Overall Manhattan Market Update: June 2022

Manhattan Market Update

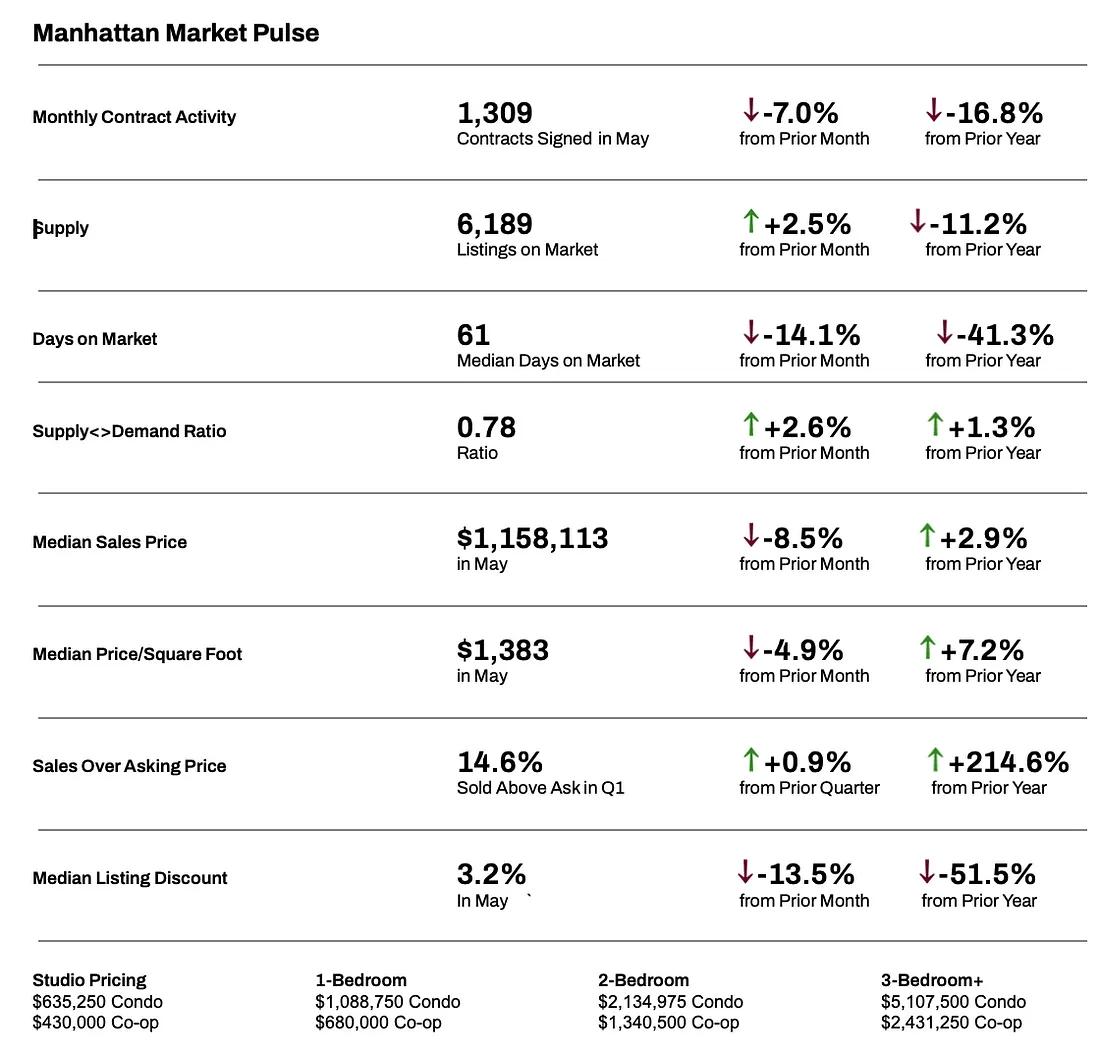

May wraps up the busy spring season for Manhattan Real Estate as Memorial Day marks the unofficial start of summer. March, April, and May are typically the busiest months as measured by contract activity. May 2022, true to the trend, had a relatively high volume of contracts signed (1,309), although it is noticeably lower than last year. Since late April, weekly contract signed volumes in 2022 began falling behind those levels in 2021 by double digits on a percentage basis. This is not surprising, given the off-the-charts and unsustainably high contract volume the market experienced last spring. With rising interest rates, some buyers accelerated plans to purchase, driving up demand now, one reason why homes have sold in nearly two months, with a median which is almost 40% quicker than last spring.

