Momentum Holds as NYC Pushes Deeper Into Summer

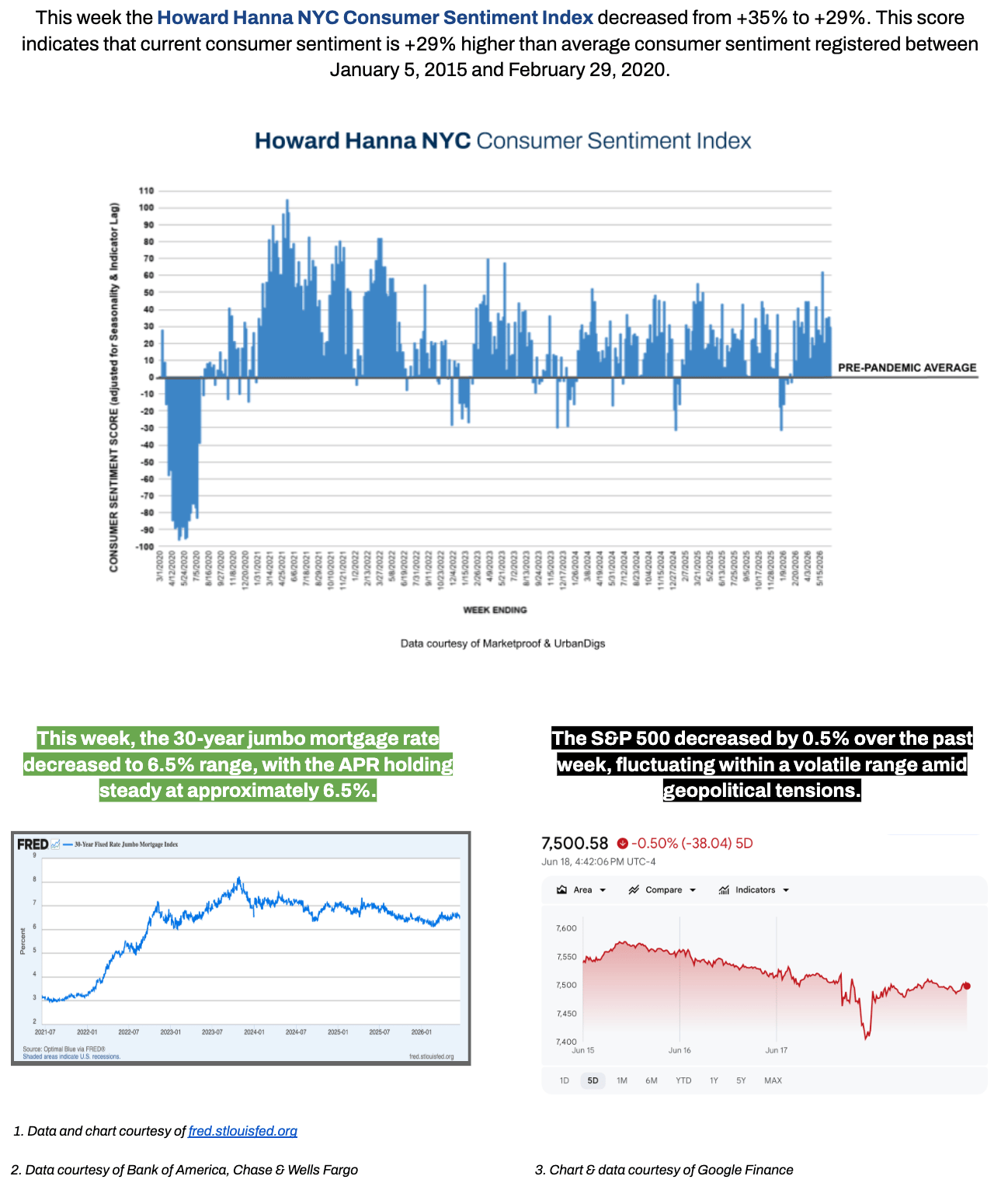

New York City's housing market carried its momentum through a shortened working week, with signed contracts running well ahead of last year in both boroughs and pending sales climbing across the board. The week's softer sentiment reading is best understood in context - it reflects a holiday-shortened calendar and contract backlog rather than any genuine loss of demand.

