Holiday Slowdown Brings Market Back in Balance

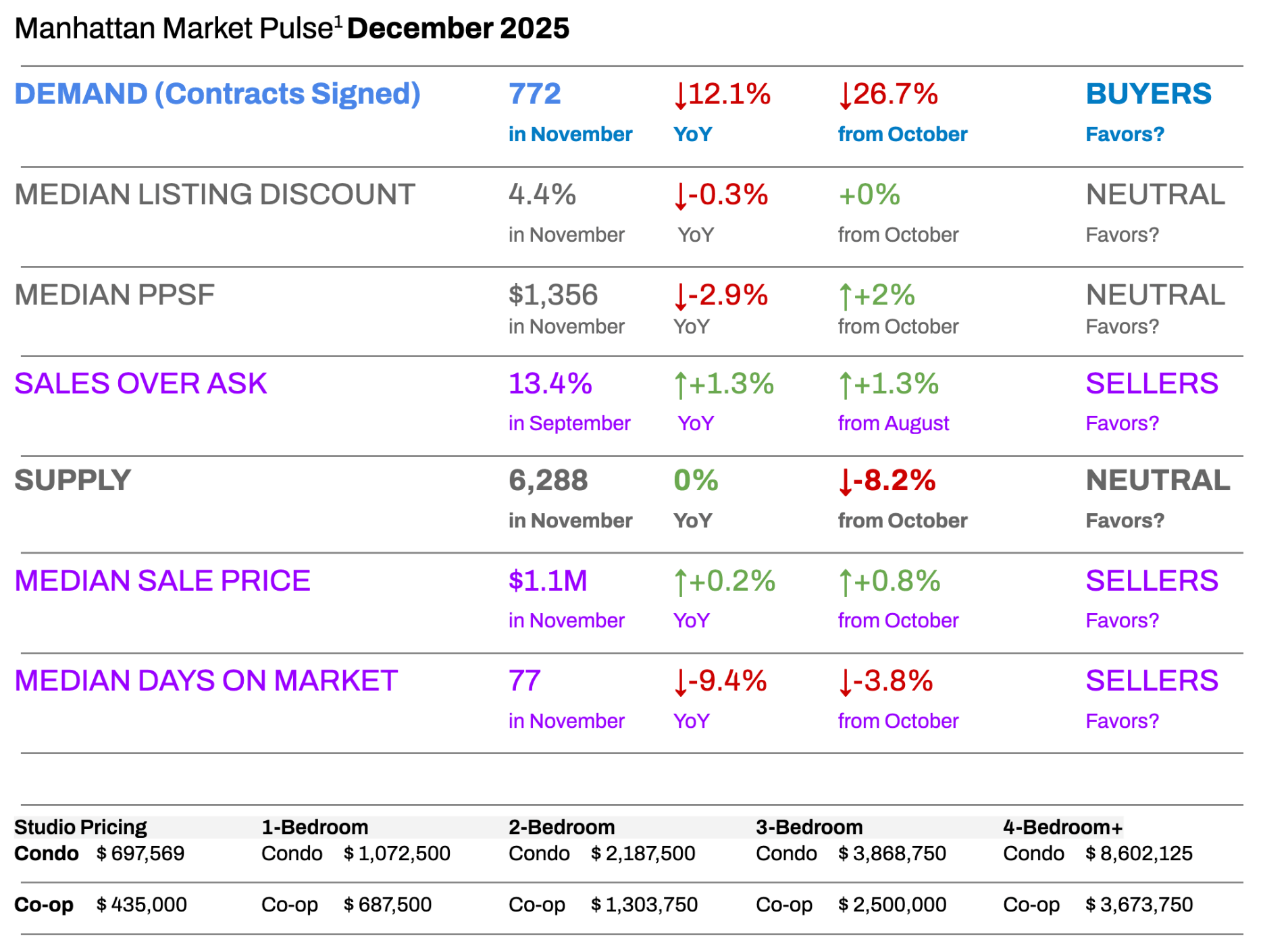

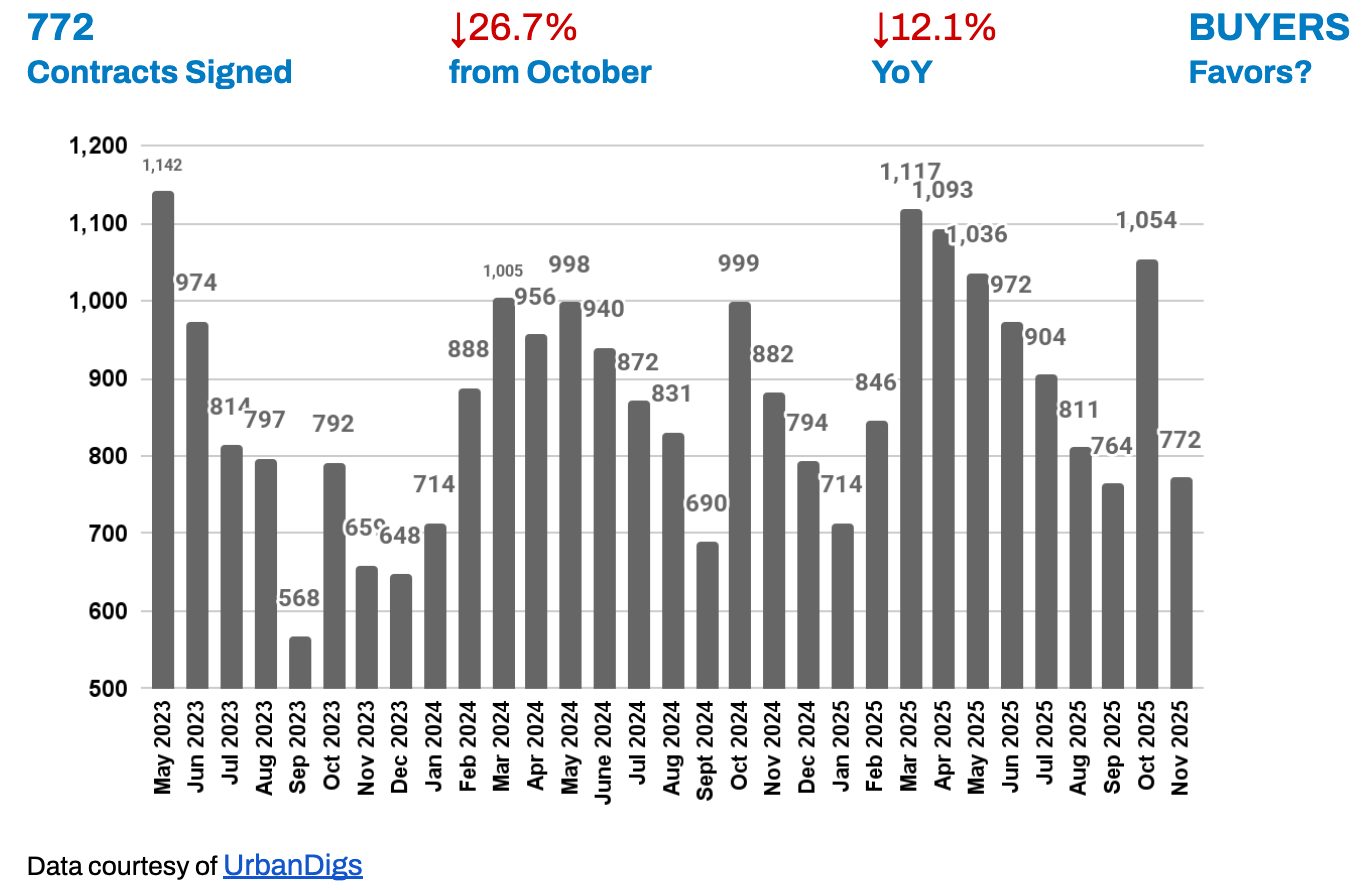

Manhattan’s market cooled in November after October’s burst of activity. Contract signings fell to 772 – a 26.7% drop from the prior month and 12.1% below last year. Inventory also thinned, with active listings dropping to 6,288 (–8.2% month-over-month), leaving fewer options for buyers. This created a more balanced playing field: the Howard