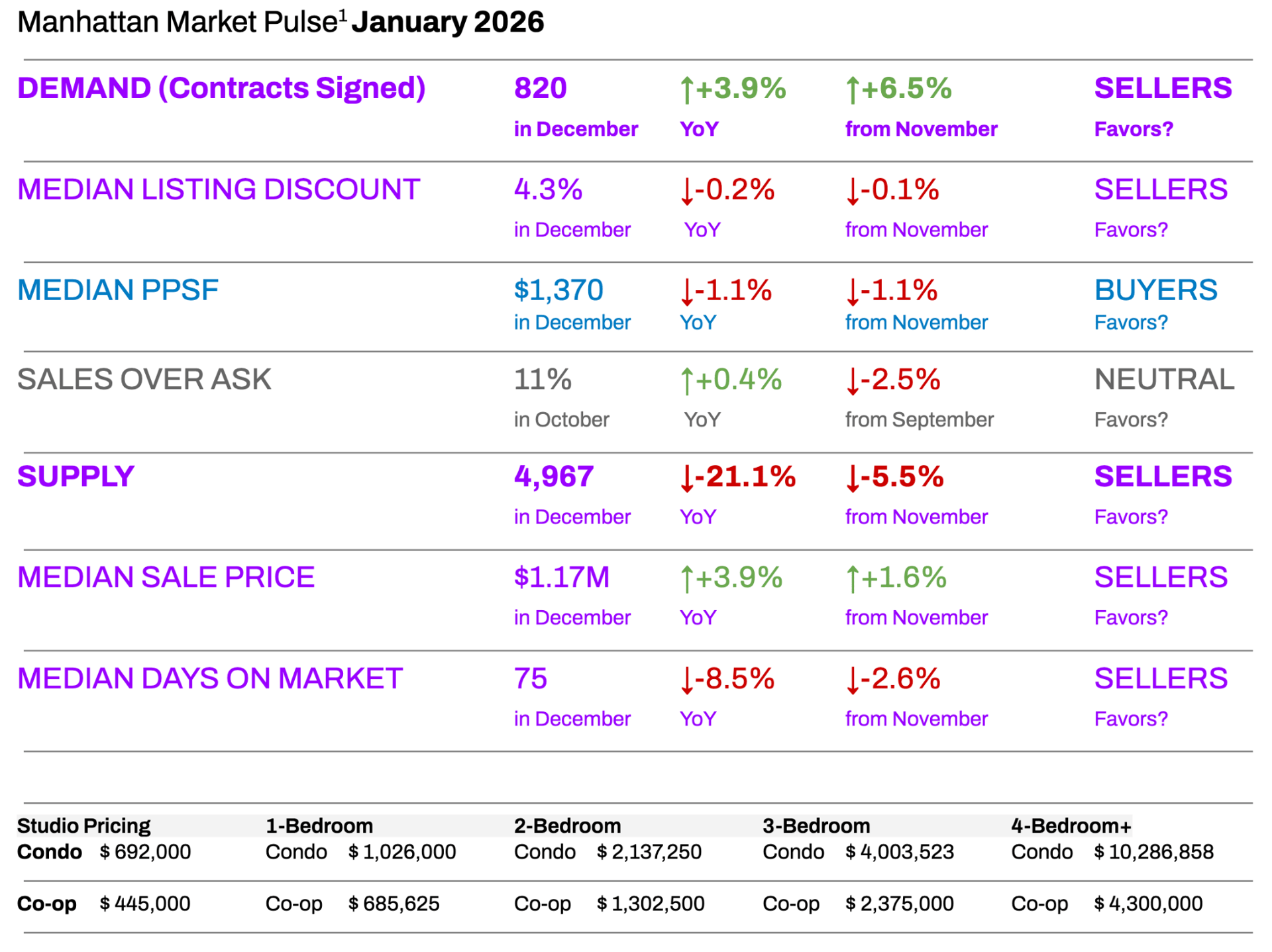

Manhattan Begins 2026 With Strong Demand and Shrinking Supply

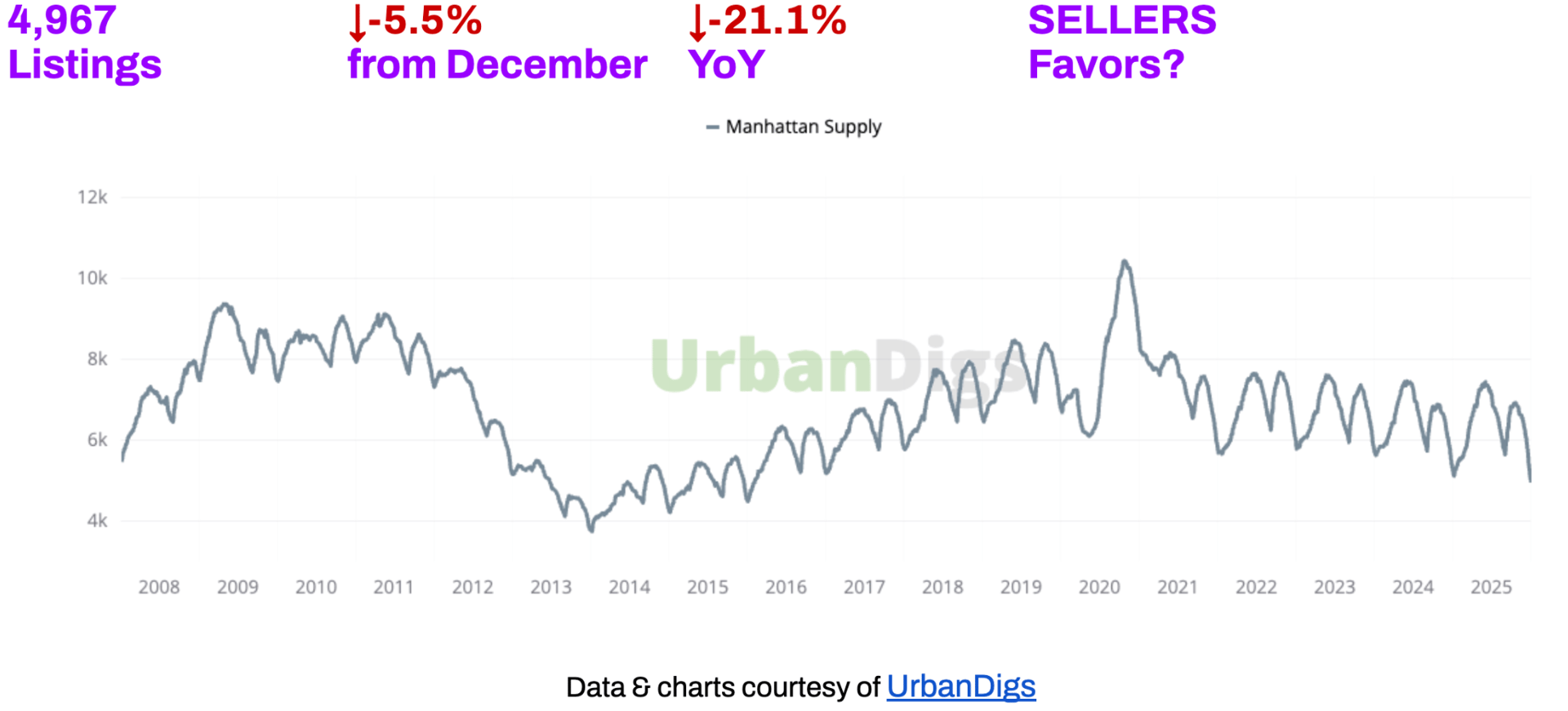

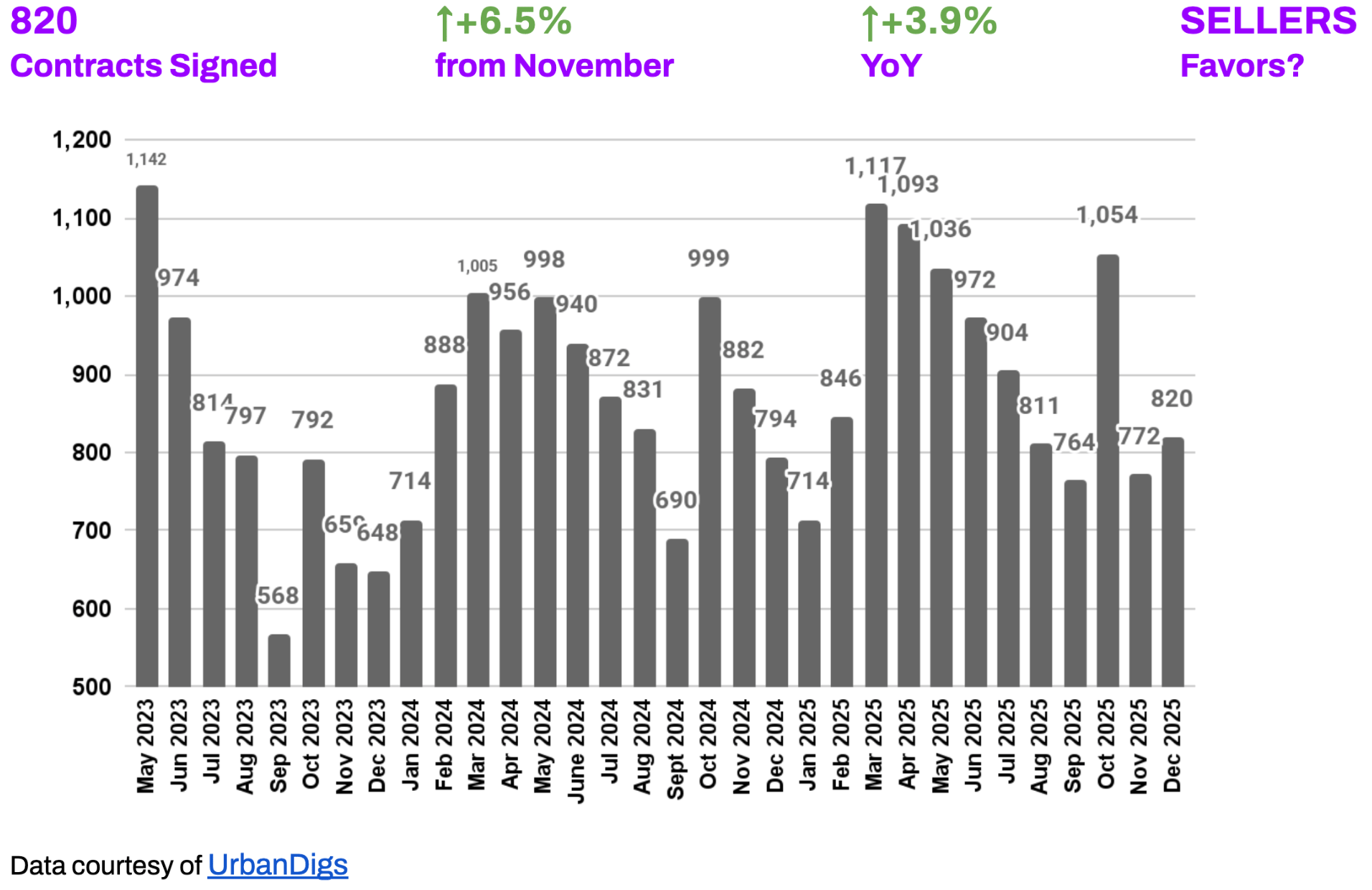

Manhattan’s residential market closed 2025 with renewed momentum, setting a constructive backdrop for the start of 2026. Contract activity increased to 820 signed deals in December, up 6.5% month over month and 3.9% year over year, signaling a return of buyer engagement following the seasonal November slowdown. At the same time, active inventory declined to 4,967 listings, representing a 5.5% monthly drop and a 21.1% year-over-year contraction, leaving supply near recent cyclical lows.

