.

-

3,244 active listings — up 9.9% year-over-year, giving buyers more options than in Manhattan and putting mild pressure on sellers to price competitively.

-

$1.03M median sale price — up 3.6% year-over-year and crossing the $1M threshold, reflecting continued long-term appreciation.

-

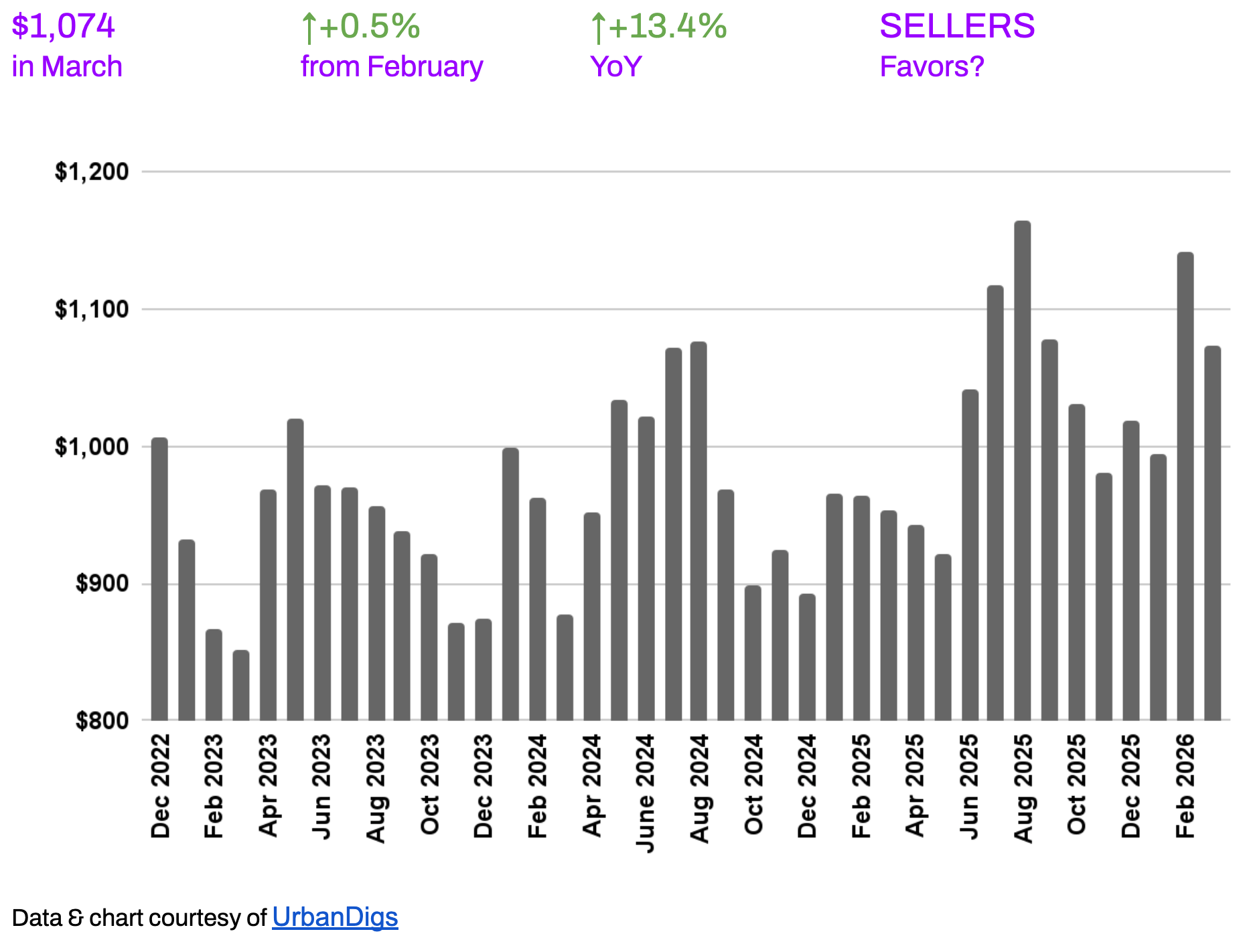

$1,074 median price per square foot — up 13.4% year-over-year, the most striking data point of the month and a clear signal that demand for well-located Brooklyn assets remains structurally firm.

-

23.8% of sales closed above asking price — one of the highest readings in the metro, underscoring that competitive properties still attract multiple offers.

KEY TAKEAWAYS

-

Supply rose 9.9% year-over-year to 3,244 listings — unlike Manhattan, Brooklyn inventory is above prior-year levels, giving buyers incrementally more negotiating room.

-

Contracts increased 10.4% from February to 542, confirming spring engagement, but remain 8.4% below March 2025 — demand has not yet fully recovered.

-

Median PPSF surged 13.4% year-over-year to $1,074 — the strongest pricing signal in the market and a meaningful indicator of long-term asset appreciation.

-

The median sale price crossed $1.03M, up 3.6% year-over-year — a milestone that reflects Brooklyn's continued evolution as a premium market.

-

Days on market extended to 82, up 26.2% year-over-year — sellers need to price accurately from day one, as the days of quick offers regardless of pricing are not the current environment.

-

23.8% of sales closed above asking price — nearly one in four transactions — confirming that well-priced, well-located properties still generate real competition.

OUTLOOK

Brooklyn's spring market is more textured than the headline numbers suggest. The right listing — priced correctly, presented well, and in a desirable location — is still attracting multiple offers and closing above ask. But the market is no longer forgiving of overpricing. Days on market are up meaningfully, supply is above last year, and buyer volume has not yet returned to 2025 levels. This is a spring that rewards preparation on both sides of the table.