The Howard Hanna NYC Consumer Sentiment Index decreased from +35% to +29% - a typical week-to-week fluctuation that also includes some backlog contracts not yet recorded. This was also a short working week in NYC due to the Juneteenth holiday, which compresses reported activity.

What This Means for Summer 2026

For buyers: Pending sales are rising in both boroughs and Manhattan inventory remains 7.1% below last year. With contract activity running double-digits ahead of last summer, waiting for materially better conditions risks competing against a more active market.

For sellers: Demand is firmly in your favor - but the pricing truism holds. Well-priced product is selling fast at ask, while aspirational pricing means longer days on market and deeper cuts down the line.

Overall, the market is entering mid-summer 2026 on firm footing: tight Manhattan supply, steady Brooklyn growth, rising pending pipelines in both boroughs, and contract volumes well above year-ago levels.

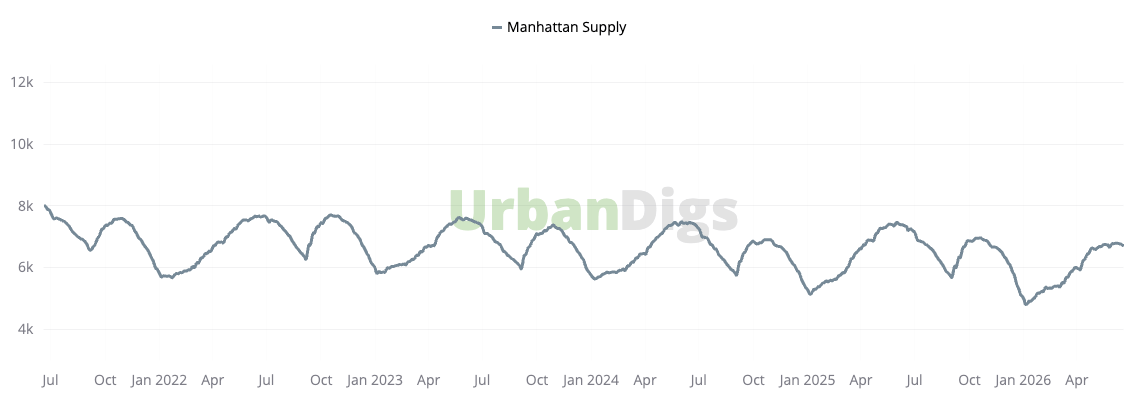

Manhattan Supply: Inventory Tightens Further Below Last Year

Manhattan active inventory held roughly steady at 6,714 homes (−1% week-over-week | −7.1% year-over-year), remaining notably below last year's level. New listings totaled 313 units (0% week-over-week | +5% year-over-year), reflecting a year-over-year increase in seller activity but no change from the prior week.

The takeaway for buyers and sellers: the persistent year-over-year supply deficit continues to favor well-positioned sellers, while buyers face a market with fewer options than a year ago heading into summer. For buyers, that means moving decisively on well-priced homes; for sellers, the tight backdrop rewards accurate pricing from day one.