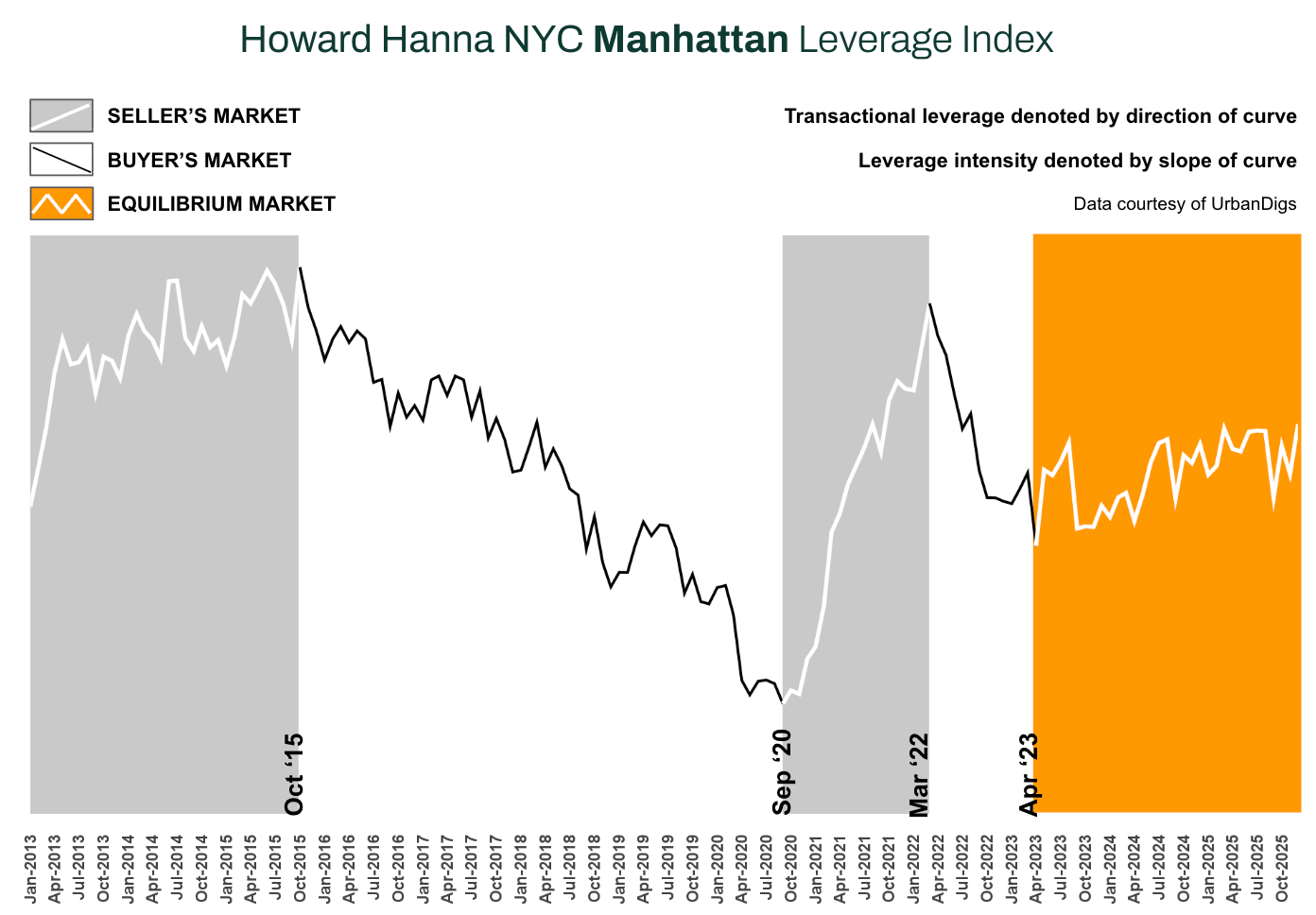

Against this backdrop of strengthening demand and constrained inventory, the Howard Hanna NYC Leverage Index shifted back into seller territory, indicating a modest but clear advantage for sellers entering the new year.

Price indicators, however, remain mixed. The median sale price rose to $1.17 million, up 3.9% year over year and 1.6% from November, while the median price per square foot (PPSF) eased to $1,370, down 1.1% on both a monthly and annual basis. Transaction dynamics suggest stability rather than excess: the median listing discount held at 4.3%, meaning homes traded at approximately 96% of asking price, and median days on market declined to 75, roughly 8% faster than a year ago. Well-priced listings continue to transact efficiently.

Competitive conditions persist in select segments. Approximately 11% of recent sales closed above asking price, underscoring continued demand for high-quality, appropriately priced properties. On the rental side, rents remain at record levels, while mortgage rates, though down from their 2025 highs, are still elevated at approximately 6.3%, reinforcing the ongoing “rate-lock” effect and limiting new supply.

Key Takeaways

-

Demand rebounded into year-end: December contract signings rose 6.5% month over month, exceeding last year’s pace and defying typical holiday-season softness.

-

Inventory remains tight: Supply fell to 4,967 listings, down 21% year over year, reinforcing seller leverage amid limited buyer choice.

-

Pricing steady, not overheated: Median sale prices increased, while PPSF softened modestly, indicating stable valuations rather than rapid appreciation.

-

Seller advantage, narrowly defined: Market fundamentals currently favor sellers, particularly for well-priced, high-quality listings, though conditions remain far from overheated.

Outlook: Overall, Manhattan begins 2026 in a position of balance with a slight seller tilt. Demand is resilient, inventory remains constrained, and pricing is broadly stable, supporting a disciplined and measured market environment as the year unfolds.