Photo by Rihards Gederts | Howard Hanna NYC

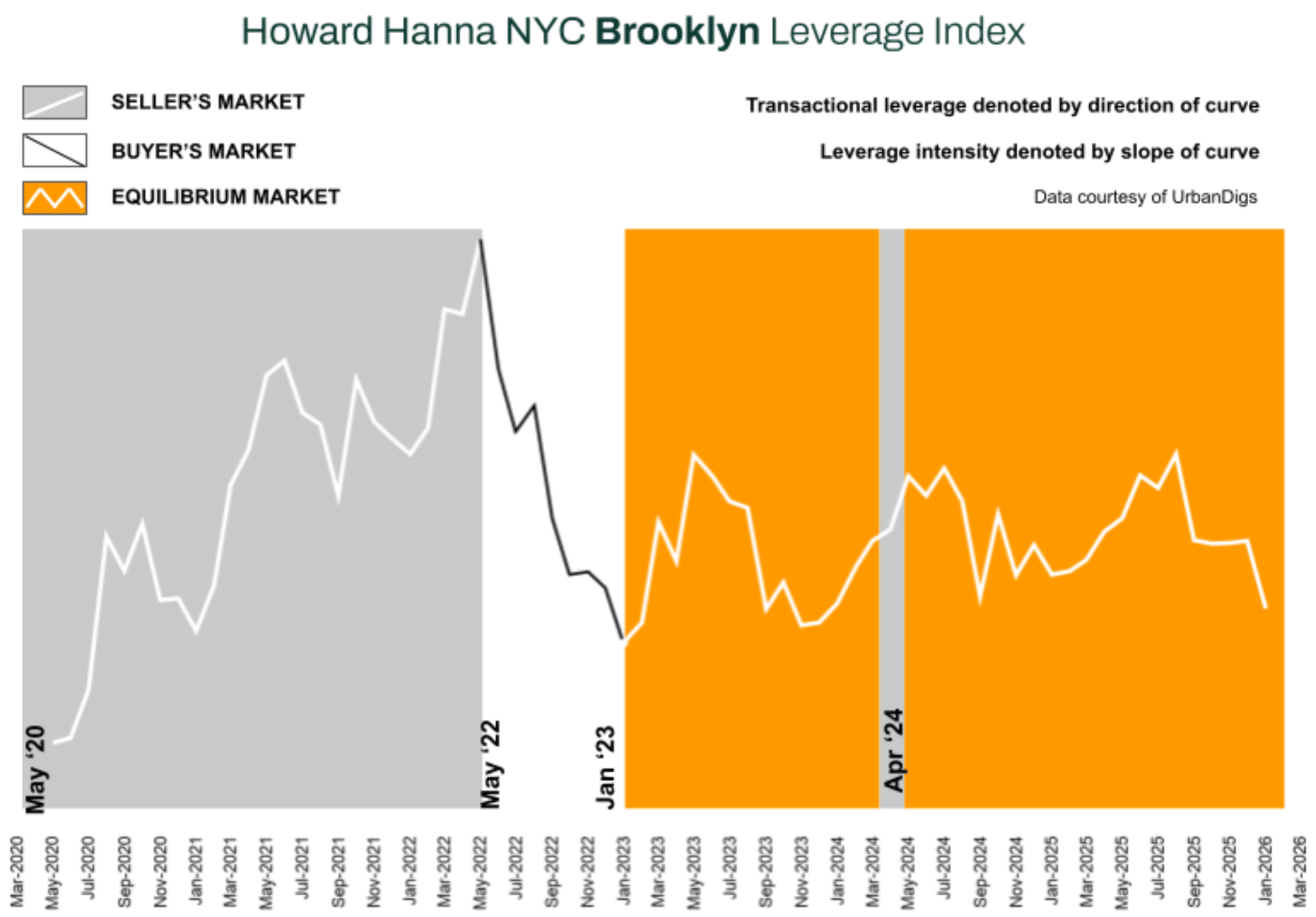

Howard Hanna NYC Brooklyn Leverage Index

The Howard Hanna NYC Brooklyn Leverage Index blends four market signals - supply, demand, median price per square foot, and median listing discount - to capture the balance of power between buyers and sellers.

Direction Matters:

-

An upward-sloping curve = seller’s market

-

A downward-sloping curve = buyer’s market

-

The steeper the slope, the stronger the advantage for either side

In March 2026, the index moved modestly toward buyer territory — a notable divergence from Manhattan, where the index held in seller-leaning territory. Of its four core inputs: supply and listing discounts favor buyers; demand sits in neutral territory, leaning slightly buyer-ward given the year-over-year contraction in contracts; and median PPSF is the single seller-side signal — and a strong one, with a 13.4% year-over-year gain that suggests underlying asset demand remains intact even as surface-level market mechanics soften.

The takeaway from the index is not that Brooklyn has become a buyer's market — it is that the leverage balance has normalized relative to the seller-favorable conditions of 2021–2022.