Hanna NYC Leverage Index² shifted back to neutral after favoring sellers in October.

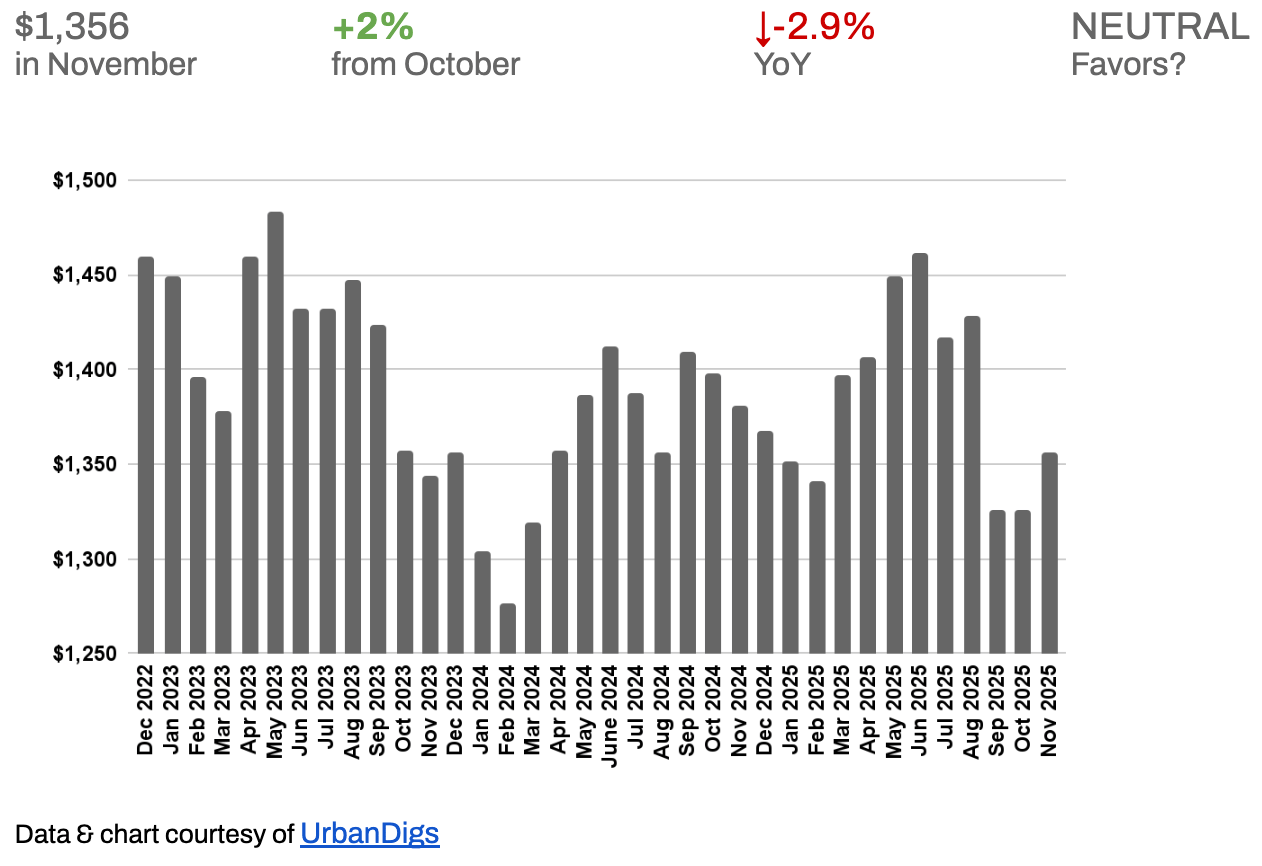

Despite slower sales, pricing stayed firm. Median price per square foot rose 2% month-over-month to ~$1,356 (though still 2.9% below last year). Median sale price held at $1.1M, and days on market shrank to 77. About 13.4% of homes sold above ask, a slight uptick from October – showing that well-priced listings continue to draw competition.