The Federal Reserve’s December rate cut, lowering the benchmark range to 3.50%–3.75%, marks a shift toward easing and may gradually improve financing conditions as 2026 progresses.

Photo by Rihards Gederts | Howard Hanna NYC

Howard Hanna NYC Manhattan Leverage Index

The Howard Hanna NYC Manhattan Leverage Index² blends four key market signals – supply, demand, median PPSF, and median listing discount – to gauge the balance of power between buyers and sellers in Manhattan. It’s a proprietary index that distills these metrics into one indicator of market leverage.

Direction Matters:

-

An upward-sloping curve = seller’s market

-

A downward-sloping curve = buyer’s market

-

The steeper the slope, the stronger the advantage for either side

In December, the index ticked up into seller’s territory, indicating a growing advantage for sellers. Three of the four components (contract activity, listing discounts, and inventory levels) moved in sellers’ favor, while only median price per square foot remained tilted toward buyers. This marks a shift from much of 2025, when the index spent long periods in neutral territory, teetering back and forth between slight buyer or seller advantages. We will see if this back-and-forth pattern continues into 2026, but for now the year-end trend favors sellers.

Manhattan Supply

Manhattan Supply: Inventory Tightens Further After Holidays into 2026

Manhattan’s active inventory continued to contract through the end of the year. December closed with roughly 4,967 residential listings on the market – about –5.5% fewer than a month prior and a steep –21.1% drop compared to a year ago. Such a significant year-over-year decline in supply means buyers have markedly fewer options than last winter.

This post-holiday dip in listings is partly seasonal (many sellers pull listings off the market or delay listing new properties in late December), but it’s been exacerbated by 2025’s “rate-lock” effect – many homeowners with ultra-low pandemic-era mortgage rates are still reluctant to sell and give up those rates. The result is an unusually tight inventory landscape as we kick off 2026.

🟥 Buyers: With fewer choices – especially in popular price points and neighborhoods – buyers need to be decisive and well-prepared.

🟩 Sellers: Scarce inventory works to your advantage. You face less competition from other listings, so a well-priced home is likely to draw attention. Listing in early Q1 could capture pent-up buyer demand while options are few.

Outlook: Expect supply to remain constrained through the winter. Many owners locked into ultra-low rates will continue to sit on the sidelines, so a flood of new inventory is unlikely in the near term. Typically, we do see listings tick up as spring approaches, and 2026 should follow suit with more homes hitting the market by March/April. But unless mortgage rates fall significantly (enticing more owners to trade up or move), inventory will likely stay below pre-2020 norms.

Manhattan Demand

Manhattan Demand: Contract Signings Rebound After Holiday Lull

Buyer demand bounced back in December. There were 820 contracts signed across Manhattan in the month – a healthy uptick of +6.5% from November’s level, and roughly +3.9% more deals than the same time a year prior. This reversal comes after a typical November slowdown. The late-year bump in sales suggests many buyers who paused for the holidays re-engaged and moved on properties before year-end.

It’s an encouraging sign that, despite higher interest rates and economic uncertainties, there is underlying pent-up demand ready to act when conditions allow. Notably, December 2025’s contract volume even slightly exceeded previous year levels, highlighting the market’s resilience in the face of affordability challenges.

🟩 Buyers: Rising sales activity means you’ll face more competition on desirable homes. Well-priced listings that hit the market now are seeing increased foot traffic and multiple offers.

🟥 Sellers: Buyer demand is on the upswing, which is good news if you’re listing your home. Traffic at open houses should improve compared to the fall, and there are more qualified buyers actively making offers.

Outlook: The first quarter is usually slower for sales, and January may indeed see a modest dip in contracts simply due to seasonality. However, all signs point to solid underlying demand heading into 2026.

The recent Fed rate cut could bolster buyer confidence, especially if mortgage lenders pass along lower rates by spring. We anticipate serious buyers will continue entering the market as the year progresses, particularly if there’s even a slight easing of financing costs. Barring any major economic upsets, Manhattan buyer interest should pick up notably by the spring selling season.