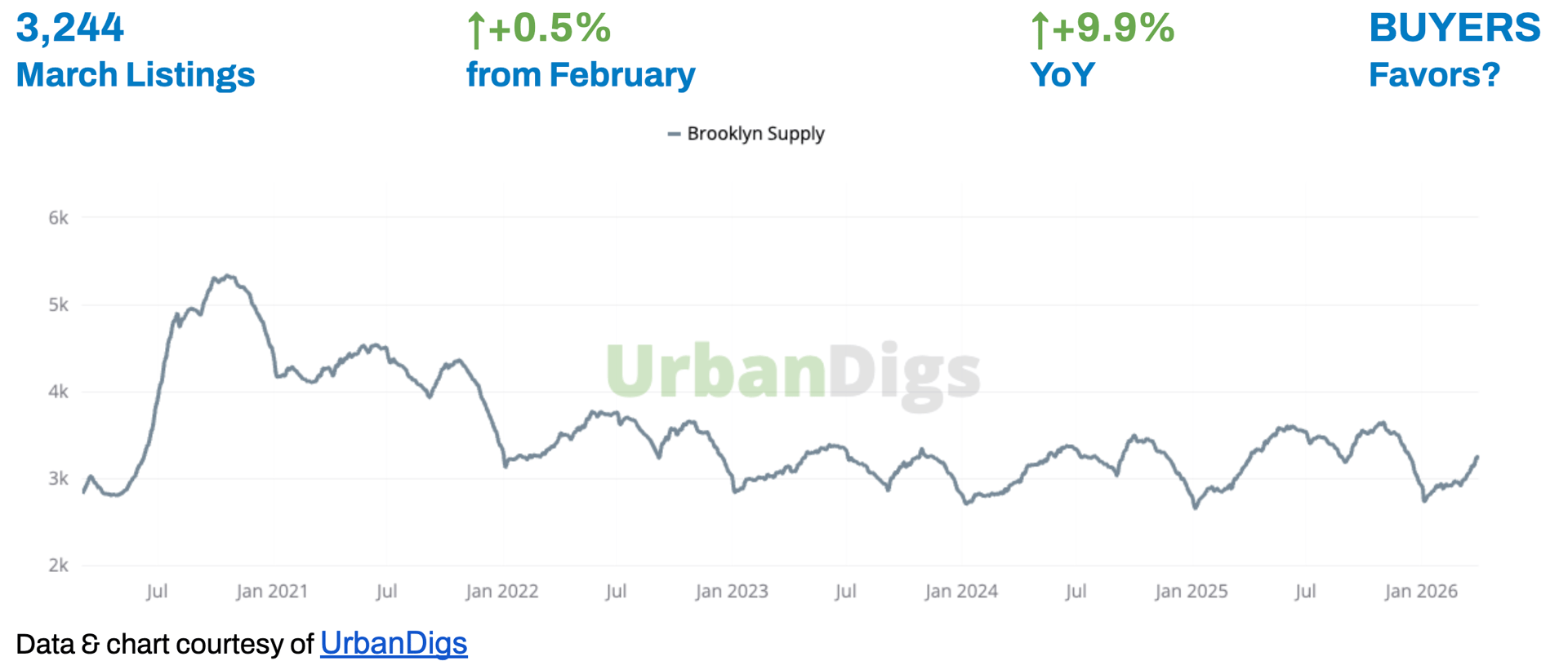

Brooklyn Supply

INVENTORY RETURNS TOWARD NORMAL — AND SELLERS MUST PRICE ACCORDINGLY

Brooklyn's active listing count reached 3,244 in March, up modestly from February and — crucially — 9.9% above where it stood in March 2025. This is the sharpest contrast with Manhattan, where inventory remains nearly 10% below last year. In Brooklyn, buyers have more options heading into spring, and sellers cannot rely on structural scarcity to do the pricing work for them.

That said, context matters: the 9.9% year-over-year increase does not indicate oversupply. It indicates normalization. Brooklyn inventory spent much of 2022–2024 at historically depressed levels.

🟦 Buyers: You have more selection than a year ago, and more negotiating room than in Manhattan. Use this spring window strategically — more inventory means fewer bidding wars on mid-market listings, but well-priced premium properties still attract competition.

🟪 Sellers: The days of listing at any price and finding a buyer quickly are behind us for now. Inventory is rising, days on market are extending, and buyers have options. Accurate pricing from day one is not just advisable — it is the defining factor between a smooth transaction and a lengthy, discount-driven one.

Outlook: Inventory is expected to continue its seasonal rise through April and May. Unless demand accelerates sharply, the supply-demand balance will remain closer to equilibrium than to either extreme — which means price discovery will continue to be driven by individual asset quality rather than market-wide scarcity.

