Manhattan Market Update: New Dev Performing at Par; Resale Underperforming

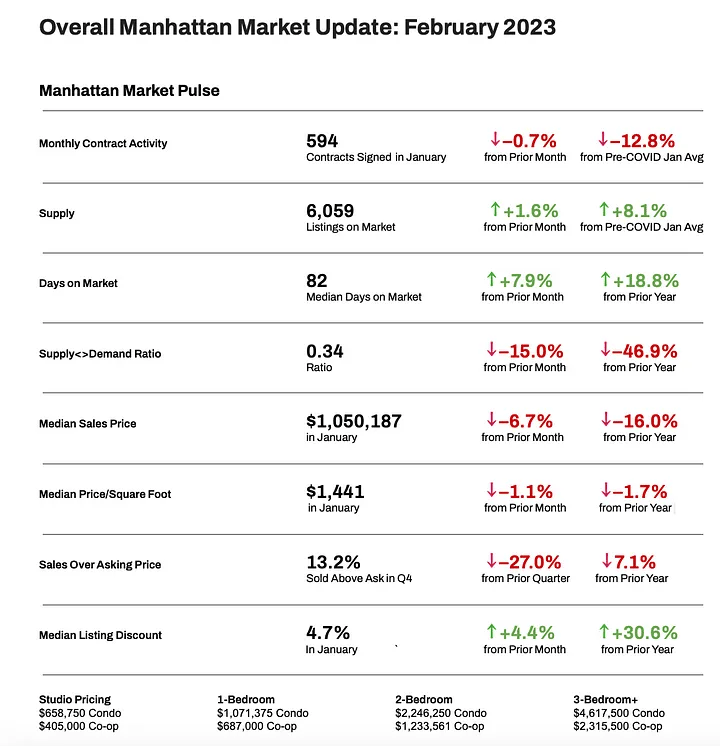

Compared to the pre-pandemic* benchmark, demand for residential real estate in Manhattan underperformed in January. The number of contracts signed for new developments is right on par with its historical average, but activity within the resale market, the larger of the two, has been slow.

Numbers from the final week of the month provided a glimmer of hope that buyers may be coming out of hibernation as we soon turn the corner towards spring.

* the period January 5, 2015, to March 1, 2020

Manhattan Supply

Within our weekly reports, we discussed the bi-annual supply cycle, with crests in Spring and Fall and troughs in Summer and Winter. January is the low point of the initial cycle, so numbers will increase from here. The bar chart below illustrates that the total supply is “normal” as it is within 10% of its pre-pandemic average. New supply, however, is a bit light compared to its pre-pandemic benchmark. Note: “Total Supply” refers to inventory on the market at a given time. “New Supply” refers to new inventory listed during a specific period.

Data Courtesy of UrbanDigs

Data Courtesy of UrbanDigs

Manhattan Buyer Activity

As discussed within our weekly reports, demand for Manhattan residential real estate has been trending below its historical average. The bar chart below illustrates this insight, as this January posted the fewest contracts signed during the 9 years observed. The same was true for December. However, as we noted in this report’s opener, the metric began to claw its way back towards historical parity during the final week of the month.

Data Courtesy of UrbanDigs

Manhattan Leverage Indicator

Elegran’s Leverage Indicator informs us whether the current is a buyer’s or a seller’s market; i.e, which party possesses transactional leverage. Looking at the graph below, this is indicated by the direction of trendlines. Our indicator also informs us regarding the relative strength of that leverage, indicated by the slope of those trendlines. Per below, Manhattan is in the grips of a strong buyer’s market.

The change in the direction of the line between Oct-2022 and Nov-2022 may indicate a transition from a buyer’s market to a seller’s market; however, as one can see from the choppy nature of the data, there are a very large number of false positives

What we can say for certain is that the slope of the curve is now a bit less dramatic (steep), indicating that the strength of the current buyer’s market has waned slightly.

Data Courtesy of UrbanDigs

Price/SF & Discounts

Price per square foot has trended slightly downwards the past few months, yet is still on par with previous highs reached at various points throughout 2015–2017 and 2019.

Chart Courtesy of UrbanDigs

The chart below indicates that listing discounts are still on the rise. This goes hand in hand with the observation that demand is lower than its historical average and also confirms our indicator’s suggestion that the present is a buyer’s market. If it were a seller’s market, listing discounts would be retreating.

What This Means for:

Buyers:

- Due to lower than normal demand, Manhattan continues to be a strong buyer’s market — meaning — buyers should be rewarded for their patience.

- However, nothing lasts forever, and further decreases in mortgage rates should catalyze demand and slowly force the transition from a buyer’s to a seller’s market.

Sellers:

- A buyer’s market suggests that sellers should move forward with haste, but hope is on the horizon with mortgage rates off their highs and the Fed beginning to tap the brakes on rate hikes.

- Sellers, who are betting that prices will strengthen shortly, should consider leasing during the interim as rents have slipped a bit but are still historically very high.

Renters:

- A resistance level was reached over the summer that forced rents to cool. That being said, they’re still very high. But, so too are asking prices and 6.2% mortgage rates still tip the rent-versus-buy scale for many towards leasing.

Investors:

- Mortgage rates have let the air out of leveraged cap rates, but cash buyers can still source opportunities on account of near-record rents.

- On the sell side, a relatively strong USD affords foreign investors, depending on their native currency, the opportunity to realize significant capital gains upon the sale of their asset.

- On the buy-side, the weakening dollar creates opportunities for foreigners to purchase Manhattan real estate and lock-in its notorious stability and potential for price appreciation.