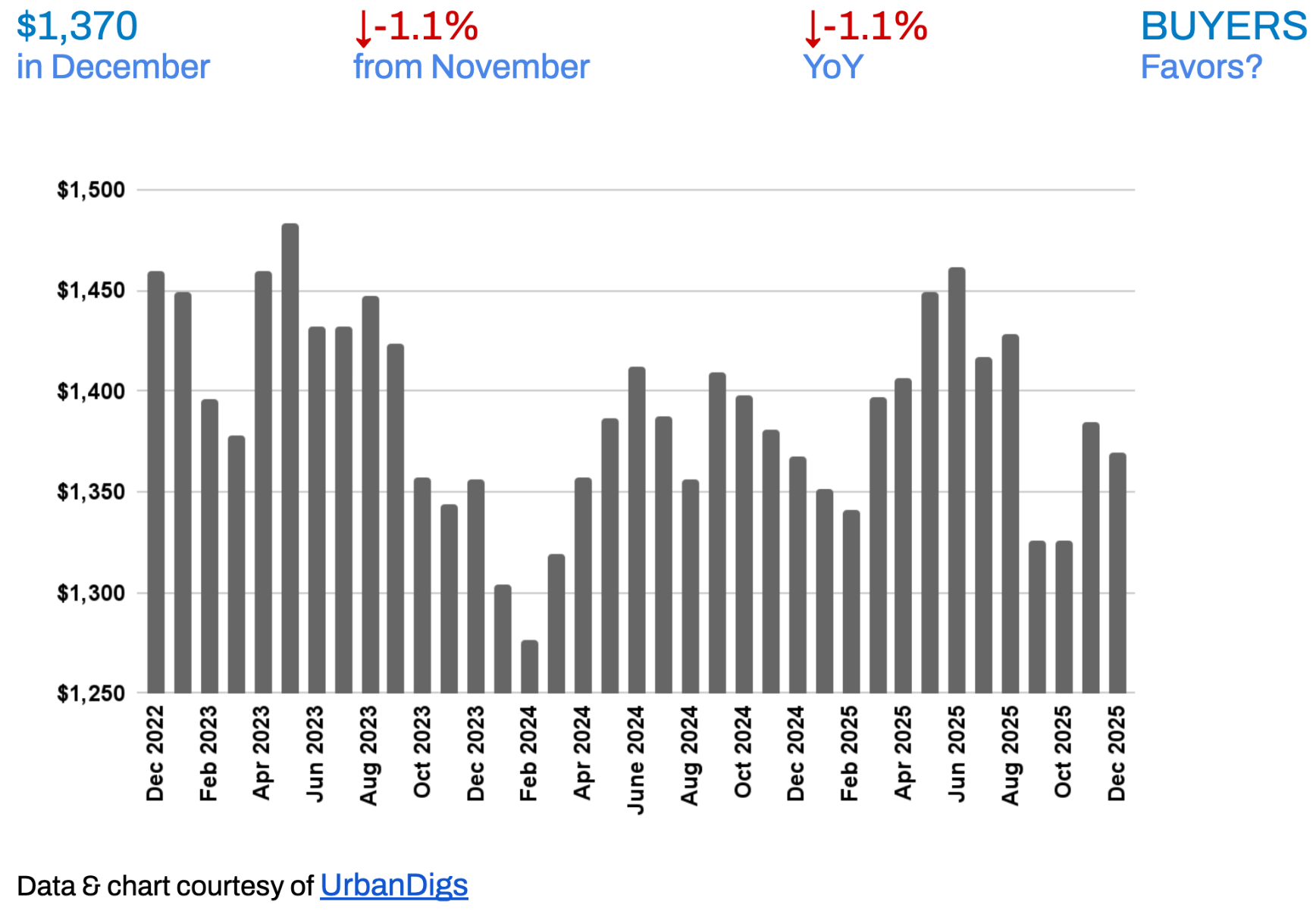

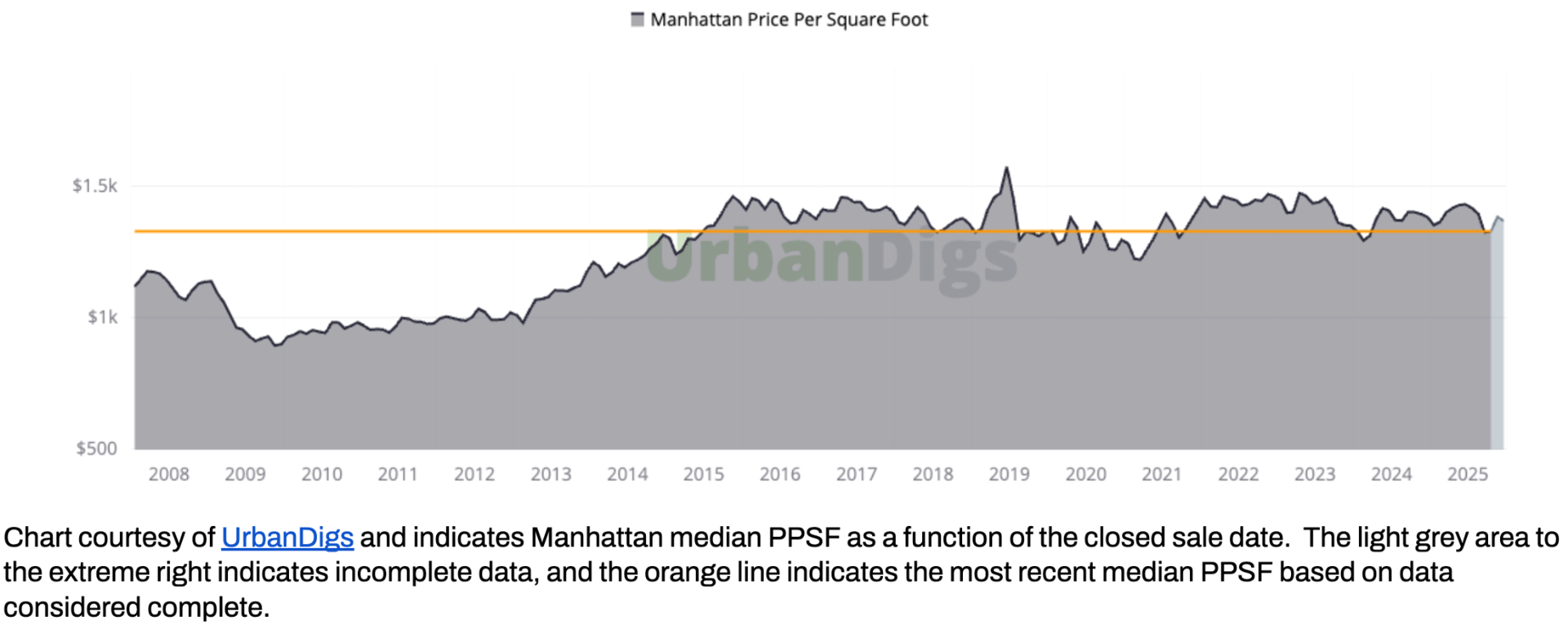

Manhattan Median PPSF

Manhattan Median PPSF: Price Per Square Foot Edges Down at Year-End

Manhattan’s median price per square foot (PPSF) ticked down to about $1,370 in December. This represents a slight –1.1% decline from November’s level (which was roughly $1,385), and a similar –1.1% dip year-over-year. In essence, prices measured on a per-square-foot basis are flat-to-mildly softer compared to both last month and last year. This gentle easing at year-end likely reflects a mix of factors: fewer big-ticket luxury closings in the winter months (which can pull averages down), some sellers adjusting pricing to meet the market, and buyers negotiating hard on overpriced listings. Importantly, the decline is modest – there’s no sign of a sharp price correction, more a slight softening that varies by segment.