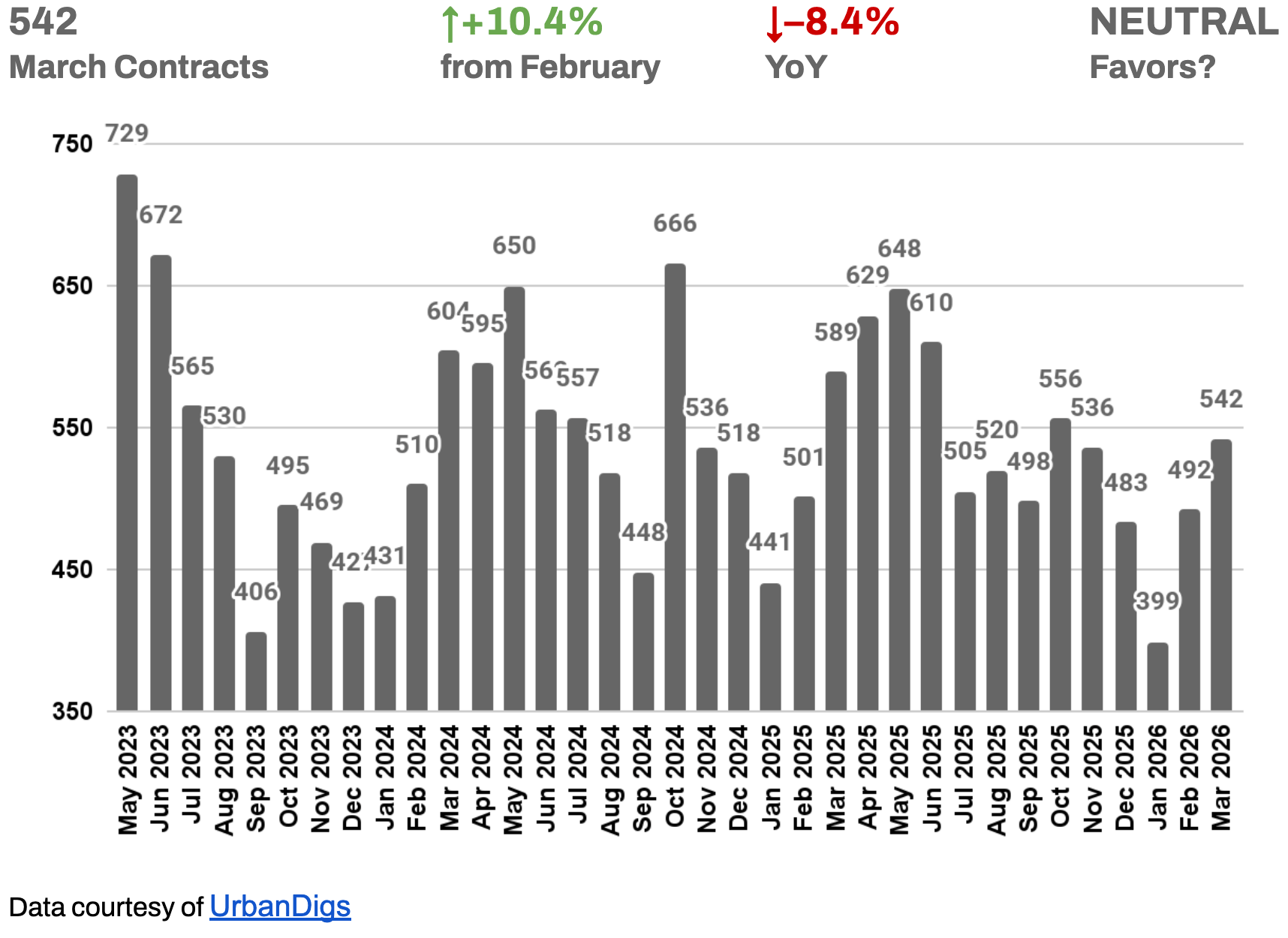

Brooklyn Demand

SPRING IS ENGAGED — BUT 2025 LEVELS REMAIN OUT OF REACH

March brought 542 signed contracts, a 10.4% increase from February and a clear confirmation that buyers who sat out the winter are returning to the market. The month-over-month rebound is real and meaningful — it reflects genuine spring engagement rather than a statistical bounce. At 542 contracts, Brooklyn demand sits comfortably within its recent mid-cycle range.

The year-over-year picture, however, requires honest accounting: March 2026 is 8.4% below March 2025. It reflects a buyer pool that remains rate-sensitive, selective, and unwilling to stretch — a rational response to a market where affordability has tightened and mortgage rates have climbed back toward 6.5%.

🟦 Buyers: The month-over-month trend is your signal — spring has started, and competition for the best properties is building. If you have been waiting for the right opportunity, this spring window offers a better inventory-to-competition ratio than what the fall cycle is likely to deliver.

🟪 Sellers: The 10.4% demand rebound from February is a tailwind, and well-positioned listings will benefit from it. But the 8.4% year-over-year contraction is a reminder that the market is not self-correcting for overpricing.

Outlook: Contract volume is expected to increase through April and May as more spring inventory comes online and buyer urgency builds with the season. A full recovery to 2025 levels is possible but not certain — much will depend on whether mortgage rates stabilize or continue to drift higher.