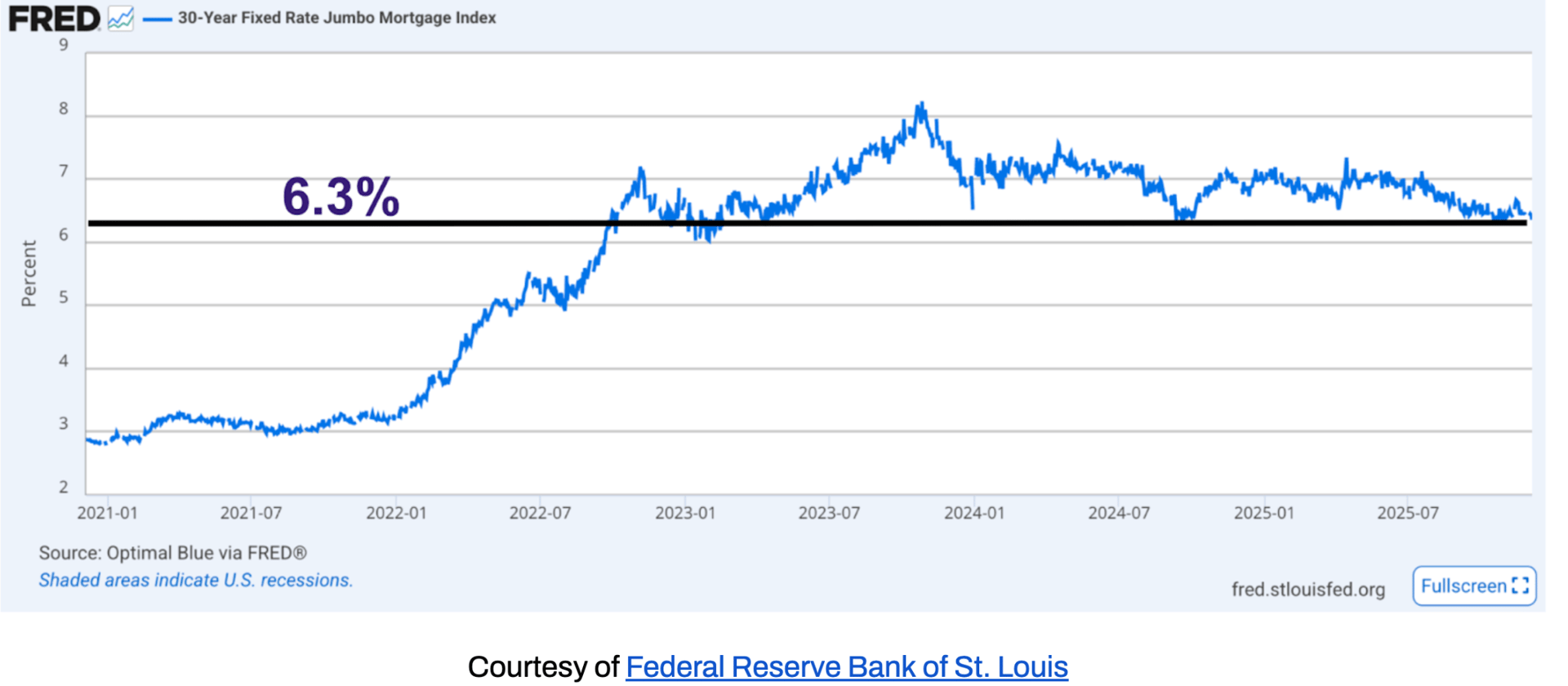

Rents remain near record highs, and mortgage rates, while down from peak levels, remain elevated (~6.3%), keeping many would-be sellers “locked in” and listings low. However, on December 10th, the Federal Reserve lowered its benchmark interest rate to a target range of 3.50%–3.75%, signaling the first meaningful shift toward easing since mid-2023 and setting the stage for improved borrowing conditions in early 2026.

Overall, Manhattan closes out 2025 on stable footing: cooled activity, firm pricing, and tight inventory signal a cautiously optimistic runway into 2026.

Key Takeaways

-

Seasonal cooldown hit demand – contracts dipped sharply post-October, as buyers hit pause ahead of holidays.

-

Leverage Index now reads neutral, reflecting no clear edge for buyers or sellers.

-

Prices held firm – PPSF up 2% MoM; homes are trading at ~95–96% of asking, with low discounts.

-

Rates eased slightly, but affordability remains a headwind. Sellers must price precisely to attract the narrowed pool of serious buyers.

-

2026 setup: modest rate relief (projected ~6% avg) may unlock some sidelined demand, while new city leadership could influence policy sentiment.

Market Outlook for 2026

Manhattan heads into 2026 on steady ground, with expectations of a moderate rebound. The National Association of Realtors projects a 14% increase in existing-home sales and ~4% price growth nationwide, driven by slightly lower mortgage rates and ongoing job gains.

Any drop in rates toward the mid–5% range could reignite demand among buyers sidelined in 2025. Q1 is expected to stay quiet seasonally, but activity may pick up by spring.

Price-wise, expect a stable-to-gently-rising environment. Several key factors – Federal Reserve policy, the new Mamdani administration’s stance on development and affordability, and broader macro trends – will shape market sentiment.

All signs point toward a measured market in 2026: fewer extremes, balanced activity, and continued resilience for those navigating with strategy and insight.

