Brooklyn Market Pulse¹ January 2026

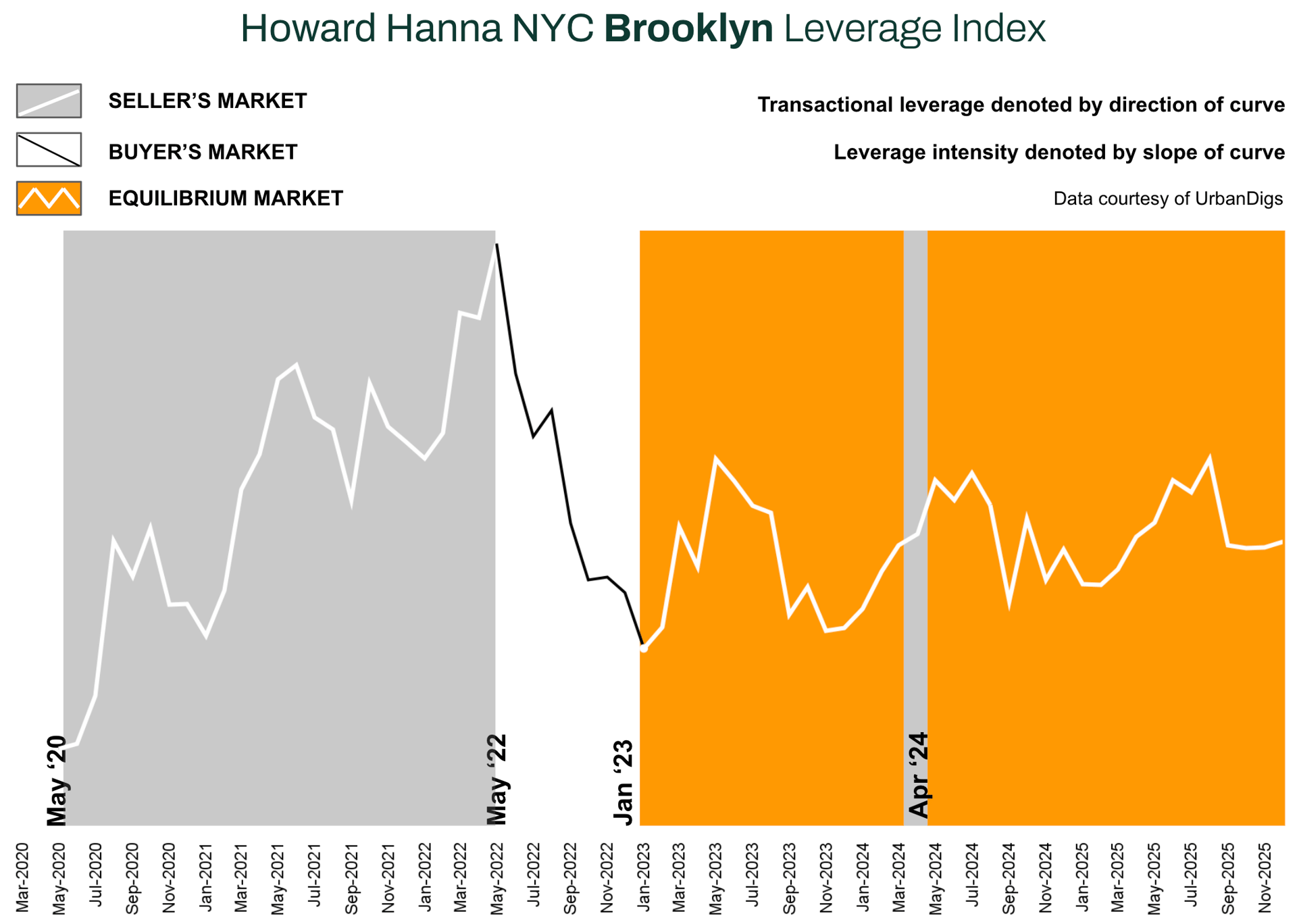

Brooklyn Ends 2025 in Market Equilibrium, With Buyer and Seller Leverage Largely Balanced