Brooklyn Median PPSF

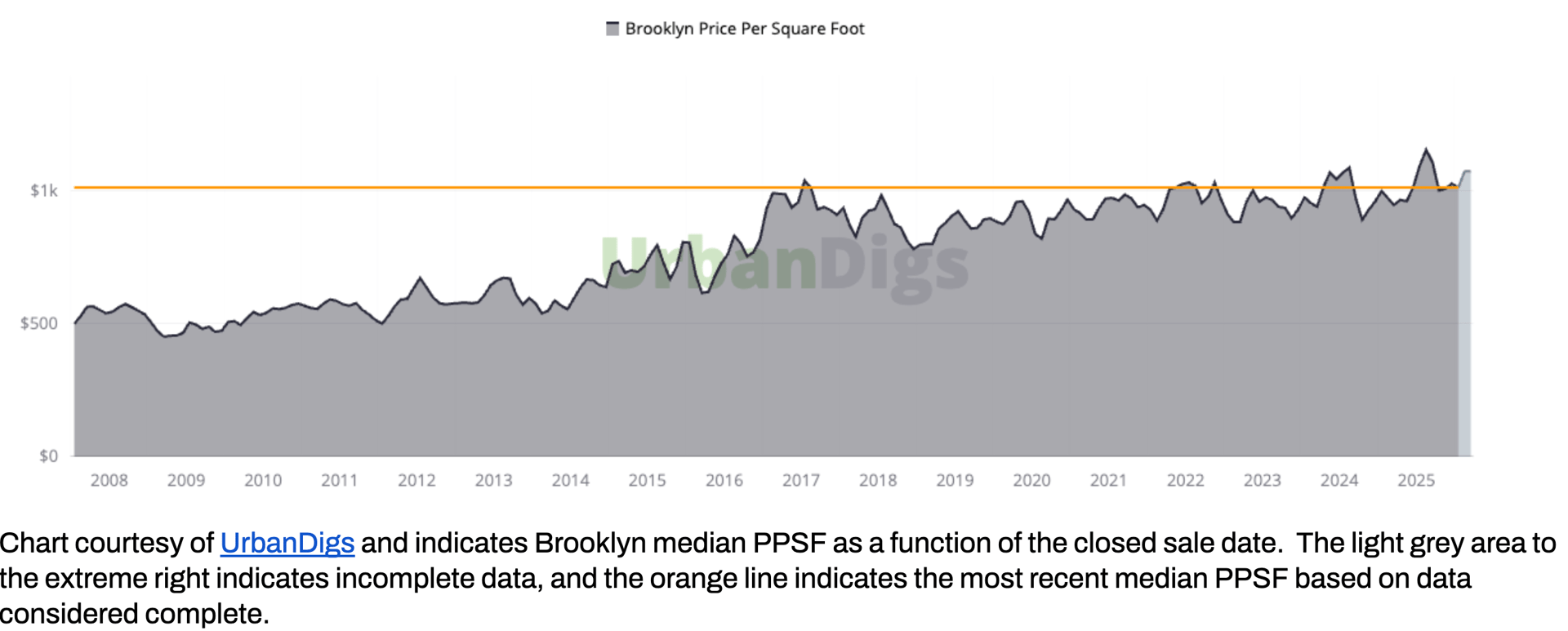

$1,074 PER SQUARE FOOT, UP 13.4% YEAR-OVER-YEAR: THE MONTH'S DEFINING NUMBER

Brooklyn's median price per square foot reached $1,074 in March — up 0.5% from February and 13.4% above March 2025. That year-over-year acceleration is the most striking data point in this update and deserves careful interpretation.

A 13.4% annual gain in PPSF does not mean the entire Brooklyn market appreciated 13.4%. It reflects a meaningful shift in the composition of what sold: March 2026 saw a higher concentration of larger, better-located, and more premium transactions than the comparable period in 2025. That mix effect amplifies the headline figure — but it also points to something real: the top end of the Brooklyn market is performing strongly, and buyers are willing to pay for quality.

Rising from approximately $500 per square foot in the post-financial-crisis period to roughly $1,000 by 2017, Brooklyn has followed a disciplined, sustained appreciation path — interrupted by the pandemic dislocation but not derailed by it. The current level approaching $1,074 represents a market that has earned its premium through organic, demand-driven growth over fifteen years, not through a speculative cycle.

🟦 Buyers: Strong PPSF does not mean overpaying is inevitable — it means the market rewards selectivity.

🟪 Sellers: The 13.4% year-over-year PPSF gain supports premium pricing for well-located, well-presented assets. Properties with outdoor space, high ceilings, and recent renovation are achieving strong PPSF — and the data supports holding the line on pricing for those listings.

Outlook: PPSF is expected to remain firm through spring as demand for premium Brooklyn assets continues to outpace the modest supply increase. Any softening is more likely to appear in days-on-market than in PPSF compression for quality listings.