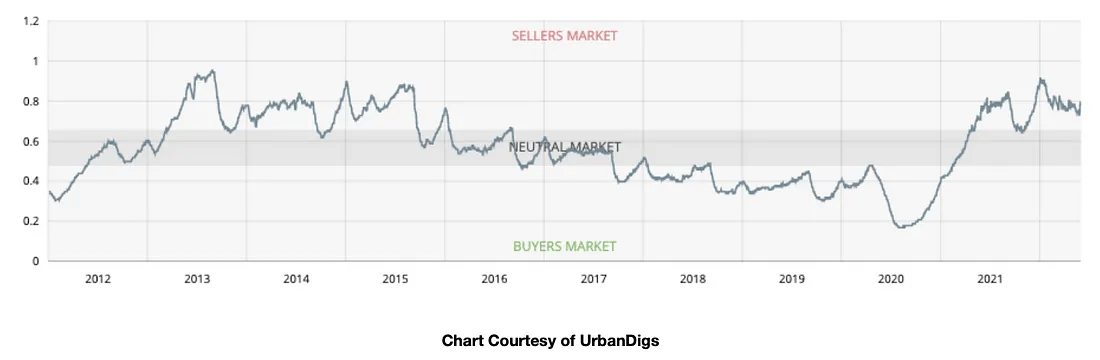

While buyers experienced a very competitive and seller-favored market this spring, indicators are pointing to a more balanced market for the summer months, with buyers likely to experience rising supply [more choice] and decreased competition. The Market Pulse, which is currently at 0.78, continues to indicate that a seller’s market could very likely enter neutral market territory this summer. It’s plausible that buyers can have a window of opportunity this summer to purchase in a less competitive market. Homes that did not enter contract this spring and remain on the market into the summer may be more likely to negotiate, and savvy buyers can find deals with fatigued sellers.

Prices, too, may have hit a short-term high as a result of both the sheer volume of luxury sales in the first five months of 2022 and the strong competition that resulted in bidding wars and little discount. Prices may take a little breather this summer. Prices won’t noticeably fall per se, rather the pace of increase may stall for a few months as the market readjusts to a more normal seasonal market with a traditionally busy March, April, and May, followed by a secondary busy season post-Labor Day and continuing through early November.

While others escape NYC this summer for the summer destination of choice, buyers who remain in NYC can anticipate a little more choice and a less frenzied pace, at least until after Labor Day.

Sellers still on the market need to reassess the competition and check their prices. There is a direct correlation between time on the market and the discount offered. Median listing discounts increase substantially after homes have been on the market for 60 days and then again after 90 days on the market.

While a lot may be changing, what remains the same is that NYC is hyper-local. Even though the aggregate Manhattan market is going through a gearshift, specific micro-markets may already be luke-warm or may be red-hot. Whether you are a buyer or seller, it’s important to speak with your real estate advisor to assemble your game plan.