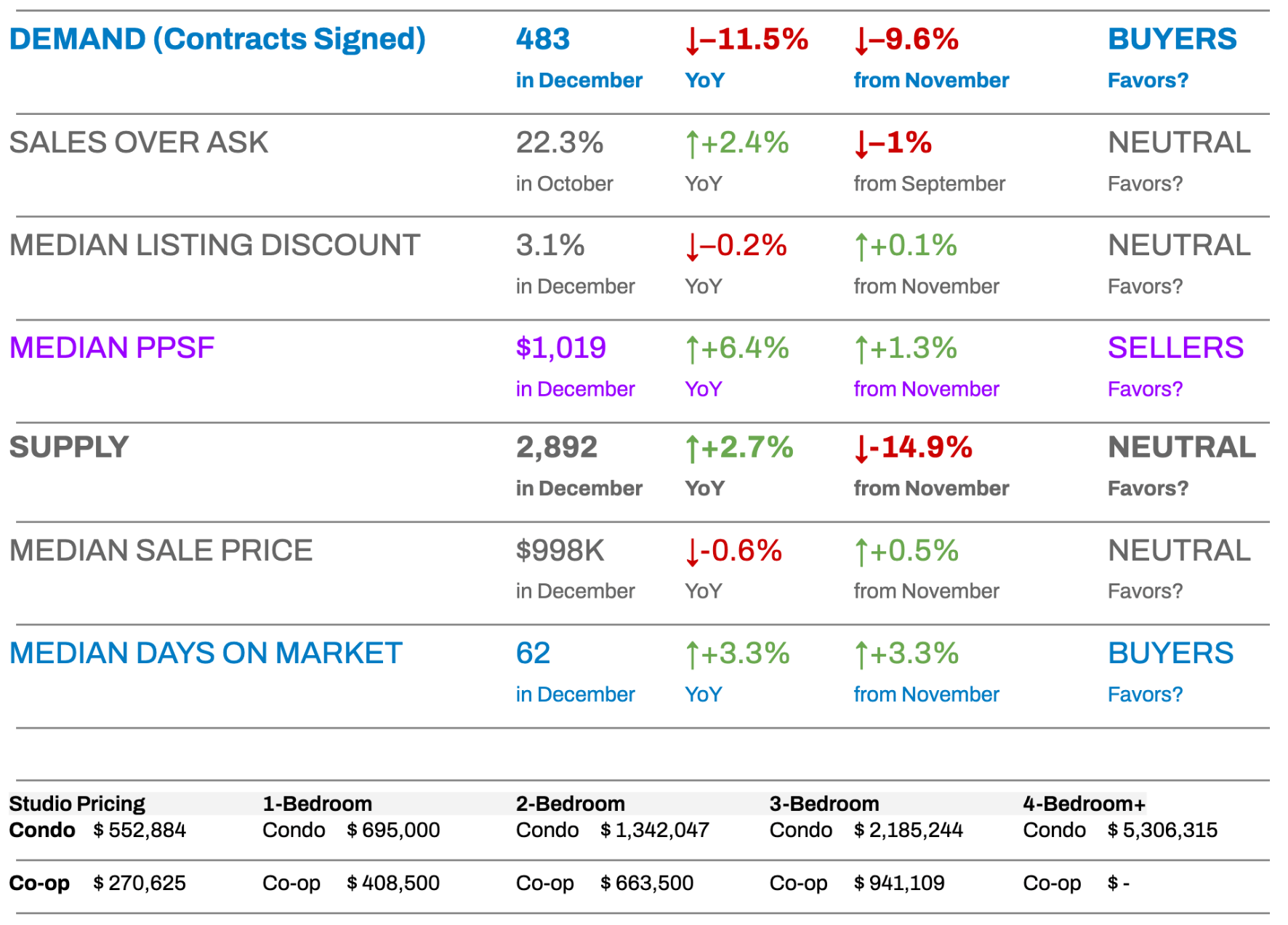

Brooklyn’s residential market closed out 2025 in a largely balanced position, with signs of cooling momentum heading into the new year. Contract activity declined to 483 signed deals in December, down 9.6% from November and 11.5% year over year, reflecting a typical holiday slowdown compounded by elevated borrowing costs. Active inventory fell to 2,892 listings (–14.9% month over month) as many sellers paused listings for the holidays. However, supply remained 2.7% higher than a year ago, giving buyers slightly more choice than last winter. As a result, the Howard Hanna NYC Brooklyn Leverage Index² held in neutral territory, with a modest tilt toward buyers to end the year.

Pricing conditions remain stable. The median sale price was approximately $998K, essentially flat year over year, while the median price per square foot (PPSF) reached $1,019, up 6.4% year over year despite a modest month-over-month pullback. Homes continue to trade close to asking price, with a median listing discount of 3.1%, meaning sellers achieved roughly 97% of list price on average. Market pace has eased slightly, with median days on market at 62, but well-priced listings continue to transact efficiently. Notably, about 22% of sales closed above asking price, underscoring ongoing competition for high-quality properties.

Brooklyn’s rental market remains historically tight. Median rent in November was approximately $3,804, up 8.7% year over year, hovering near record levels. Landlords retain strong leverage, with limited concessions on in-demand units. Meanwhile, mortgage rates, though down from 2025 peaks, remain elevated near 6.3%, reinforcing the ongoing rate-lock effect and limiting resale supply. A key development in December was the Federal Reserve’s 25-basis-point rate cut, signaling a shift toward easing that could gradually improve financing conditions in 2026.

Overall, Brooklyn enters 2026 on balanced footing with a slight buyer tilt. Demand has cooled, inventory is constrained but less so than in Manhattan, and pricing remains firm without signs of overheating. The market continues to reward realistic pricing and disciplined execution, setting the stage for a measured year ahead.

Key Takeaways

-

Buyer activity softened: December contracts fell both month over month and year over year amid seasonal and affordability pressures.

-

Inventory eased seasonally: Listings declined into year-end but remained higher than last year, modestly improving buyer choice.

-

Prices held steady: Sale prices were flat year over year, while PPSF remained meaningfully higher, reflecting 2025’s appreciation.

-

Limited discounts persist: Homes sold close to asking, and bidding wars remain common for well-priced properties.

-

Rents high, rates easing slightly: Rental conditions favor landlords, while modest rate relief may support demand later in 2026.

Outlook for 2026

Brooklyn’s market is expected to remain balanced, with activity picking up gradually after winter. Additional rate relief could bring buyers off the sidelines and encourage more listings, though borrowing costs are likely to stay well above pandemic-era lows. Price growth should moderate, favoring a stable, selective environment rather than sharp moves in either direction.