Brooklyn Median Listing Discount

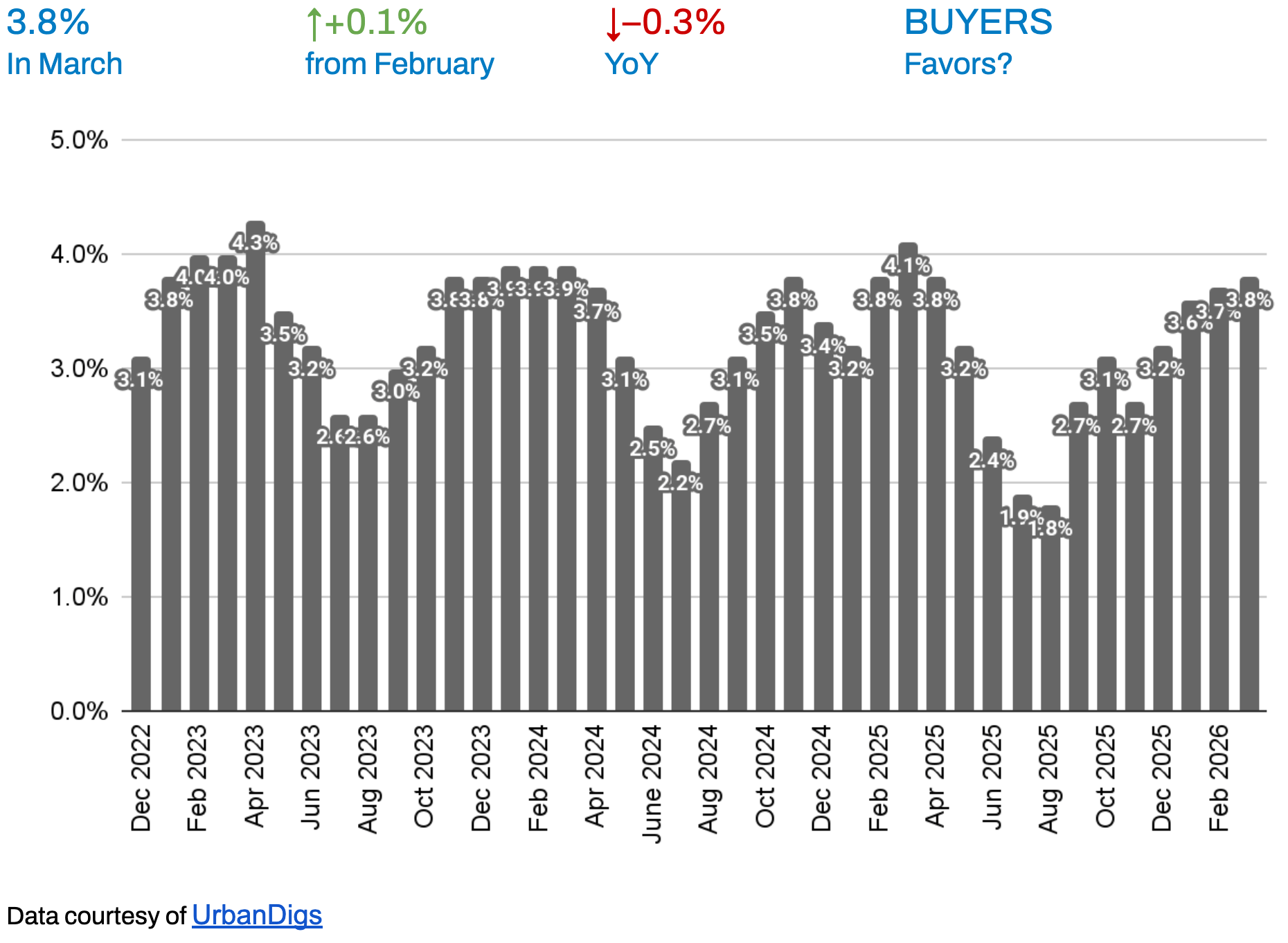

3.8% DISCOUNT: NEGOTIATING ROOM EXISTS — BUT IT IS UNEVENLY DISTRIBUTED

The median listing discount in Brooklyn held at 3.8% in March — fractionally higher than February and down slightly from a year ago. In practical terms, properties are trading at approximately 96.2 cents on the dollar of their last asking price. For a $1M listing, that translates to roughly $38,000 of negotiating room on average.

That figure is modestly more buyer-friendly than Manhattan's 4.5% might suggest at first glance — but context matters here. Brooklyn's 3.8% discount reflects a market where the premium assets are closing with minimal discount or above ask, while longer-sitting listings are absorbing larger concessions to transact.

🟦 Buyers: The negotiating window exists — particularly on properties that have been on the market for more than 45 days or have already undergone price reductions.

🟪 Sellers: If your listing has been sitting, the 3.8% market average is a signal worth taking seriously. Strategic price alignment — not just "price reductions" — is the difference between reopening buyer interest and accumulating days on market.

Outlook: Listing discounts are unlikely to compress materially from current levels unless spring demand accelerates significantly. The more likely scenario is that the 3.7–4.0% range holds through Q2 as buyers and sellers continue to negotiate within a balanced-to-slightly-buyer-favoring framework.