🟩 Buyers: The good news is that prices aren’t rapidly escalating. Unlike in some boom periods, you’re not chasing a runaway market. In fact, in certain segments (especially some luxury and new development units), PPSF is a bit lower than a year ago, which can mean better value now.

🟥 Sellers: Even with demand improving, buyers are price sensitive and this slight PPSF dip is a reminder that overpricing can backfire. While overall values are holding up, you might not see much above-ask frenzy in this market. The best strategy is to price at market value – if you do, low inventory and steady demand should ensure you still sell close to your asking price.

Outlook: We expect flat to gently rising PPSF as 2026 gets underway. If inventory remains constrained and buyer activity stays solid, there could be upward pressure on price per square foot by spring – particularly in high-demand neighborhoods or for turnkey properties. However, any increase will likely be measured, not meteoric.

Conversely, if a wave of new development condos hit the market or if interest rates were to spike again, PPSF could stagnate or soften slightly in some pockets. On balance, Manhattan’s PPSF should hold steady, with minor fluctuations, in the coming months.

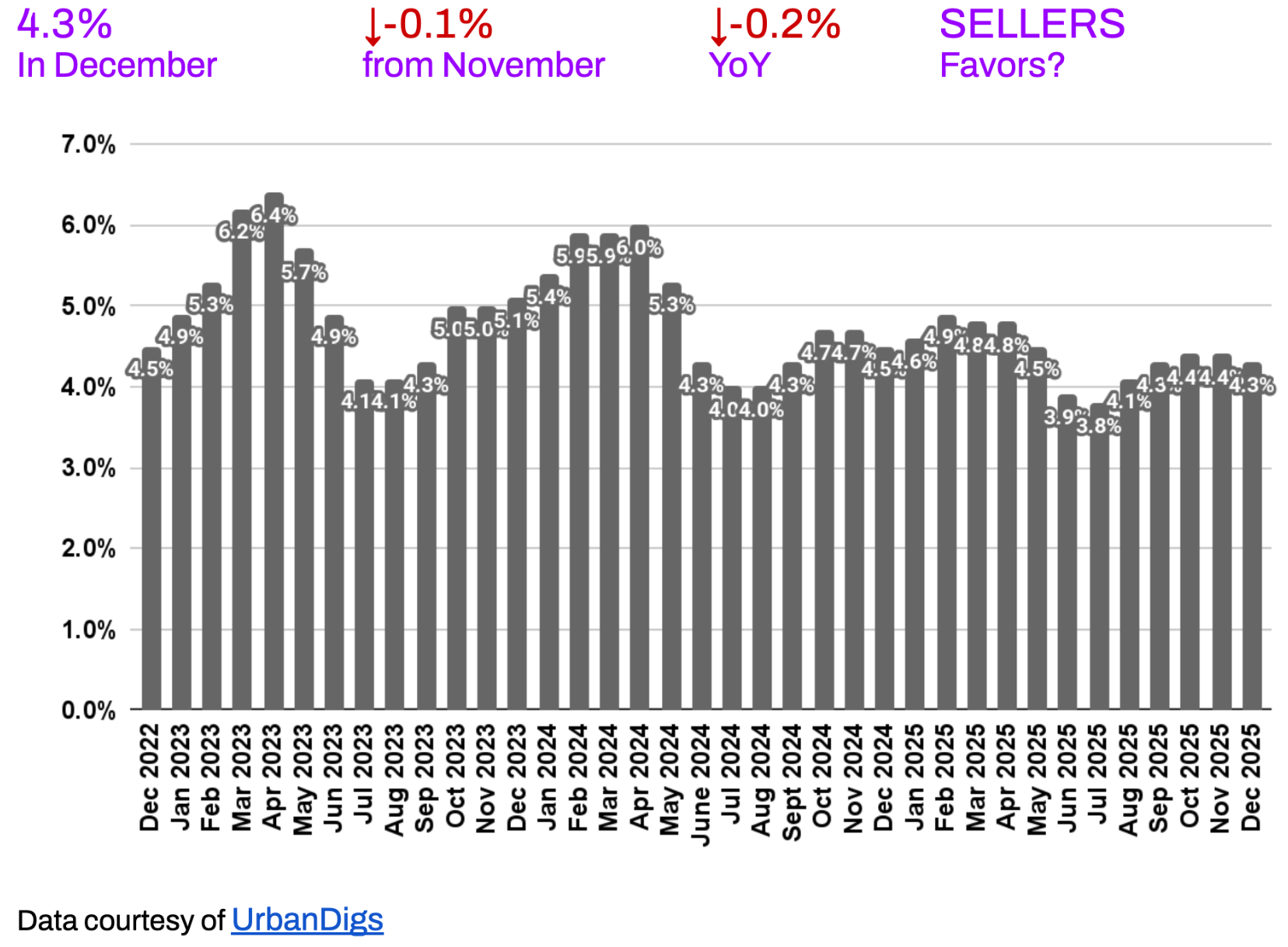

Manhattan Median Listing Discount

Manhattan Median Listing Discount: Negotiations Tip Toward Sellers

The median listing discount – the percentage by which final sale prices are below the last asking prices – held around 4.3% in December. That’s a tight range historically and a slight improvement from the ~4.5% median discount seen a year ago (down about 0.2 percentage points YoY, and 0.1 points lower than November).

In practical terms, buyers on average paid 95.7% of asking price last month. This minimal discount underscores that most Manhattan sellers are still holding firm on pricing and buyers, by and large, are willing to meet them near the ask to get a deal done.

🟩 Buyers: Negotiations are leaning in your favor. On average, you only had to concede around 4% off your asking price in recent deals – a level that indicates you maintain considerable pricing power. If you price your home correctly out of the gate (near fair market value), chances are you can expect offers in the 95–96% of ask range.