Photo by Rihards Gederts | Howard Hanna NYC

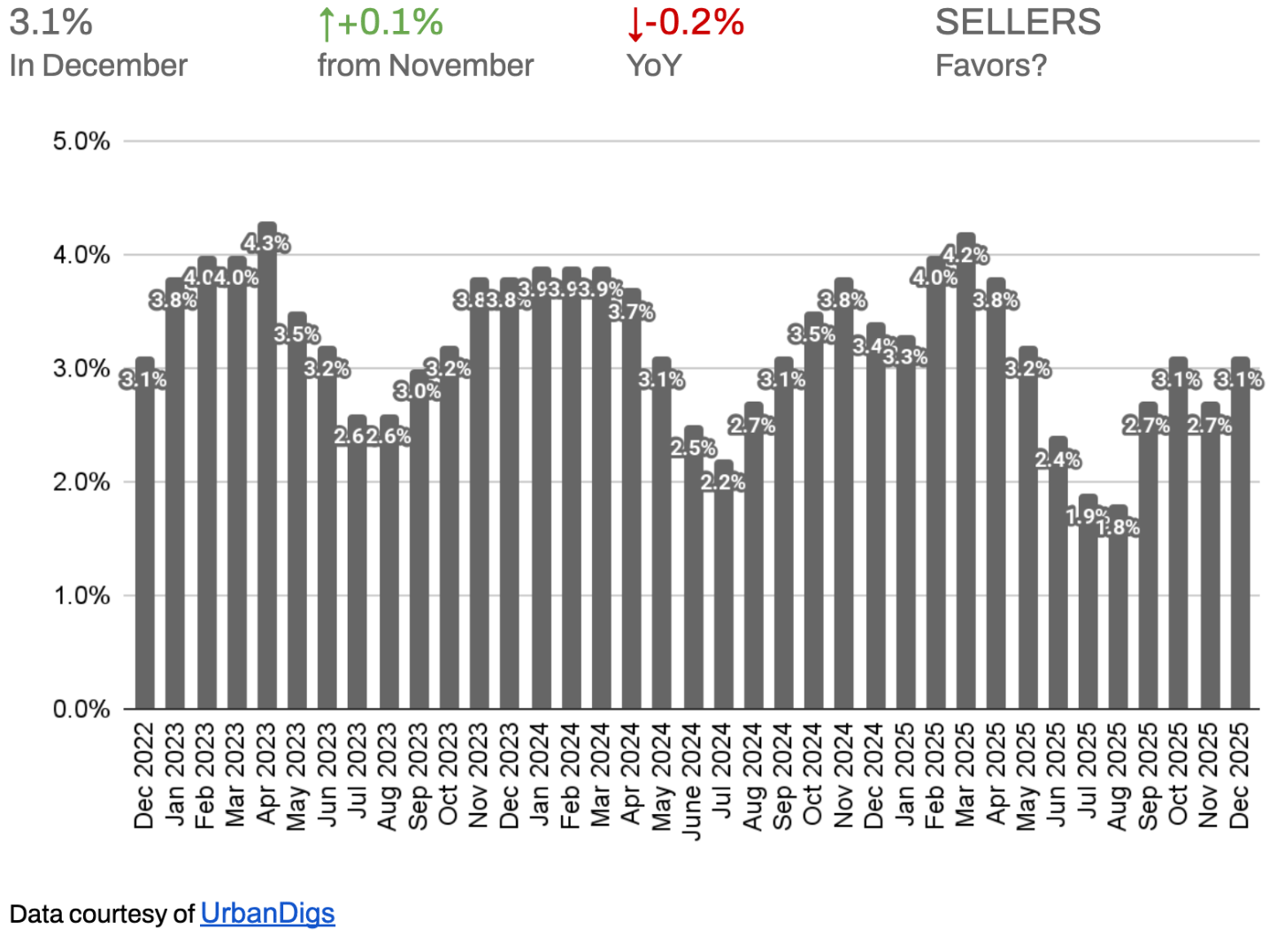

Howard Hanna NYC Brooklyn Leverage Index

The Howard Hanna NYC Brooklyn Leverage Index blends four market signals - supply, demand, median price per square foot, and median listing discount - to capture the balance of power between buyers and sellers.

Direction Matters:

-

An upward-sloping curve = seller’s market

-

A downward-sloping curve = buyer’s market

-

The steeper the slope, the stronger the advantage for either side

December’s Reading: Brooklyn’s index remained effectively neutral at year-end. One of the four components – contract signings (demand) – moved in buyers’ favor (down year-over-year), while two indicators – inventory and listing discounts – held roughly neutral.

Only price per square foot still leaned toward sellers (with values up on both a monthly and annual basis). Overall conditions remained in market equilibrium, with neither side holding a decisive advantage. This mirrors much of 2025, during which the index fluctuated around neutral with only subtle shifts in either direction.

Brooklyn Supply

Brooklyn Supply: Listings Dip for Holidays, Remain Above Last Year

Brooklyn’s active inventory contracted in December, finishing the month with approximately 2,892 listings on the market. This was about a 14.9% decrease from November – a typical pullback as many sellers temporarily withdrew listings during the holidays or waited to list until the new year. However, supply was still up 2.7% compared to December 2024, meaning buyers had a bit more to choose from than a year ago, even with the seasonal dip.

🟥 Buyers: The year-end market offered slim pickings due to the holiday slowdown, but you did have slightly more options than last December. With inventory temporarily low, you might find less competition per listing right now – use this breather to survey what’s available and identify good opportunities.

🟩 Sellers: With many homeowners holding off during the holidays, your listing faces less competition in December. Serious buyers who are active now have fewer properties to consider, which can work to your advantage if your home is priced and presented well.

Outlook: Expect supply to build back up as we head deeper into winter and early spring. Many sellers will likely list in January and February now that the holidays are over, boosting inventory from its current lows. If mortgage rates ease further, we could also see more rate-locked owners finally deciding to sell, adding to supply. Even so, Brooklyn’s inventory in 2026 is likely to remain below pre-pandemic norms.