RENTAL REMARKS

Source: StreetEasy · February 2026 NYC Market Report

Brooklyn Leads City in New Supply — But Rents Keep Rising Anyway

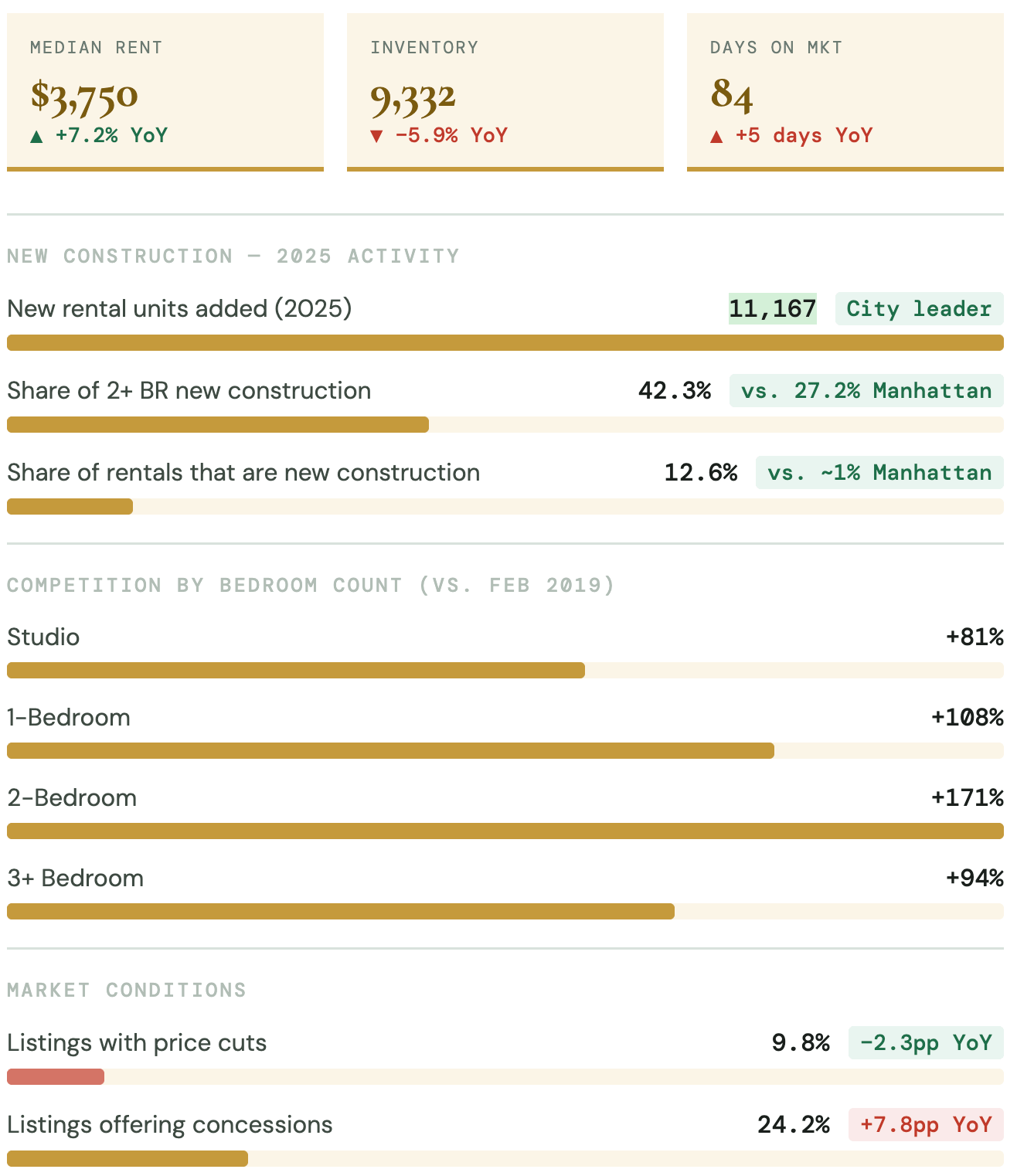

Brooklyn's rental market tightened further in February, with the median asking rent climbing 7.2% year-over-year to $3,750. Inventory fell 5.9% to 9,332 units — a steeper decline than Manhattan. Despite leading the city in new rental construction with 11,167 units added in 2025 (vs. 2,575 in Manhattan), demand has absorbed supply.³

Brooklyn also led the city in family-sized housing: 42.3% of new construction rentals had two or three bedrooms, compared to just 27.2% in Manhattan. Notably, competition on two-bedroom units surged 171% above pre-pandemic levels — the sharpest increase among all bedroom types citywide.

🟦 Renters: Brooklyn offers more new inventory and larger units than Manhattan, but competition remains fierce — particularly for two-bedroom apartments. Concessions (24.2% of listings) offer a negotiating window not available in most Manhattan buildings.

🟪 Landlords: Rising rents and high occupancy support strong asset performance. The concentration of new supply in family-sized units opens pricing power for well-positioned 2–3BR buildings, especially near transit.

Outlook: Brooklyn's pipeline of new construction is the strongest in the city, which may moderate rent growth modestly in select neighborhoods — but citywide demand and tight vacancy keep the market landlord-favorable heading into spring 2026.

MORTGAGE REMARKS

RATE UNCERTAINTY RETURNS — AND CHANGES THE CALCULUS FOR BROOKLYN BUYERS

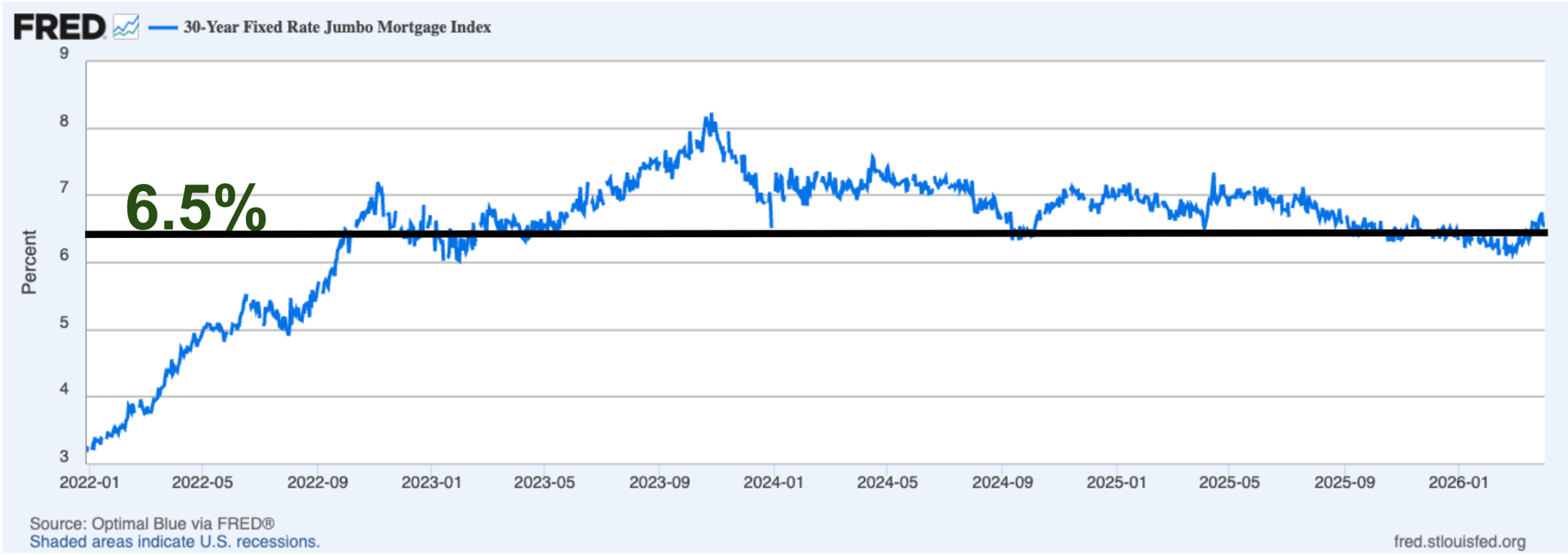

After a period of relative stability, mortgage conditions have grown more unpredictable. By early April, average 30-year jumbo rates had climbed back to approximately 6.5%⁴, with effective APRs near 6.4%⁵ — roughly 40 basis points above where they stood in February.

That move matters more for Brooklyn than for Manhattan, because a higher share of Brooklyn buyers are rate-sensitive: they tend to finance more of the purchase and rely more heavily on conventional mortgage products than the cash-heavy, equity-financed buyers who dominate Manhattan's upper segments.

The brief window of rate stability near 6.1% in late winter had begun to ease the "rate shock" psychology that has defined buyer behavior since 2023. Some of that progress has been undone. For Brooklyn buyers working with 20–30% down payments and conventional financing, the difference between a 6.1% and a 6.5% rate on a $1M mortgage is approximately $250 per month — meaningful for household budgeting, and enough to push some buyers back to the sidelines temporarily.