🟥 Sellers: Bargains are hard to come by. The low median discount means most sellers are only budging a few percentage points off ask. To find value, focus on listings that have lingered on the market or that were overpriced initially – those are the situations where bigger discounts might be negotiated.

When making offers, understand that a bid 10% below asking will probably be a non-starter on a well-priced property in today’s climate.

Outlook: Expect listing discounts to remain tight through early 2026. In the absence of a major shift in supply or demand, there’s little reason to foresee a dramatic change in negotiation dynamics.

Buyers shouldn’t count on discounts suddenly widening in the winter months – if anything, with inventory so low, sellers have little incentive to slash prices.

On the flip side, a return to widespread bidding wars (where many sales go over ask) also seems unlikely without a significant surge of new buyers. We anticipate that the “near-ask” negotiation pattern will continue: most deals closing within a few percentage points of the list price.

RENTAL REMARKS

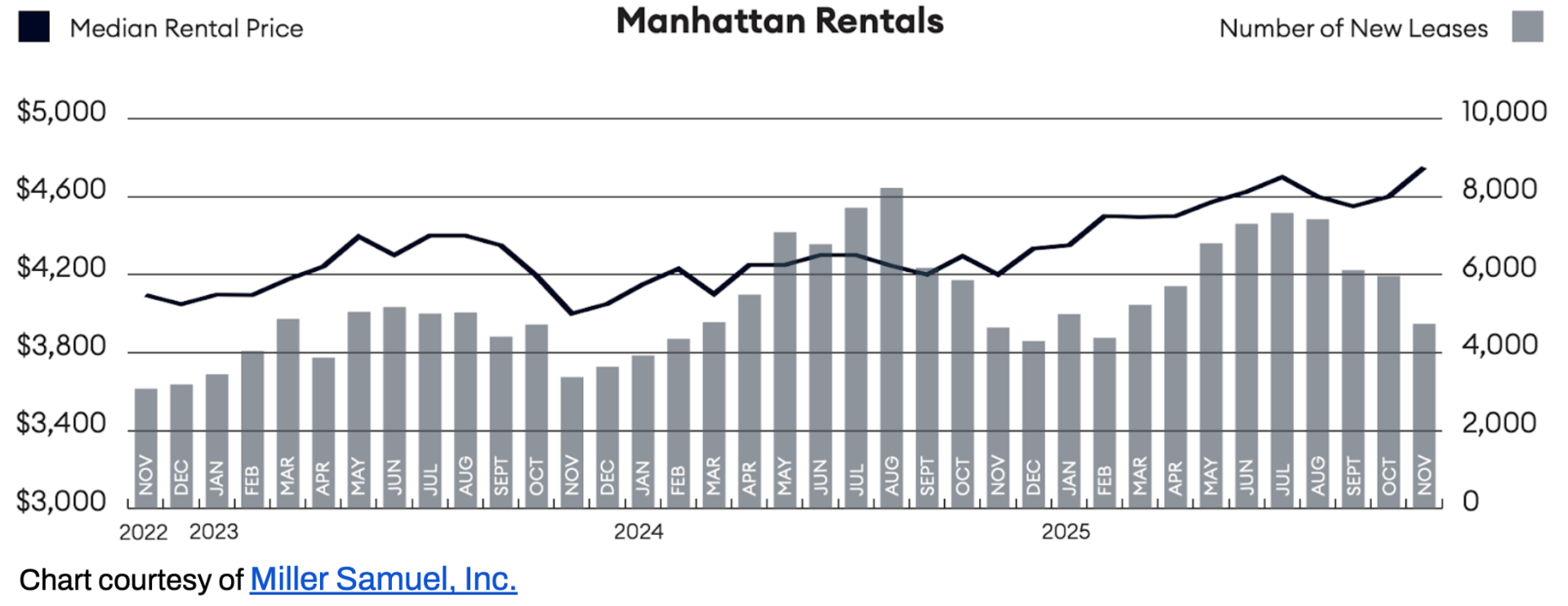

Rental Market: Rents Hit New Records, Tenants Feel the Squeeze

Manhattan’s rental market finished 2025 at all-time highs. The median monthly rent in December climbed to approximately $4,750 – up +3.3% from November and a staggering +13.1% year-over-year – marking a record high for Manhattan.³

Similarly, average rents and rent per square foot also reached new peaks. Demand in the rental sector remains fierce: even as winter sets in, vacancy rates are hovering near historic lows (the vacancy rate stayed below the December average for the past decade).

🟥 Renters: Unfortunately for tenants, affordability has only worsened. Rents are at record levels, and any winter slowdown in pricing is minimal at best. There are very few concessions (like free months or owner-paid fees) in today’s market. If you’re searching, budget accordingly and be ready to act fast when a decent apartment (within your price range) hits the market – it likely won’t last long.

🟩 Landlords: These conditions remain squarely in your favor. You’re achieving historically high rents and low turnover. Many apartments are drawing multiple applicants, sometimes bidding above the asking rent, even in what is typically an off-peak season.

Outlook: The seasonal chill of winter may bring a tiny bit of relief to the rental market – we might see rent growth pause or tick down slightly in January/February as demand temporarily ebbs. However, any relief for renters is likely to be short-lived and modest.

The fundamental picture is unchanged: a strong job market, high housing costs keeping people in rentals, and scarce vacancies point to continued high rents in 2026. 2026 is poised to be another landlord-friendly year in Manhattan.