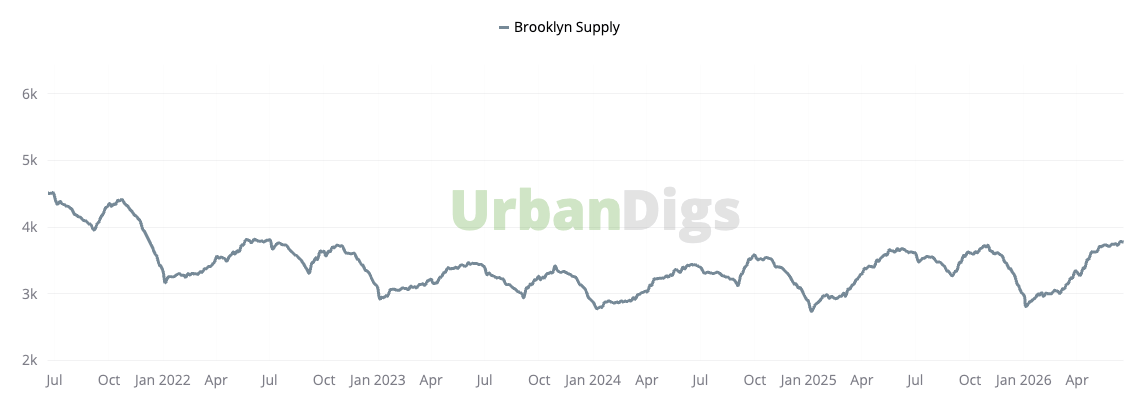

Brooklyn Supply: Steady Growth Continues

Brooklyn inventory remained virtually unchanged at 3,785 homes (+0.2% week-over-week | +4.5% year-over-year) - a modest weekly increase and continued year-over-year growth. New listings decreased to 201 units (−20% week-over-week | +10% year-over-year), a sharp weekly pullback set against solid year-over-year growth.

This pattern suggests Brooklyn supply may continue expanding gradually if new listings keep returning, though the weekly dip points to measured, uneven growth. For buyers, Brooklyn continues to offer more room than Manhattan; for sellers, the year-over-year rise in listing flow underscores why accurate pricing matters from day one.

Pending Sales: Forward Pipeline Strengthens in Both Boroughs

Pending sales increased in both Manhattan and Brooklyn, reinforcing the view that buyer activity remains healthy and that the market is carrying momentum into the summer season.

Manhattan pending sales: up +3% week-over-week to 4,059 units - a steady gain that signals a strengthening forward transaction pipeline.

Brooklyn pending sales: up +2% week-over-week to 2,234 units - stable deal flow as buyers continue moving toward contract.