Brooklyn Demand

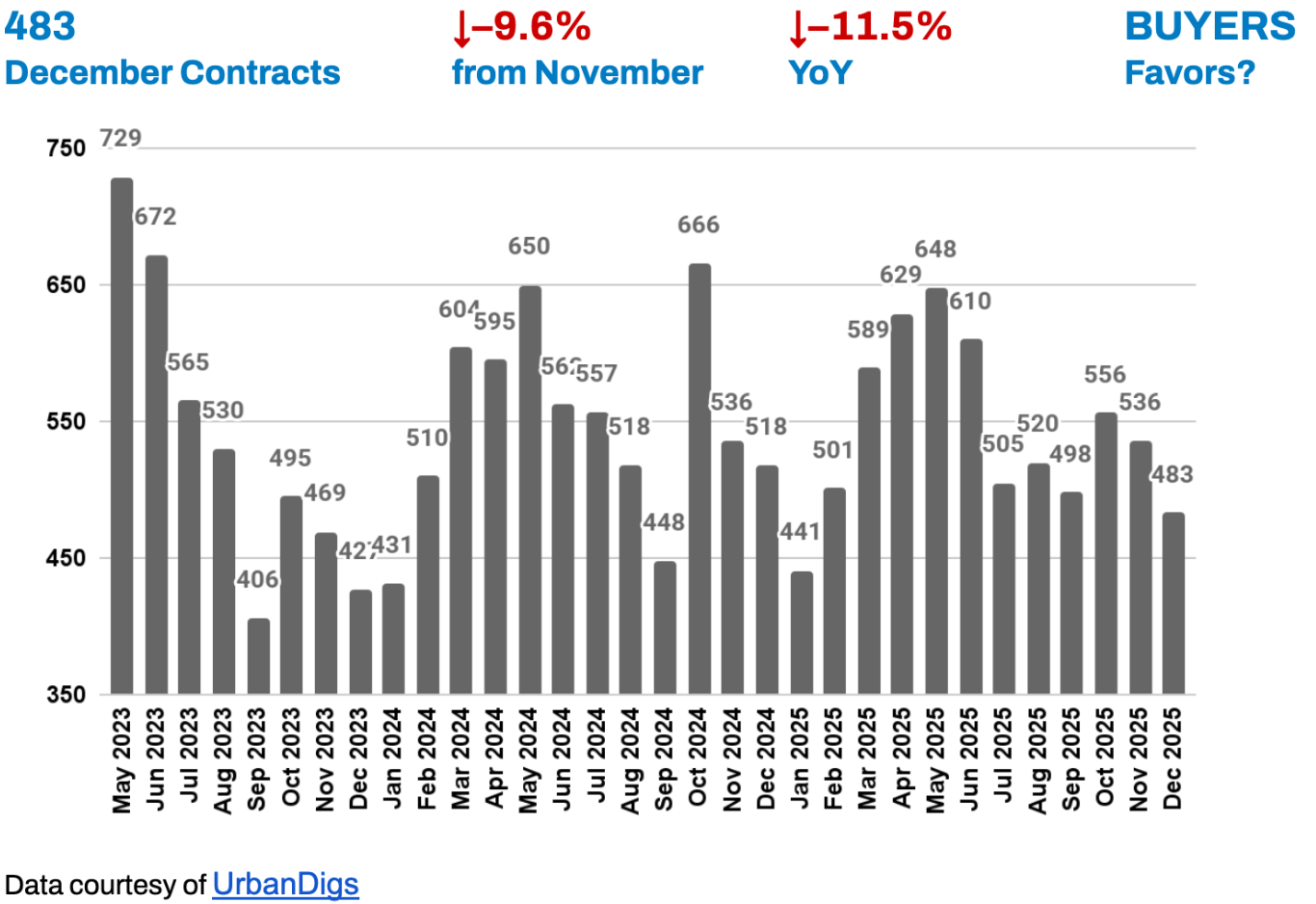

Brooklyn Demand: Contract Activity Eases into Year-End

Buyer demand continued to ease in December. There were 483 contracts signed across Brooklyn during the month, roughly a –9.6% drop from November and about –11.5% fewer deals than in December 2024. This slower pace of contract signings is in line with typical holiday seasonality (many buyers pause their search in late November and December), but it also reflects a more cautious mood compared to the end of 2024, likely influenced by higher interest rates and economic uncertainties.

🟥 Buyers: The slower year-end pace means you’re facing less competition than during the busier spring and fall periods. You may not need to rush into a bidding war this time of year, and if a property you like has been on the market for a few weeks, you likely have room to negotiate on price or terms.

🟩 Sellers: Fewer buyers in the market means you might not see a torrent of offers in late December. Buyer caution is higher now than last year, so an overly ambitious asking price is risky – house-hunters will likely pass on overpriced listings and wait for price drops or the new year’s inventory.

Outlook: Contract volume should rebound as we move into January and February. Many buyers who sat out late fall often re-engage after the holidays, so we anticipate a noticeable uptick in signed contracts in the coming weeks. The big question is by how much – if mortgage rates dip closer to 6% or below, we could see pent-up demand release and a stronger-than-usual winter/spring surge in deals.