Photo by Rihards Gederts | Howard Hanna NYC

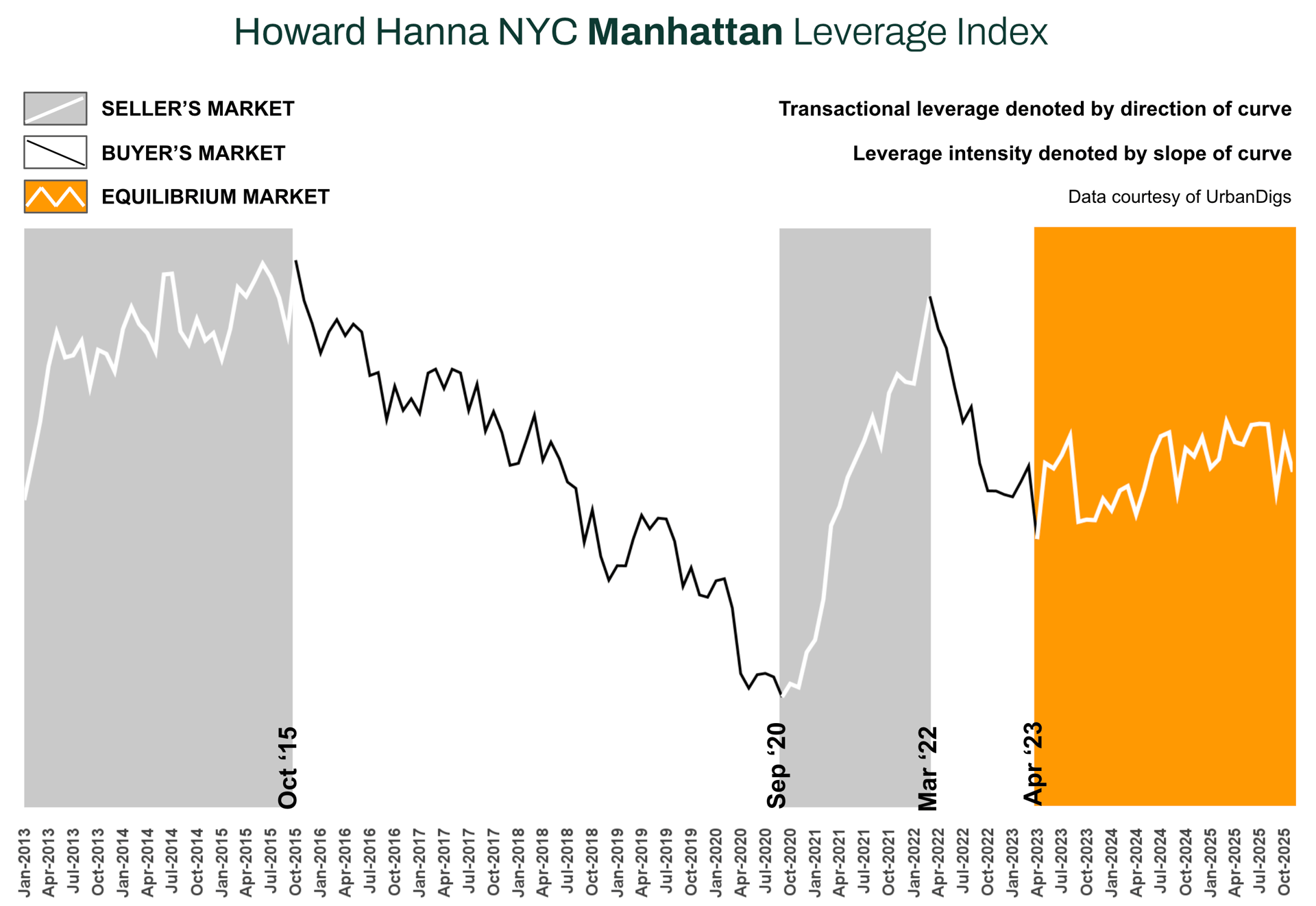

Howard Hanna NYC Manhattan Leverage Index

The Howard Hanna NYC Manhattan Leverage Index blends four market signals - supply, demand, median price per square foot, and median listing discount - to capture the balance of power between buyers and sellers.

Direction Matters:

-

An upward-sloping curve = seller’s market

-

A downward-sloping curve = buyer’s market

-

The steeper the slope, the stronger the advantage for either side

In November, the index ticked downward into neutral territory, indicating no clear advantage for buyers or sellers. This was a pivot from October (which had tilted in sellers’ favor) and reflects the market’s year-end equilibrium. Of the four index components, contract activity pulled back

significantly (a win for buyers), while prices and resale metrics stayed firm (helping sellers).

Supply and discounts lingered around neutral. In effect, the autumn surge in demand dissipated, tempering seller leverage, even as low inventory continued to prevent any buyer’s market. The outcome is a balanced standoff: neither side had a decisive edge as the holiday season set in.