MORTGAGE REMARKS

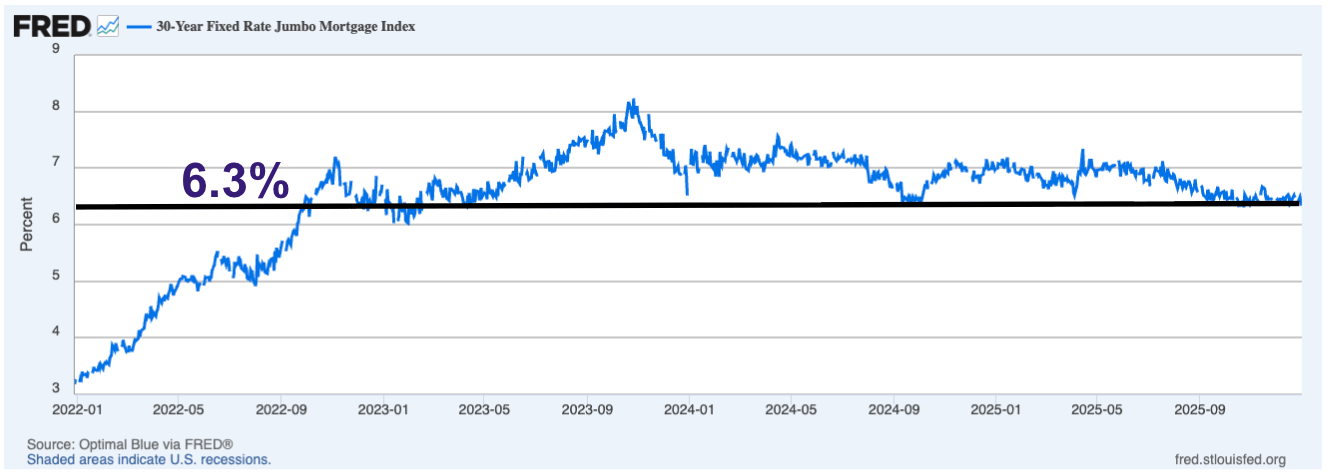

Mortgage Rates: Slight Relief, But “Rate Lock” Effect Lingers

Mortgage rates remain elevated but are drifting lower compared to their 2025 peak. By December, the average 30-year jumbo loan rate hovered around 6.3%⁴, down from the 7%+ highs seen in Q3. Many borrowers with excellent credit even saw quotes in the high-5% range for conforming loans toward year-end. The APR for jumbo loans (which factors in some fees) settled near 6.1%⁵ in December.

This gradual easing of rates has provided marginal relief to buyers’ monthly payments, but let’s be clear: borrowing costs are still significantly higher than the ultra-low 3–4% rates enjoyed during 2020–2021.

One major consequence of sustained ~6%+ mortgage rates is the ongoing “rate lock” effect. A huge swath of homeowners refinanced or bought at those sub-3% rates in the pandemic era; many of them are now hesitant to sell and give up their cheap financing.

This has kept resale inventory tight, as noted earlier. In turn, fewer move-up sellers means fewer new listings, which helps keep home prices supported (even as higher rates simultaneously dampen some buyer affordability). It’s a bit of a stalemate dynamic caused by high rates.

Outlook:

December 2025 brought a noteworthy development: the Federal Reserve cut its benchmark interest rate by 25 bps, bringing the federal funds target range to 3.50%–3.75%. This is the first meaningful step toward monetary easing since mid-2023, and it sets the stage for improved borrowing conditions as we move into 2026. Mortgage rates tend to follow the direction (if not the exact magnitude) of Fed policy over time, so this could foreshadow further relief for home loans in the coming year.

However, buyers should temper expectations – we are unlikely to see sub-5% 30-year mortgage rates again unless the economy enters a downturn or the Fed enacts much larger cuts due to recessionary pressures. Most projections have 2026 mortgage rates averaging in the mid-5% to low-6% range.

INVESTOR INSIGHTS

Market Overview: 2025 presented a mixed bag for real estate investors in Manhattan. On the international front, currency dynamics provided a tailwind: roughly a 4–5% drop in the U.S. dollar over the past year has made Manhattan property effectively cheaper for many foreign buyers.

A $5 million apartment now “feels” closer to $4.75M for someone converting from euros, pounds, or yen at today’s rates. This forex discount, combined with Manhattan’s perennial appeal as a stable, long-term investment, has sparked renewed interest from overseas.

We’ve seen an uptick in foreign buyers, particularly targeting luxury condos and new developments in prime areas. These global investors are taking advantage of the dollar’s slide and some softness in Manhattan luxury prices since the peak; for them, this is an opportunistic entry point into a market they view as a safe haven.

Meanwhile, local (domestic) investors have been more cautious. With mortgage rates hovering ~6–7% for investment loans and rental yields still modest (~3–4%), the math on a traditional condo/co-op investment isn’t terribly compelling.

Key Insight: We currently have a somewhat bifurcated investor market – global capital is moving actively, while local capital is more restrained.

Outlook: Several factors will influence investors as we move through 2026. The Federal Reserve’s policy path is chief among them; if inflation continues to cool, the Fed could make additional rate cuts, hastening the decline of mortgage rates (a big “if,” but one to watch closely).

Cheaper financing would undoubtedly bring more investors – both foreign and domestic – off the sidelines.

References

1. Data courtesy of UrbanDigs

2. According to the Howard Hanna NYC Manhattan Leverage Index

3. Data courtesy of Miller Samuel, Inc.

4. Data courtesy of Federal Reserve Bank of St. Louis

5. JUMBO mortgage rate APR data courtesy of Bank of America, Chase, and Wells Fargo

6. Cover Photo by Rihards Gederts.

If you would like to chat about the most recent market activity,

feel free to contact us at [email protected] or

connect with one of our Advisors.

About Us

Howard Hanna NYC brings the nation’s largest independent and family-owned brokerage to New York City, uniting the strength of a national network with the insight and sophistication of a local firm. Formed through joining forces with Elegran Real Estate, Howard Hanna NYC delivers a seamless, full-service experience backed by more than 15,000 agents across 500 offices in 14 states. The firm’s forward-thinking, agent-first culture continues to shape the future of real estate across Manhattan and the Tri-State area.

Learn more at www.howardhannanyc.com.