Photo by Rihards Gederts | Howard Hanna NYC

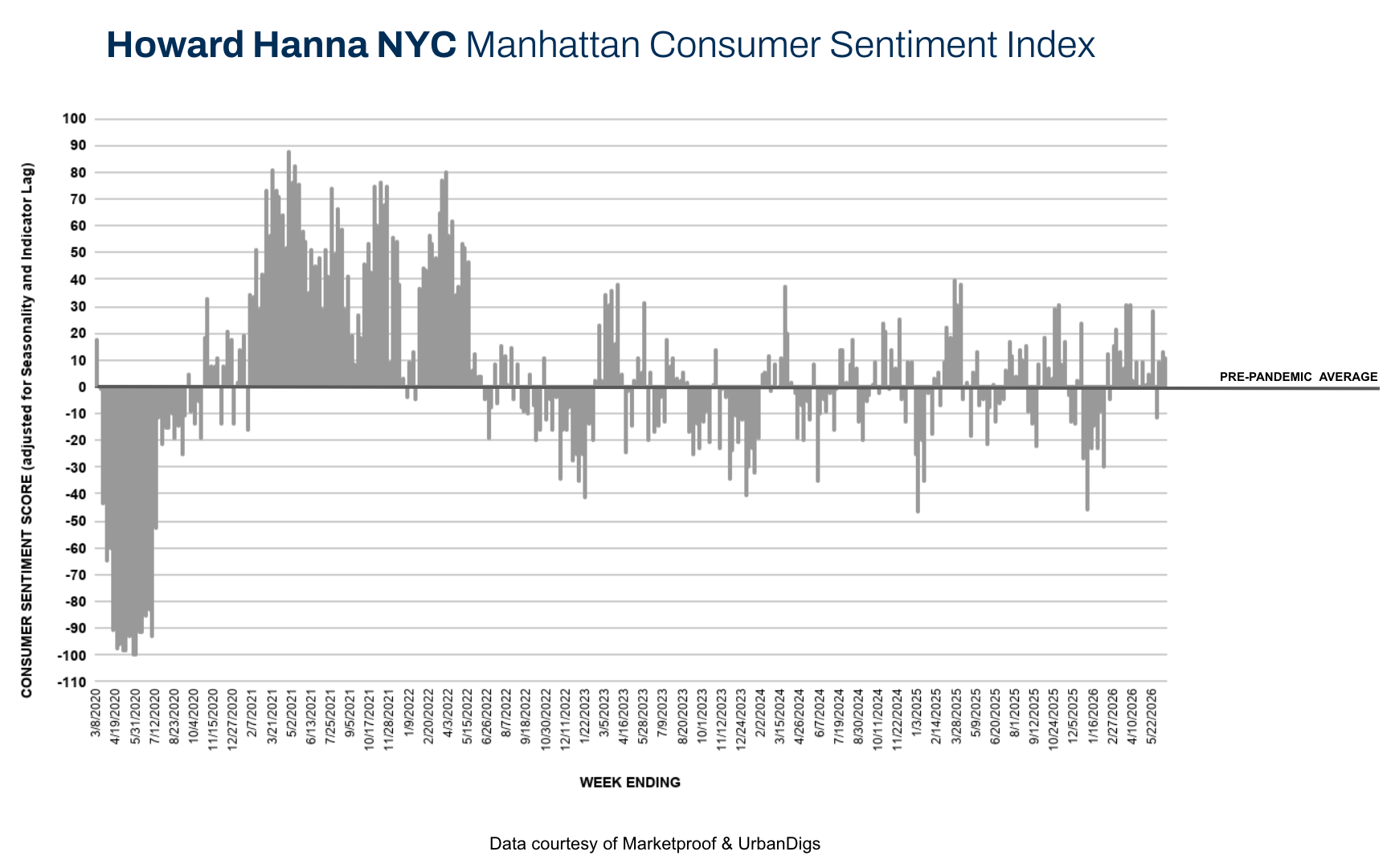

Manhattan Consumer Sentiment: Holding in Positive Territory

Manhattan recorded 266 signed contracts (−2% week-over-week | +23% year-over-year) — a slight weekly dip but a strong year-over-year gain.

The Howard Hanna NYC Manhattan Consumer Sentiment Index decreased slightly from +13% to +11%, marking virtually no change and holding in positive territory as the market rolls through the summer of 2026.