Brooklyn Median PPSF

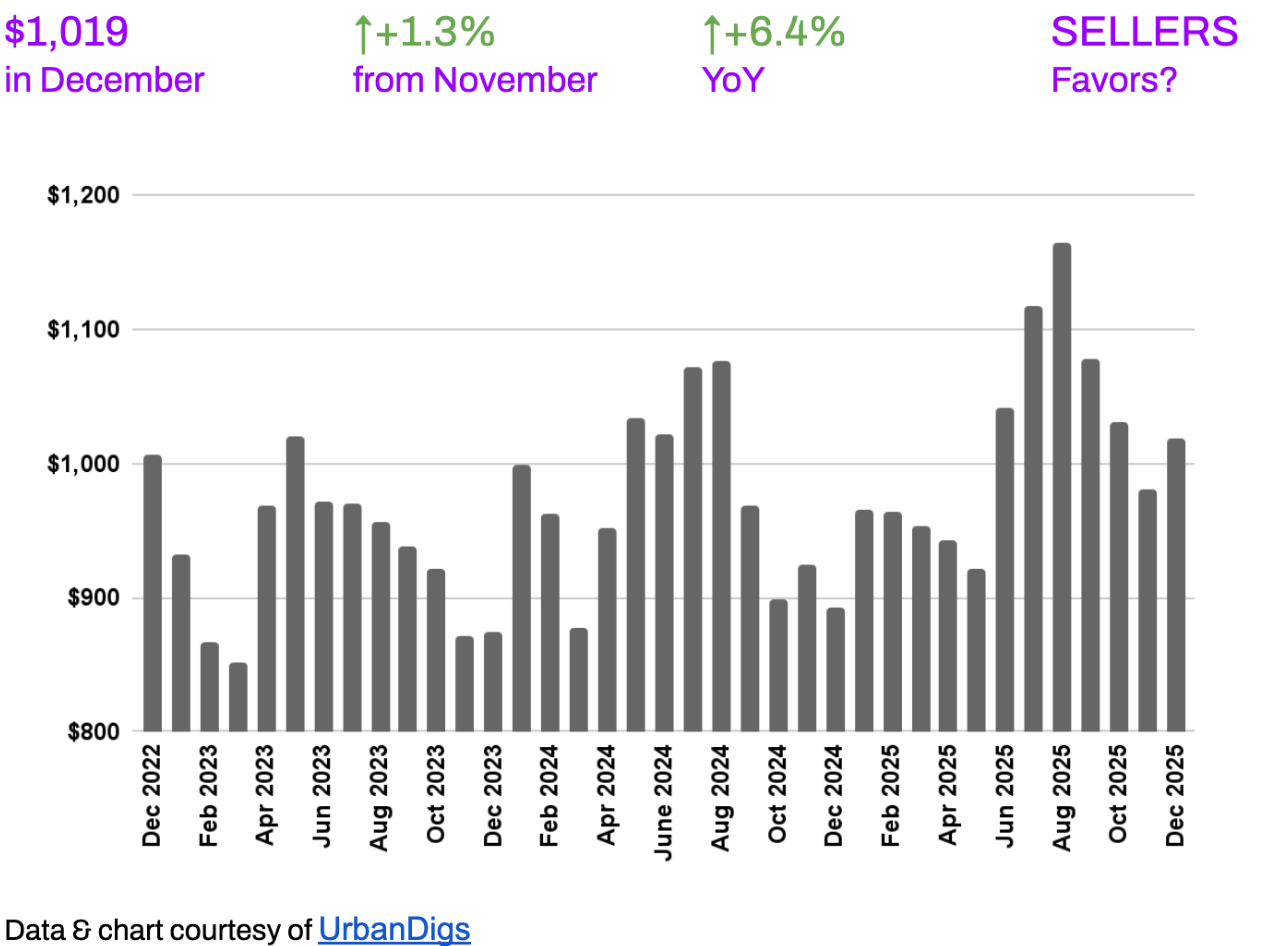

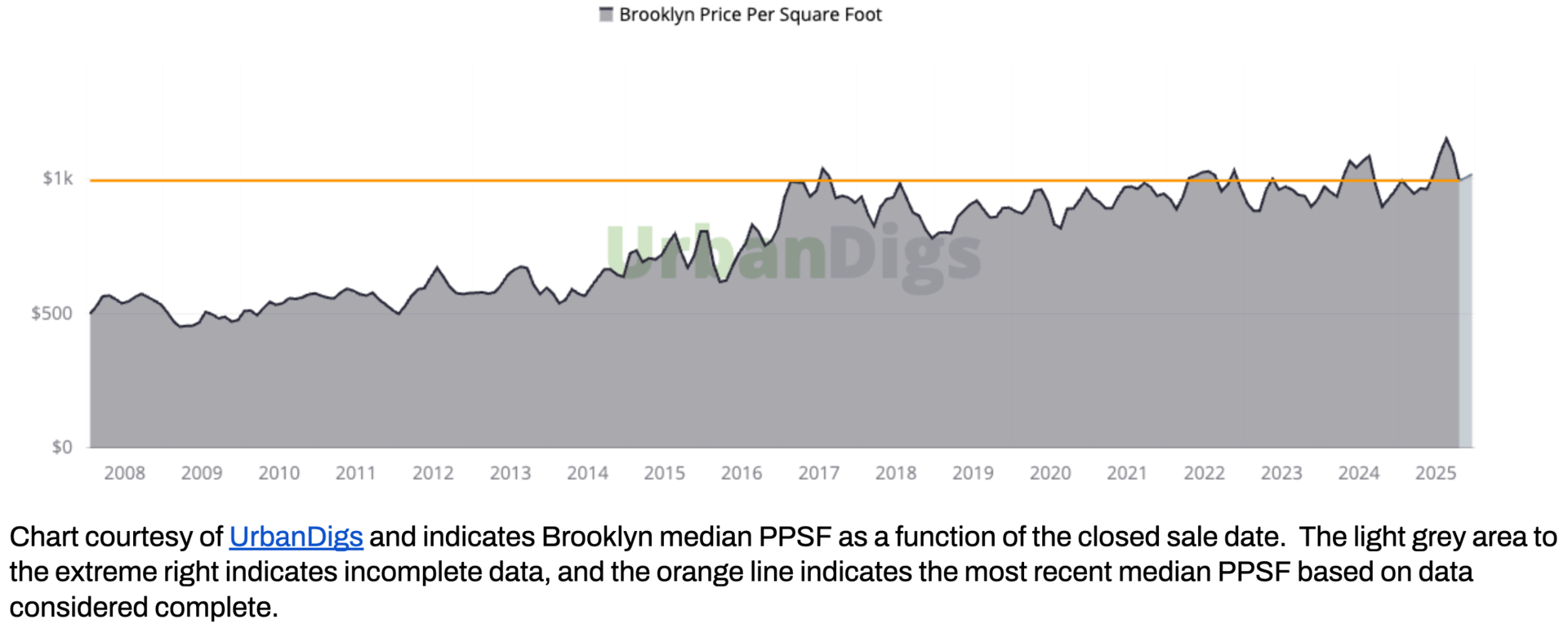

Brooklyn Median PPSF: PPSF Retreats Slightly, Remains Up YoY

Brooklyn’s median price per square foot (PPSF) for closed sales in December was $1,019. This figure edged down about 1.3% from November, indicating a minor price-per-foot cooling at year-end. Even with that dip, PPSF was 6.4% higher than a year ago – a substantial annual gain that underscores how much Brooklyn values climbed during 2025. In essence, prices per square foot are off their peak but still markedly up year-over-year, reflecting that Brooklyn properties appreciated significantly in 2025 despite the recent flattening.

🟥 Buyers: The slight dip in price-per-square-foot is a welcome sign if you’re house-hunting – it means prices are starting to bend in your favor, albeit gradually. You have more negotiating power on price now than you did in the frenzy of mid-2025, so use recent data (like that small month-over-month decline) to inform your offers. Don’t expect huge bargains – remember, PPSF is still up over 6% from last year, and sellers know this.

🟩 Sellers: After a long stretch of rising prices, we’re seeing some resistance at the current price levels. Buyers are much more price-sensitive now, armed with data showing that values leveled off in late 2025.

Outlook: We anticipate Brooklyn PPSF will remain relatively stable going into 2026. With the expectation of slightly higher inventory and steady demand, significant price-per-square-foot jumps are unlikely in the short term. If anything, pricing may oscillate within a narrow range – small dips in one month, slight upticks in another – reflecting a market seeking equilibrium.