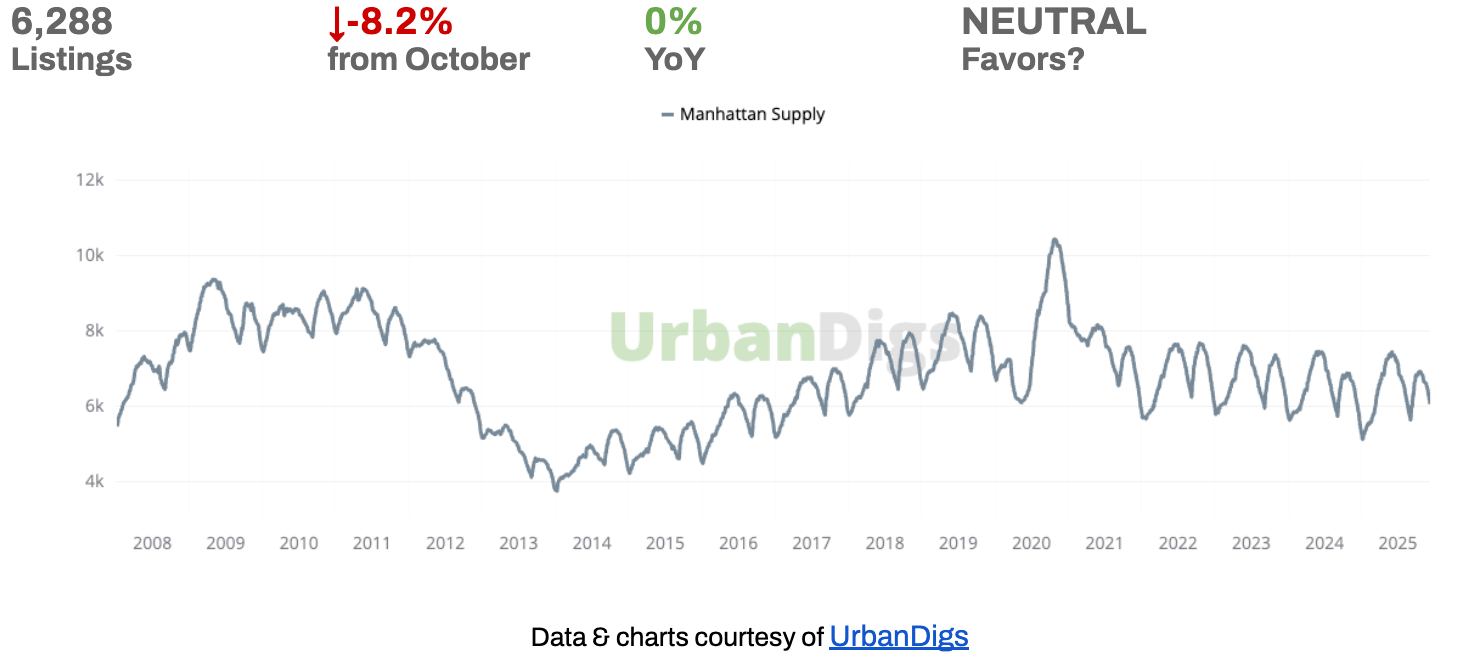

Manhattan Supply

Manhattan Supply: Inventory Tightens Further Ahead of Holidays

Manhattan’s active inventory contracted again in November, ending the month at approximately 6,288 listings (about –8.2% vs. October, and virtually unchanged year-over-year). This sizeable month-over-month drop – coming right before the holidays – means buyers had even fewer options to choose from as winter approached. Many sellers likely pulled listings off the market or delayed new listings until after New Year’s, a typical late-year pattern that was exacerbated by 2025’s high “rate-lock” effect keeping would-be sellers on the sidelines.

🟥 Buyers: Fewer choices, especially in prime locations. Be decisive when a good match appears.

🟩 Sellers: List timing into early Q1 could capture returning demand with limited competition.

Outlook: Many owners locked into ultra-low pandemic-era mortgage rates remain reluctant to sell, which will likely keep supply tight into early 2026. Don’t expect a flood of new inventory in the winter months. Manhattan’s housing stock should stay constrained, a trend that will continue to give diligent sellers a slight edge going into the new year. More listings may emerge by spring, but unless mortgage rates drop substantially, inventory will remain below pre-2020 norms.

Manhattan Demand

Manhattan Demand: Contract Signings Fall in Holiday Lull

Buyer demand contracted significantly in November. There were 772 contracts signed across Manhattan – a steep –26.7% drop from October’s level, and about –12.1% fewer deals than November 2024 This pullback made November one of the slowest sales months of 2025. After October’s unseasonably strong surge in activity, many purchasers hit pause as the holidays approached. The year-end rush to “get in before winter” had largely passed, and what followed was a typical seasonal cooldown (perhaps amplified by buyer fatigue and ongoing affordability challenges).

🟩 Buyers: Pricing power improved in some segments, but competition for quality listings remains.

🟥 Sellers: Listing pace may slow, but serious buyers are still transacting. Preparation and pricing are key.

Outlook: We anticipate a quiet final month of 2025 – December is likely to follow suit with low activity. Big picture: the fact that October’s sales were up year-on-year is a positive indicator for 2026 demand It suggests there’s a lot of pent-up interest that could materialize once conditions improve. Barring any economic shocks, buyer interest should pick back up by the spring of 2026.