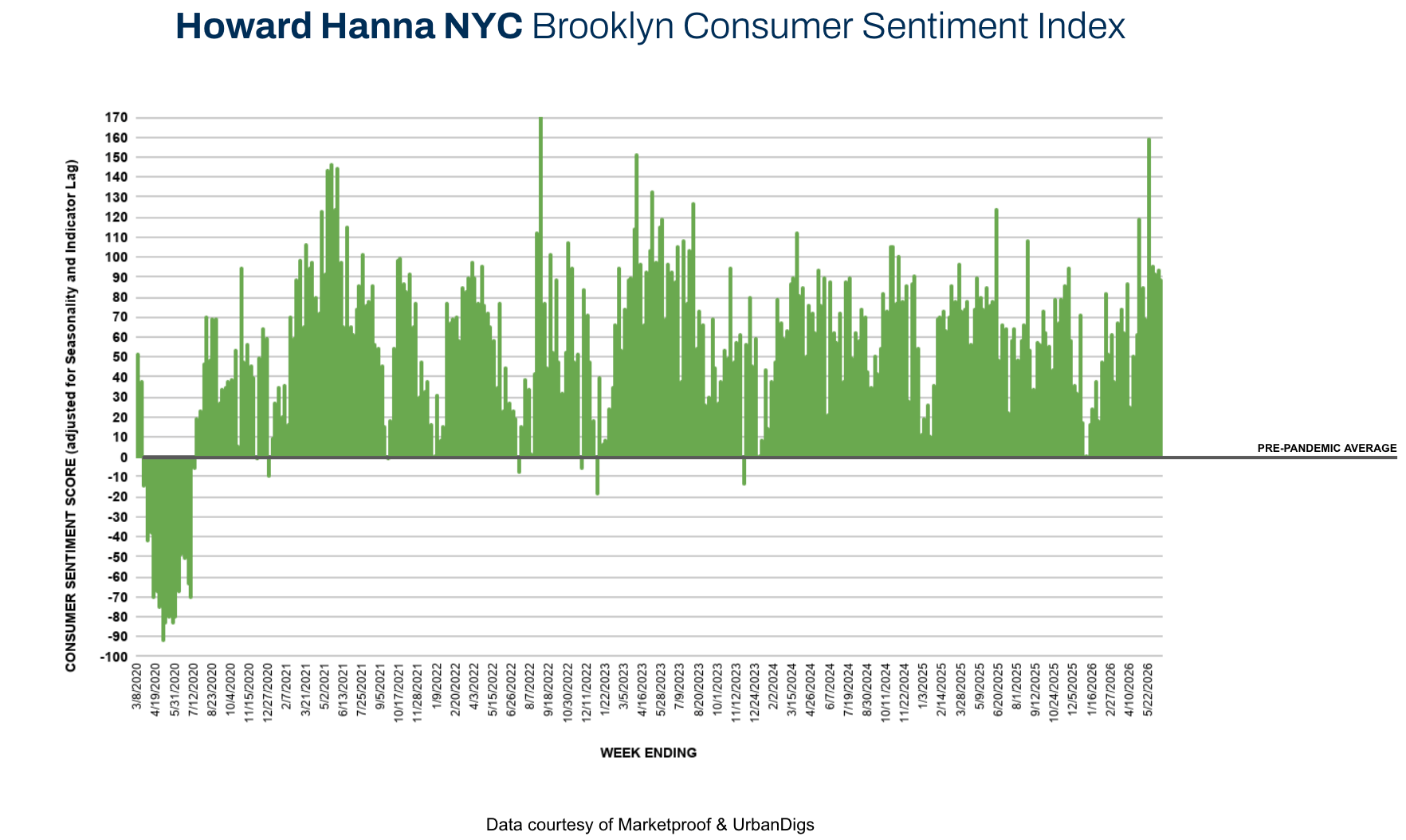

Brooklyn Consumer Sentiment: Engagement Stays Elevated

Brooklyn recorded 155 signed contracts (−3% week-over-week | +24% year-over-year) — a slight weekly contraction but a notable year-over-year increase.

The Howard Hanna NYC Brooklyn Consumer Sentiment Index decreased slightly from +94% to +89%, signaling that buyer engagement remains elevated as the market rolls through summer.

New Development Insights: One Manhattan Square and Greenwich Village Lead

According to Marketproof data, new development activity recorded 34 signed contracts across 26 buildings during the week of June 15, 2026 — the strongest weekly tally in recent weeks. Top-performing developments included:

One Manhattan Square (Two Bridges) with four signed contracts

The Village West (Greenwich Village) with three signed contracts

Demand continues to concentrate in well-located, lifestyle-oriented developments with strong pricing alignment, reinforcing buyer preference for turnkey product in prime neighborhoods.

If you would like to chat about the most recent market activity,

feel free to contact us at [email protected] or

connect with one of our Advisors.

Howard Hanna NYC brings the nation’s largest independent and family-owned brokerage to New York City, uniting the strength of a national network with the insight and sophistication of a local firm. Formed through joining forces with Elegran Real Estate, Howard Hanna NYC delivers a seamless, full-service experience backed by more than 15,000 agents across 500 offices in 14 states. The firm’s forward-thinking, agent-first culture continues to shape the future of real estate across Manhattan and the Tri-State area.Learn more at www.howardhannanyc.com.