Over the course of 2026, any further easing of mortgage rates could bolster buyer budgets and put a bit of upward pressure on PPSF, but concurrently, more listings and new development projects (if any come to market) would add supply and help cap rapid price inflation. In sum, look for moderate, sustainable price trends rather than the double-digit annual gains Brooklyn saw in 2025.

Brooklyn Median Listing Discount

Brooklyn Median Listing Discount: Discounts Narrow, Sellers Hold Firm

In December, the median listing discount – the percentage by which the final sale price lags below the last asking price – narrowed to 3.1% in Brooklyn. This is a slight improvement for sellers compared to roughly 3.3% in November and about 3.3% a year ago (December 2024). In practical terms, a 3.1% median discount means homes are generally selling for about 96.9% of their asking prices.

🟥 Buyers: With average discounts around just 3%, don’t expect deep price cuts in Brooklyn – by and large, sellers are getting about 97% of their list price. The fact that discounts narrowed slightly in December means sellers were even less willing to budge on price than before. What does this mean for you? If you’re serious about a home, you’ll likely need to come in with a strong offer.

🟩 Sellers: Brooklyn is still no bargain bin – most sellers are achieving 97%+ of asking price on average, which is a testament to pricing power if you list correctly. To be among those successful sellers, price your home appropriately from the outset.

Outlook: We expect negotiating dynamics to remain fairly tight in Brooklyn heading into 2026. If buyer demand strengthens in the spring and inventory stays limited, competition could keep listing discounts around these low-single-digit levels or even shrink them further (in competitive bidding situations, some sellers may get full price or above).

Conversely, if inventory grows more than anticipated or the market softens, we might see slightly larger discounts emerge – perhaps moving into the 4% range on average.