The longer-term perspective: rates remain far below the historical averages of the 1980s and 1990s, and the affordability constraint is primarily a function of price appreciation rather than rates alone. Buyers who are waiting for rates to fall to 5% may be waiting for a scenario that does not materialize in the near term.

Outlook: The path forward for rates depends on incoming inflation and labor data. A further move toward 7% is possible if inflation proves sticky; a return toward 6% is equally plausible if the economy softens. In the absence of clarity, locking early on well-priced properties remains the prudent strategy. Brooklyn's strong PPSF appreciation trend suggests that waiting for rate relief while prices continue to rise is not a risk-free strategy.

INVESTOR INSIGHTS

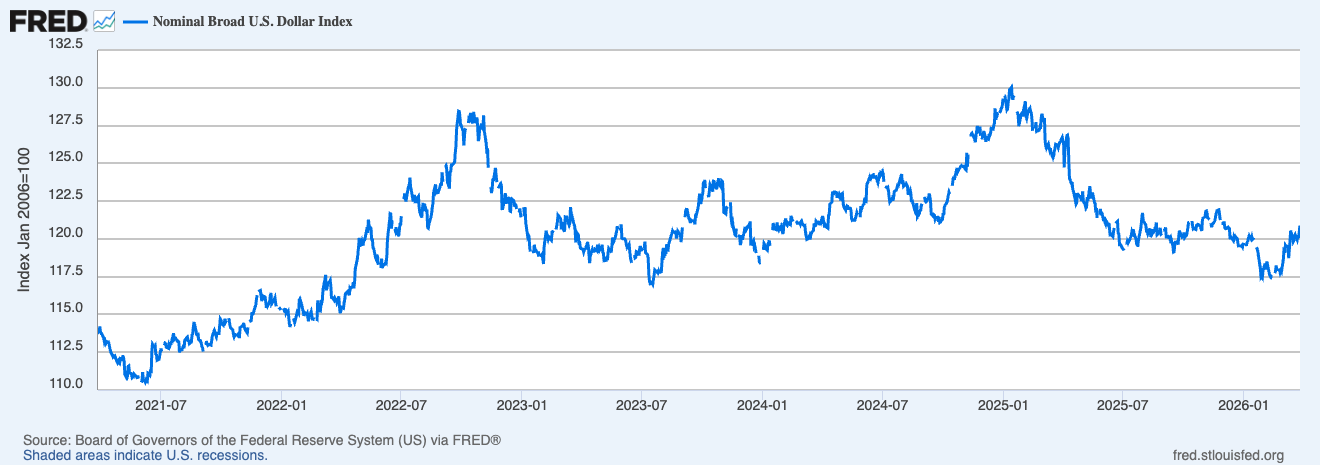

INTERNATIONAL BUYERS: A QUIET TAILWIND

A weakening U.S. dollar continues to improve the purchasing power of international buyers — particularly those from the Eurozone, the U.K., and other major economies where currencies have strengthened meaningfully against the dollar over the past 12–18 months. For a European buyer, Brooklyn real estate has effectively become more affordable in local-currency terms without any change in asking prices.

While Brooklyn draws less international capital than Manhattan's luxury segment, neighborhoods like DUMBO, Brooklyn Heights, Cobble Hill, and Park Slope have developed genuine global profiles — and the currency tailwind is beginning to show up in buyer inquiries from European and other international purchasers considering New York City as a primary or secondary residence.

DOMESTIC INVESTORS: DISCIPLINED AND SELECTIVE

Domestic investors remain cautious but engaged. With investment mortgage rates near 6.4% and stabilized rental yields in the 3–4% range, risk-adjusted returns on traditional condo and co-op investments require careful underwriting. The era of easy leverage-driven returns is behind us for now. What remains, however, is a market that rewards patient, value-oriented capital with a long time horizon.

Brooklyn co-ops in particular continue to offer compelling entry points: lower per-square-foot acquisition costs relative to condos, strong rental demand in adjacent neighborhoods, and the structural benefit of a housing stock that is not being meaningfully expanded by new development. For investors who can absorb the sublet restrictions that characterize many co-op buildings, the risk-adjusted return profile compares favorably to other asset classes at current price levels.

THE BROOKLYN PPSF STORY: FIFTEEN YEARS OF APPRECIATION

Brooklyn's median price per square foot tells one of the most compelling stories in the U.S. residential real estate market. Rising from approximately $500 per square foot in the years following the financial crisis, Brooklyn PPSF reached roughly $1,000 by 2017 — doubling over eight years in a market that experienced virtually none of the distress-driven volatility seen in sunbelt and secondary markets.

Since 2017, the appreciation curve has continued — more measured, but structurally intact. The current reading of $1,074 per square foot, with a 13.4% year-over-year acceleration, suggests that the market is not in a speculative phase. It reflects genuine, demand-driven price discovery in a borough that has been permanently revalued by demographic shifts, infrastructure investment, and a fundamental recalibration of what "Brooklyn" means to buyers globally.

For long-term investors, the insight is this: Brooklyn has never been a market of dramatic short-term gains. It has been a market of sustained, compounding appreciation — and the current trajectory is entirely consistent with that pattern.

References

1. Data courtesy of UrbanDigs

2. According to the Howard Hanna NYC Brooklyn Leverage Index

3. Data courtesy of StreetEasy · February 2026 NYC Market Report

4. Data courtesy of Federal Reserve Bank of St. Louis

5. JUMBO mortgage rate APR data courtesy of Bank of America, Chase, and Wells Fargo

6. Cover Photo by Rihards Gederts.