Manhattan Median PPSF

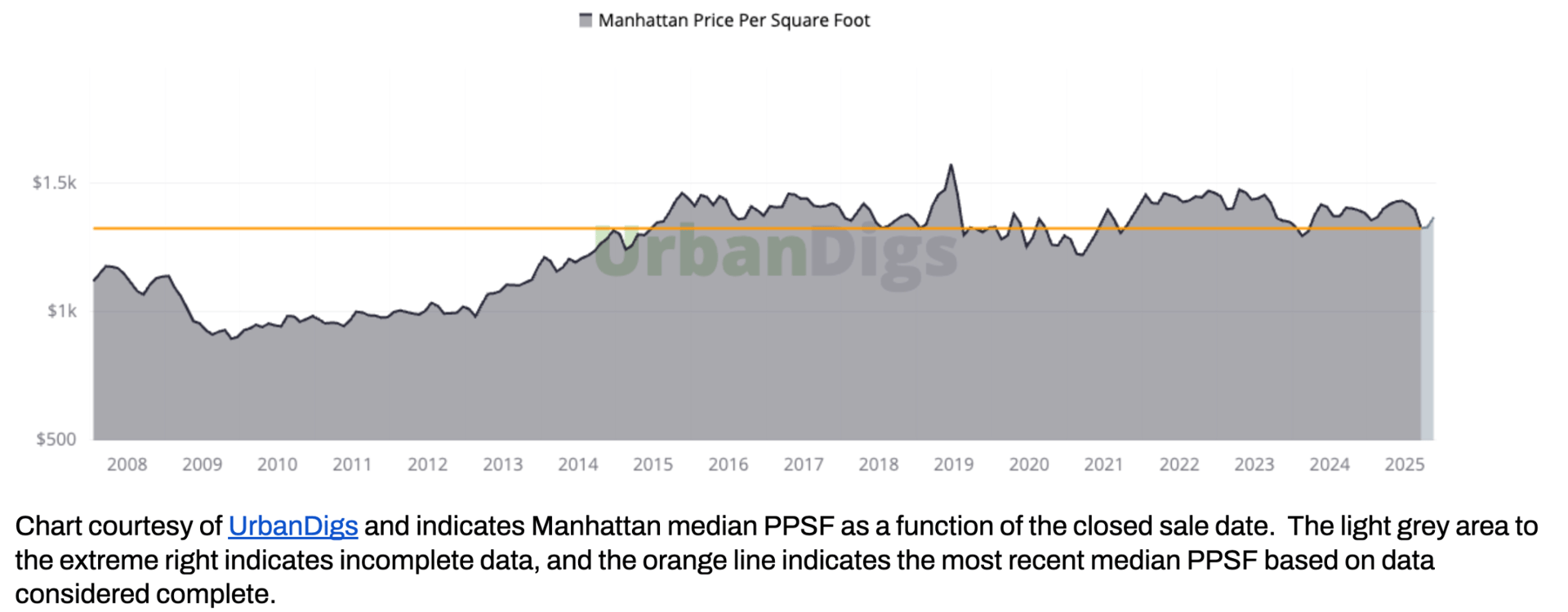

Manhattan Median PPSF: Prices Stay Resilient Amid Slowdown

Manhattan’s median price per square foot (PPSF) held around $1,356 in November, reflecting a ~2% increase from October (and about a 2.9% decrease compared to November 2024). In other words, prices in $/sqft are broadly flat to slightly up month-over-month, and only slightly softer than they were a year ago. This stability, even as sales volume dropped, underscores the market’s resilience on pricing. Heightened demand this fall didn’t send prices soaring, and now the cooler demand hasn’t caused any price collapse either. By and large, sellers have held firm on values and buyers have been willing (or forced) to pay near last year’s pricing, given the limited supply.

🟩 Buyers: The good news is that despite 2025’s ups and downs, prices haven’t skyrocketed. You’re not chasing a fast-rising market. Values are relatively flat and, in some segments, slightly softer than a year ago.

🟥 Sellers: Even with buyer demand pulling back, pricing power remains on your side in many cases. High buyer demand earlier in the fall and ongoing low supply have kept a floor under prices. This means well-priced properties are still selling relatively quickly and close to asking. But today’s buyers are extremely attuned to value – overpricing is the biggest mistake.

Outlook: Many homeowners with ultra-low mortgage rates (sub-3% loans from 2020–21) will likely stay put into 2026, which in turn will keep a lid on inventory and prevent any major price softening in the near term. Manhattan prices thus seem poised to remain remarkably resilient heading into early 2026.