Rental Remarks

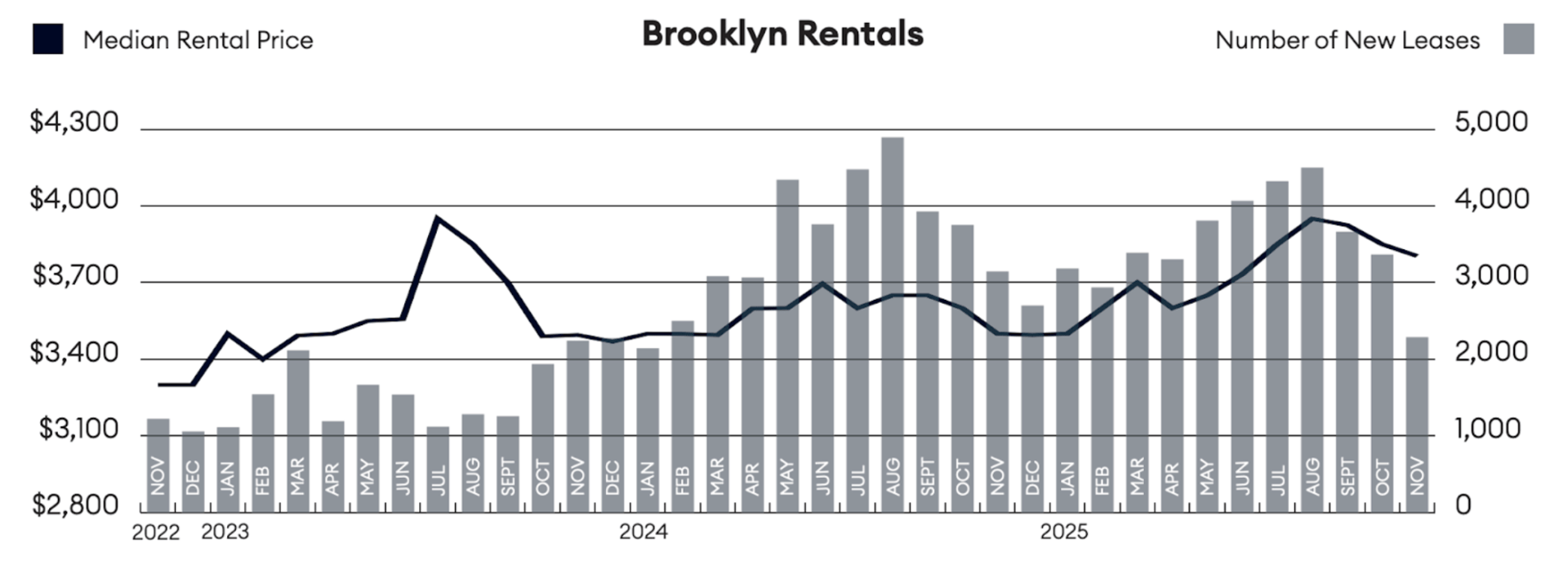

Rents Near Record Highs, Tenants Still Squeezed

Brooklyn’s rental market remained historically tight through late 2025. As of November, the median rent in Brooklyn was approximately $3,804 per month – a 1.2% dip from October but still a hefty 8.7% higher than a year ago³. In fact, rent levels are hovering near all-time highs for the borough. Other price indicators echoed this strength, with robust annual gains across the board. Notably, new lease signings and listing inventory both fell year-over-year, indicating that demand is high and supply scarce.

🟥 Renters: Unfortunately for Brooklyn tenants, affordability has only gotten tougher. Rents are sitting near record levels, and any winter cooling in prices has been minimal at best. Don’t expect generous concessions – things like free month offers or owner-paid broker fees are rare in the current market.

🟩 Landlords: The landlord’s market marches on. You’re likely achieving historically high rents with relatively low turnover, as tenants face few alternatives and are staying put longer. Many listings are drawing multiple applicants, and we’re still seeing instances of bidding above the asking rent, even in what is typically the slow season.

Outlook: The winter months may bring a tiny bit of relief for the rental market, but it’s likely to be short-lived and modest. We might see rent growth pause or even tick down slightly in January/February as demand ebbs during the cold season. However, any downtick will probably be marginal – the fundamental picture hasn’t changed. 2026 is poised to be another landlord-friendly year in Brooklyn.