Manhattan Supply

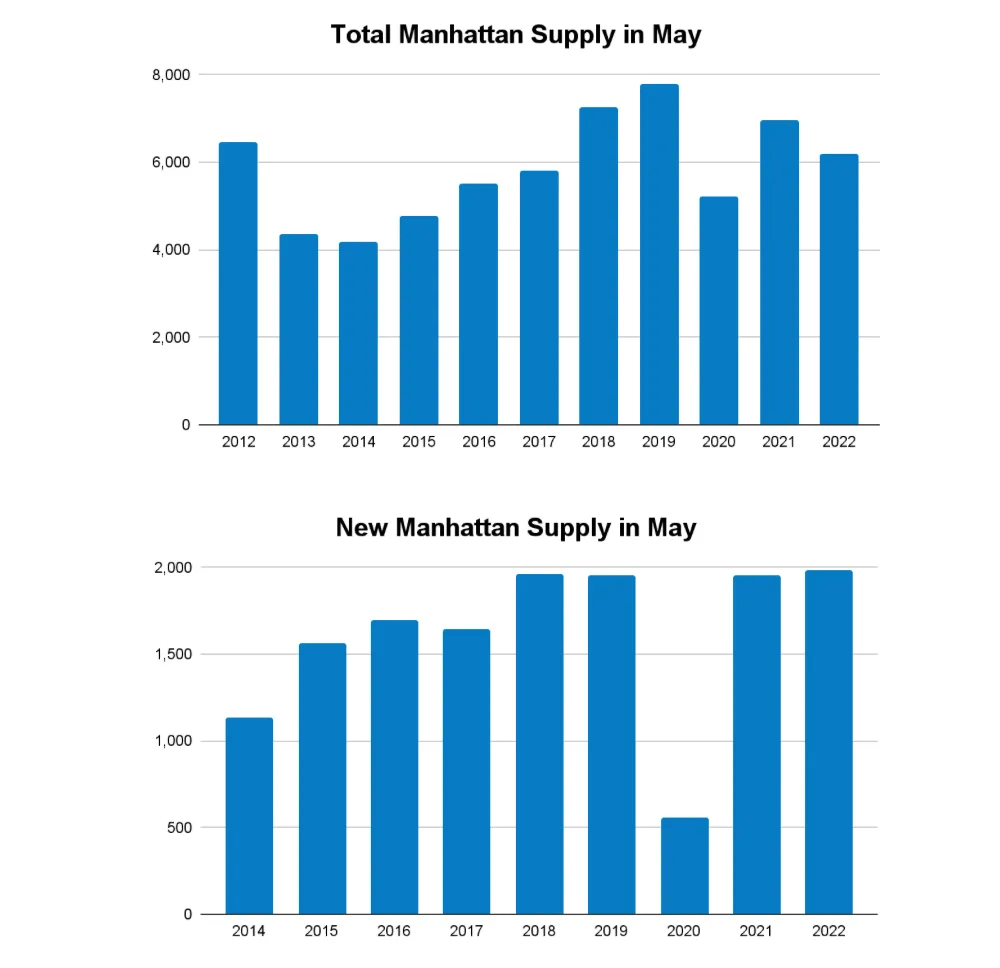

Total supply increased in May as expected, with nearly 2,000 new listings coming to market, increasing total supply by 2.5% to 6,189 units available for sale. The amount of new-to-market supply in May was comparable to levels in May of 2018, 2019, and 2021. While overall supply is still at historically above-average levels, supply remains lower than in 2018, 2019, and 2021 and feels even lower because of the continued above-average level of demand. May traditionally begins the downward trend of monthly new supply, which continues until September. Again, overall supply is kept in check because of the continued strong buyer demand, which is turning the inventory over quickly. Compared to last May, supply is 11% lower this year.

Note: “Total Supply” refers to the amount of inventory on the market at a given time. “New Supply” or “New-to-Market” refers to the amount of new inventory that came on the market in a specific period.

Manhattan Buyer Activity

As measured by signed contracts, although below the record-setting levels seen in May 2021, it remained historically high for May, with 1,309 contracts signed, which is 7% less than in April and 17% lower than in May 2021.

Manhattan’s Market Pulse

[A ratio between pending sales and supply] increased by nearly 3% in May. The current Market Pulse is 0.78, still indicative of a seller’s market, and is at a similar level to this time last year.

A Market Pulse below 0.4 is considered a buyer’s market, a Market Pulse between 0.4 and 0.6 is considered a neutral market, and a Market Pulse above 0.6 is considered a seller’s market.] In a seller’s market, sellers often have more leverage than buyers because demand is greater than supply, resulting in apartments selling quickly, fewer discounts, and increased bidding wars.

Pricing & Discounts

Manhattan prices may have hit a short-term peak in April, as both the median sales price and the median price per square foot decreased in May. With a confluence of rising interest rates, continued stock market volatility, and geopolitical instability, Manhattan’s upward price trends may be taking a breather. Nevertheless, eager buyers to lock in a deal quickly absorbed new-to-market inventory this spring, and the median days on the market decreased to just 61 days in May, a decrease of 14% from the prior month and a decrease of 41% from the prior year.

The Median Sales Price across Manhattan for May was $1,158,113, a decrease of 8.5% compared to April and an increase of 3% compared to last year. On a price per square foot (PPSF) basis, the Median PPSF is $1,383, a decrease of 5% from the previous month and an increase of 7% compared to last year. The median listing discount is currently 3.2% with nearly 15% of homes having sold over the asking price in Q1 2022.

What This Means for:

Buyers:

- The worst may have passed for buyers, as supply is trending upwards and demand is off recent highs; buyers can expect a slightly less-frenzied market this summer and may experience a brief window of opportunity.

- Mortgage rates have stalled after a rapid move higher earlier this spring. An increase in mortgage rates has motivated some on-the-fence buyers to transact sooner.

- It remains vital to work with a trusted mortgage banker or mortgage broker and ensure your pre-approval is up-to-date.

- Prices may have hit their short-term peak and have decreased slightly in the last month. While price appreciation may be taking a breather for a few months, prices are not projected to fall noticeably in the near term.

- Given rising rents and current inflation, buying may make more sense than renting today (with a holding period of 3–5 [or more] years).

Sellers:

- Thinking of listing this fall? The time is now to begin prepping your home to look its best and hit the market shortly after Labor Day.

- Homes sold quickly and with little discount in May. If you plan on coming to the market this summer, price correctly or be prepared to be patient and/or reduce your price.

- Heading into summer, sellers still on the market need to read the market cues and readjust quickly if they are overpriced or mispositioned in the market.

Renters:

- The rental market is as competitive as ever, entering the traditionally busy summer market.

- In May, about 35% fewer leases were signed this year compared to last year, and about 40% fewer apartments came to the market.

- While the overall supply of rental apartments increased by just over 3% in May, seasonal demand increased substantially more than supply, creating even more competition amongst tenants.

- Between existing tenants renewing their leases rather than moving, and a steady flow of recent graduates moving to NYC, the rental market is very tight, resulting in rising rents, lines at open houses, and often multiple applications for apartments.

Investors:

- Rising interest rates should have a more muted effect in Manhattan, as Manhattan is less leveraged than most of America, enabling the NYC market to withstand the pressures of ascending interest rates better than many other national markets.

- Leveraged investors who have a lower interest rate locked in stand to benefit from the inflationary pressures and rising rental rates. Those investors should continue to hold and experience rising cap rates in the years to come.