Manhattan Median Listing Discount

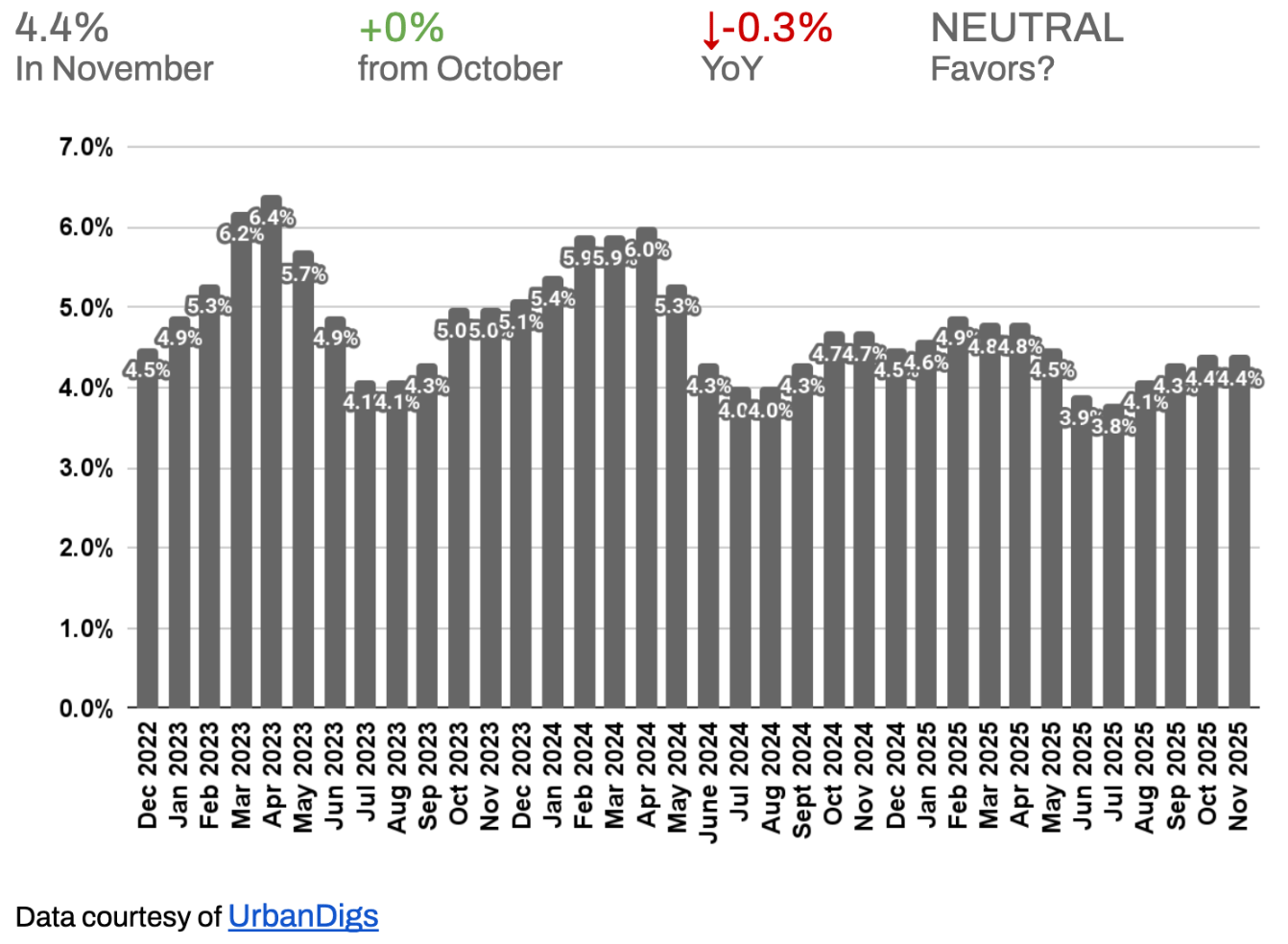

Manhattan Median Listing Discount: Negotiations Remain Balanced

The median listing discount – the percentage difference between the final sale price and the last asking price – held around 4.4% in November. That’s virtually unchanged from October’s ~4.5% level, and even a hair lower than the ~4.7% median discount a year ago. In plain terms, buyers on average paid about 95.5% of the asking price last month. Such a small discount indicates that most properties are still trading very close to their asking prices. There’s little room for deep bargains – sellers, by and large, are pricing homes realistically and not having to concede much to strike a deal.

🟥 Buyers: Realistic pricing holds the line. You have slightly more negotiating power now than you did in the ultra-competitive market of early 2025. On average, paying about 4–5% below a home’s asking price is the norm today.

🟩 Sellers: Value can be found in stale or over-ambitious listings. What it also means: if you overprice your home well above market value, buyers will likely ignore it, and you could end up having to do a much larger price reduction later to re-attract interest. In the current climate, it’s far better to price at the market and negotiate a minor 2-5% concession, than to price 10% high and watch your listing stagnate.

Outlook: Mild price growth with limited discounting through early Q1 2026. We anticipate that listing discounts will remain in this balanced range through the winter. Unless there’s a major change in supply or demand dynamics, there’s little reason to expect either a buyer-favorable surge in discounts (e.g. average discounts widening to 8% – unlikely without a market downturn) or a seller-favorable shift back to bidding wars (lots of sales over ask – unlikely without a flood of buyers). Heading into 2026, the negotiation playing field should stay relatively level – essentially a continuation of the “near-ask” deal-making we’re seeing now.

Rental Remarks

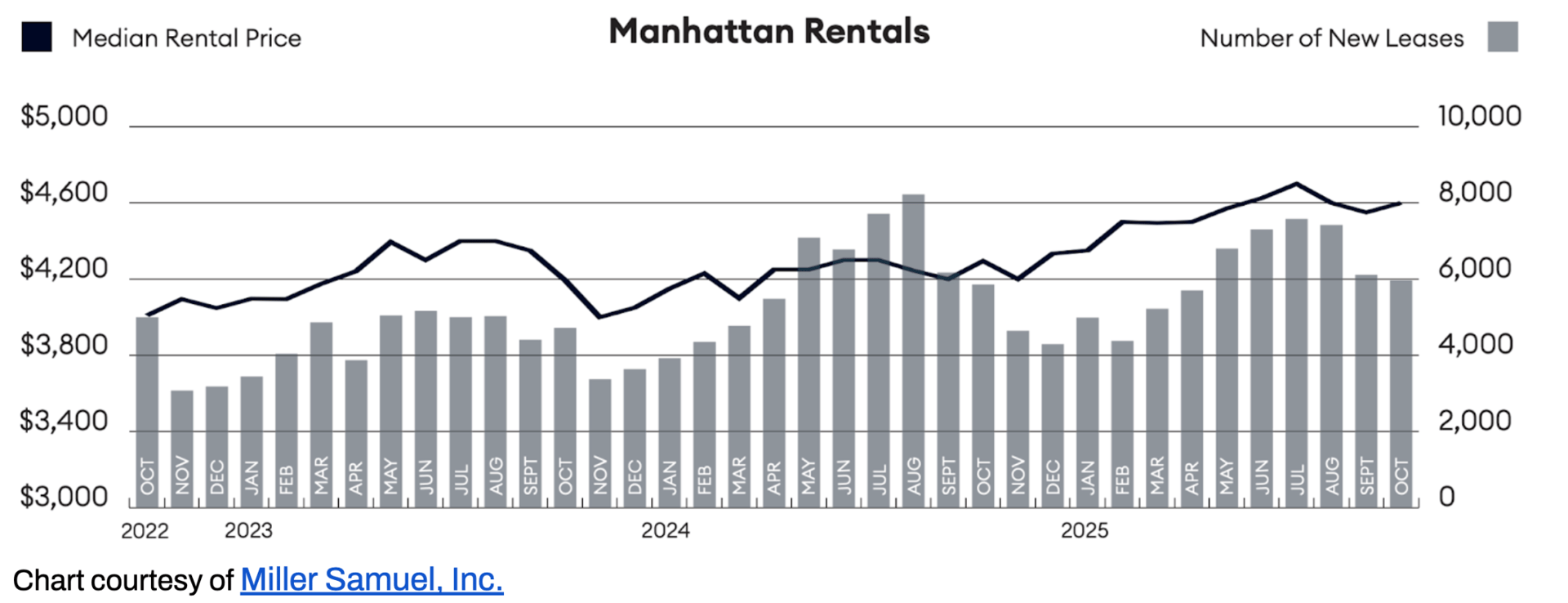

Rental Market: Rents Near Record Highs, Tenants Feel the Squeeze

Median rent rose to $4,600 (↑1.1% MoM, ↑7.1% YoY)³ - the third-highest on record. New lease signings edged up modestly, while vacancy declined for the seventh straight month. All of this points to continued landlord leverage – there are far more renters looking than there are apartments available. In fact, bidding wars haven’t disappeared: roughly 1 in 5 rental listings is still renting for above the asking price, even as we head into winter

🟥 Renters: Prices remain elevated. Incentives are rare.