Mortgage Remarks

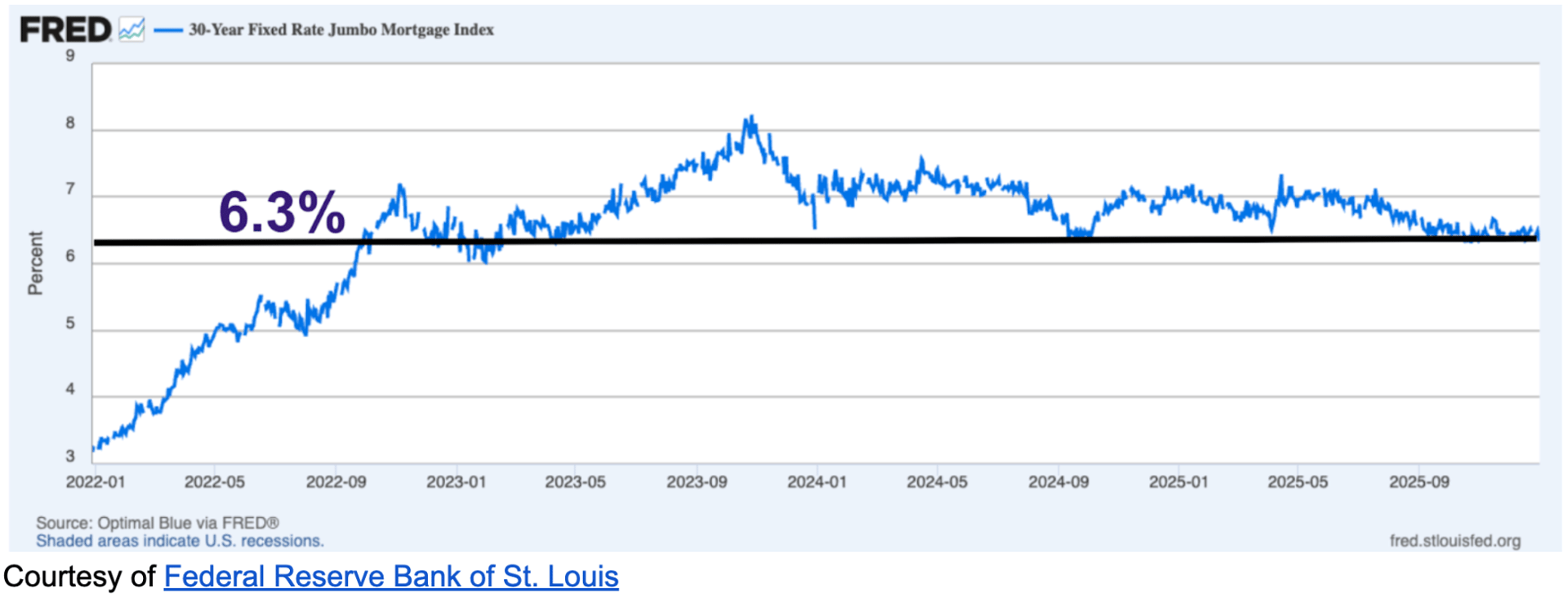

Mortgage Rates: Slight Relief, But “Rate Lock” Effect Lingers

Mortgage rates remain elevated but are drifting lower compared to their 2025 peak. By December, the average 30-year jumbo loan rate hovered around 6.3%⁴, down from the 7%+ highs seen in Q3. Many borrowers with excellent credit even saw quotes in the high-5% range for conforming loans toward year-end. The APR for jumbo loans (which factors in some fees) settled near 6.1%⁵ in December.

This gradual easing of rates has provided marginal relief to buyers’ monthly payments, but let’s be clear: borrowing costs are still significantly higher than the ultra-low 3–4% rates enjoyed during 2020–2021.

One major consequence of sustained ~6%+ mortgage rates is the ongoing “rate lock” effect. A huge swath of homeowners refinanced or bought at those sub-3% rates in the pandemic era; many of them are now hesitant to sell and give up their cheap financing.

This has kept resale inventory tight, as noted earlier. In turn, fewer move-up sellers means fewer new listings, which helps keep home prices supported (even as higher rates simultaneously dampen some buyer affordability). It’s a bit of a stalemate dynamic caused by high rates.

Outlook:

December 2025 brought a noteworthy development: the Federal Reserve cut its benchmark interest rate by 25 bps, bringing the federal funds target range to 3.50%–3.75%. This is the first meaningful step toward monetary easing since mid-2023, and it sets the stage for improved borrowing conditions as we move into 2026. Mortgage rates tend to follow the direction (if not the exact magnitude) of Fed policy over time, so this could foreshadow further relief for home loans in the coming year.

However, buyers should temper expectations – we are unlikely to see sub-5% 30-year mortgage rates again unless the economy enters a downturn or the Fed enacts much larger cuts due to recessionary pressures. Most projections have 2026 mortgage rates averaging in the mid-5% to low-6% range.

Investor Insights

Market Overview: 2025 presented a mixed bag for real estate investors in Brooklyn. On the international front, currency dynamics provided an unexpected tailwind: roughly a 4–5% drop in the U.S. dollar over the past year has made Brooklyn property effectively cheaper for many foreign buyers. For example, a $5 million townhouse or multifamily building now “feels” closer to $4.75M for someone converting from euros, pounds, or yen at today’s exchange rates. This foreign exchange discount, combined with Brooklyn’s appeal as a stable, long-term investment market, has sparked renewed interest from overseas investors.

We’ve noticed an uptick in foreign buyers, particularly targeting luxury condos and townhouses in prime Brooklyn neighborhoods – these global investors are taking advantage of the dollar’s slide and some softness in pricing since the peak, viewing this moment as an opportune entry point into New York’s outer-borough market.

Meanwhile, local (domestic) investors have been more cautious. With mortgage rates for investment properties hovering around 6–7% and rental yields still modest (on the order of ~3–4% in many cases), the math on a traditional condo or co-op investment isn’t terribly compelling right now. Many local investors are finding that, after financing costs, taxes, and common charges, net yields are thin – essentially, the carry costs often outstrip the rental income growth.

As a result, some would-be Brooklyn investors are either holding off or exploring alternative strategies (such as short-term rentals, multi-family properties, or markets outside NYC) where the numbers work out better.

Key Insight: We currently see a somewhat bifurcated investor market in Brooklyn – global capital is active and on the hunt, while local capital remains restrained. International buyers with cash (or favorable financing from abroad) are moving decisively to pick up Brooklyn assets at what they perceive as value prices. In contrast, local investors, who are more dependent on U.S. financing and attuned to thin spreads, are largely sitting on the sidelines unless they find a unique deal. This divergence underscores how macro factors like currency values and interest rates can disproportionately impact different investor groups.

Outlook: Several factors will influence investor activity as we progress through 2026. The Federal Reserve’s policy path is chief among them. If inflation continues to cool and the Fed enacts additional rate cuts, it will hasten the decline of mortgage rates – a big “if,” but certainly one to watch closely. Cheaper financing would undoubtedly bring more investors – both foreign and domestic – off the sidelines. Foreign buyers would benefit from improved leverage on top of currency savings, and more local investors might finally see deals pencil out if borrowing costs come down and/or prices adjust.

References

1. Data courtesy of UrbanDigs

2. According to the Howard Hanna NYC Brooklyn Leverage Index

3. Data courtesy of Miller Samuel, Inc.

4. Data courtesy of Federal Reserve Bank of St. Louis

5. JUMBO mortgage rate APR data courtesy of Bank of America, Chase, and Wells Fargo

6. Cover Photo by Rihards Gederts - Howard Hanna NYC.

If you would like to chat about the most recent market activity,

feel free to contact us at [email protected] or

connect with one of our Advisors.

About Us

Howard Hanna NYC brings the nation’s largest independent and family-owned brokerage to New York City, uniting the strength of a national network with the insight and sophistication of a local firm. Formed through joining forces with Elegran Real Estate, Howard Hanna NYC delivers a seamless, full-service experience backed by more than 15,000 agents across 500 offices in 14 states. The firm’s forward-thinking, agent-first culture continues to shape the future of real estate across Manhattan and the Tri-State area.

Learn more at www.howardhannanyc.com.