🟩 Landlords: High demand + low vacancy = strong retention and pricing leverage.

Outlook: Seasonal slowdowns may offer slight relief in January, but demand fundamentals remain firm. In all likelihood, high rents and tough competition will persist into 2026. Renters should plan their budgets accordingly (don’t bet on a big price drop), and landlords can look forward to another strong rental season once the weather warms up. The wild card to watch is local housing policy – any new regulations from the incoming city administration around rent stabilization or tenant protections could slightly alter the dynamics, but absent immediate changes, 2026 will begin much like 2025 ended: with landlords firmly in control of a very pricey, very competitive rental landscape.

Mortgage Remarks

Mortgage Rates: Slight Rate Relief, But the “Rate Lock” Effect Lingers

Rates remain elevated but are drifting lower. December jumbo loans average ~6.3%⁴, down from Q3’s 7%+ peak. The jumbo APR settled near 6.1⁵ percent in November. The “rate lock” effect persists, keeping many would-be sellers off-market. Buyer demand is weakening as affordability pressures mount, driven by elevated prices, higher mortgage rates, and softer immigration flows. These dynamics are slowing transaction activity, yet tight inventory continues to keep prices elevated.

Outlook: On December 10th, the Federal Reserve lowered its benchmark interest rate to a target range of 3.50%–3.75%, signaling the first meaningful shift toward easing since mid-2023 and setting the stage for improved borrowing conditions in early 2026. Don’t expect sub-5% rates without a recession.

Investor Insights

Market Overview: 2025 presented a mixed bag for real estate investors in Manhattan. On the international front, currency dynamics provided a tailwind: roughly a 4–5% drop in the U.S. dollar over the past year has made Manhattan property effectively cheaper for many foreign buyers. A $5 million apartment now “feels” closer to $4.75M for someone converting from euros, pounds, or yen at today’s rates. This forex discount, combined with Manhattan’s perennial appeal as a stable, long-term investment, has sparked renewed interest from overseas. We’ve seen an uptick in foreign buyers, particularly targeting luxury condos and new developments in prime areas.

These global investors are taking advantage of the dollar’s slide and some softness in Manhattan luxury prices since the peak; for them, this is an opportunistic entry point into a market that they view as a safe haven.

Meanwhile, local (domestic) investors have been more cautious. With mortgage rates hovering ~6–7% for investment loans and rental yields still modest (~3–4%), the math on traditional condo/co-op investment isn’t terribly compelling. The carry costs remain high, and pure cash-flow plays often don’t pencil out unless bought at a significant discount.

As a result, many New York-based investors are either sitting on the sidelines or getting creative: focusing on long-term value-add opportunities (like buying and renovating properties, or looking for distress deals) and seeking improved cash-on-cash returns through repositioning assets. We’ve also seen continued interest in multi-family or mixed-use properties where investors can add value. But generally speaking, leverage is expensive, so highly leveraged speculative buys have been scarce. Local players are waiting for either financing costs to come down or for prices to soften enough to juice future returns.

Key Insight: We currently have a somewhat bifurcated investor market – global capital is moving actively, while local capital is more restrained

Outlook

Several external factors will bear watching as we look ahead. The Federal Reserve’s policy path is chief among them; if inflation continues to cool, the Fed could make additional rate cuts, hastening the decline of mortgage rates (a big “if,” but one to watch closely). Conversely, any resurgence in inflation or other economic shock could keep borrowing costs high.

The local political climate is another: 2026 will see the new Mamdani administration’s housing policies start to take shape. Any moves on rezoning, development incentives, or rent regulations could impact investor sentiment and development pipelines.

Early indications are somewhat reassuring for the industry – pro-development ballot measures passed in November, and despite a populist campaign tone, the incoming mayor has shown signs of pragmatism in his personal votes – but only time will tell how that translates into policy. Global factors like foreign investment trends and currency fluctuations will also remain in play (e.g., will the dollar stay weak, continuing to attract overseas buyers, or will it strengthen and slightly dampen that segment?).

All told, Manhattan enters 2026 on steady ground. The extremes of the pandemic-era market are behind us; what lies ahead appears to be a period of measured activity and balanced conditions.

References

1. Data courtesy of UrbanDigs

2. According to the Howard Hanna NYC Manhattan Leverage Index

3. Data courtesy of Miller Samuel, Inc.

4. Data courtesy of Federal Reserve Bank of St. Louis

5. JUMBO mortgage rate APR data courtesy of Bank of America, Chase, and Wells Fargo

6. Cover Photo by Rihards Gederts.

If you would like to chat about the most recent market activity,

feel free to contact us at [email protected] or

connect with one of our Advisors.

Howard Hanna NYC brings the nation’s largest independent and family-owned brokerage to New York City, uniting the strength of a national network with the insight and sophistication of a local firm. Formed through joining forces with Elegran Real Estate, Howard Hanna NYC delivers a seamless, full-service experience backed by more than 15,000 agents across 500 offices in 14 states. The firm’s forward-thinking, agent-first culture continues to shape the future of real estate across Manhattan and the Tri-State area.Learn more at www.howardhannanyc.com.