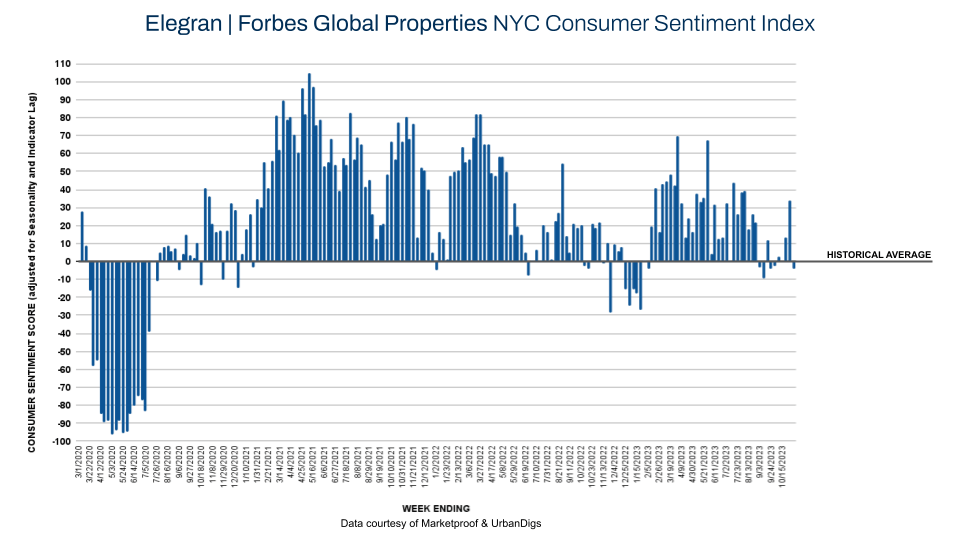

Surprising Early Peak and Cooling Sentiment in NYC's Fall Real Estate Market

This week, we observe a substantial dip in the Consumer Sentiment Index, dropping from +34 to –4. This suggests a 4% decrease in the attitude toward NYC residential real estate relative to the pre-pandemic benchmark.

This decline, to some extent, stems from a potentially early peak in Fall demand, which became evident when pending sales began their decline two weeks ago. Several external factors are also exerting pressure on the market. Geopolitical unrest, with the conflict in Israel and Gaza as a significant stress point, a stumbling stock market, and escalating interest rates have collectively sapped the momentum from the Fall market.

As we move towards winter, a period typically associated with market slowing, NYC still expects to maintain a level of activity consistent with the long-term pre-COVID average. Our ongoing analysis of supply and demand, along with consumer sentiment shifts, aims to deliver an informed and transparent view of NYC's unique real estate dynamics.

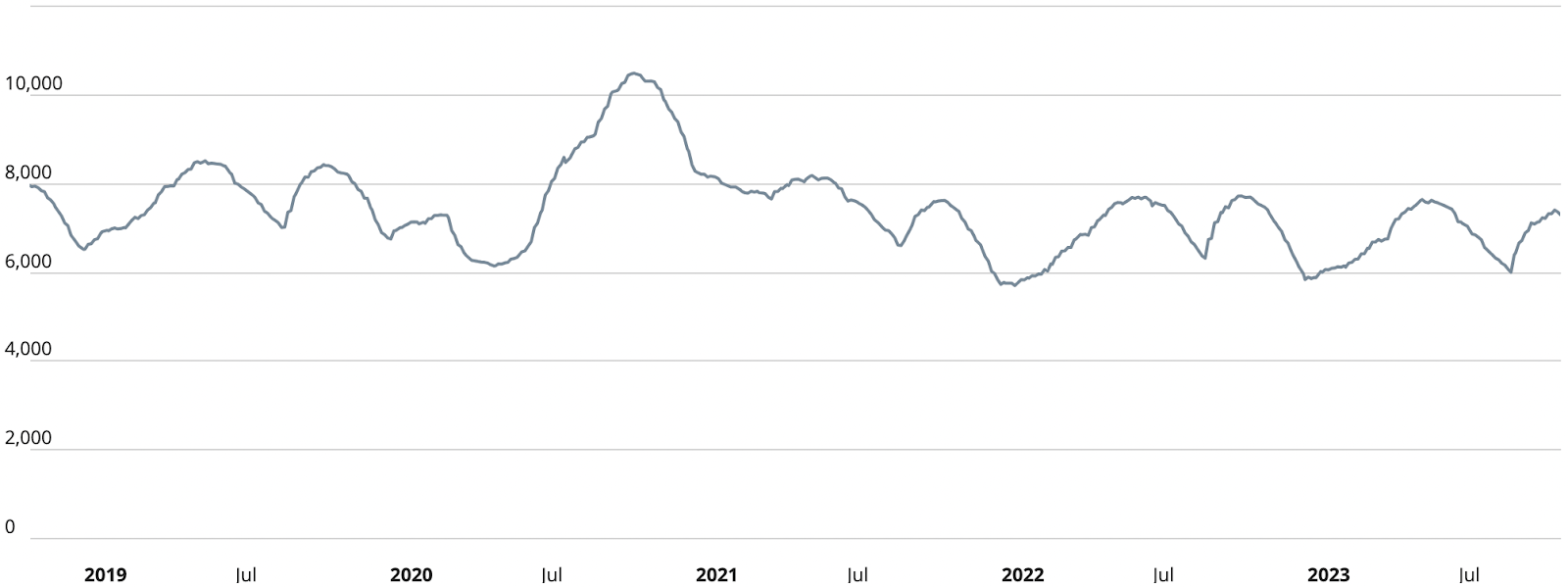

Manhattan Supply

Manhattan's real estate supply dynamics have taken a turn as anticipated, reaching a seasonal high last week. Through the end of the year, we can expect to see a rapid contraction in the number of available units. However, the abundance of supply still overshadows the demand, with a current ratio of 7,288 units available against 150 units closed this week.

Manhattan Supply | Data courtesy of UrbanDigs

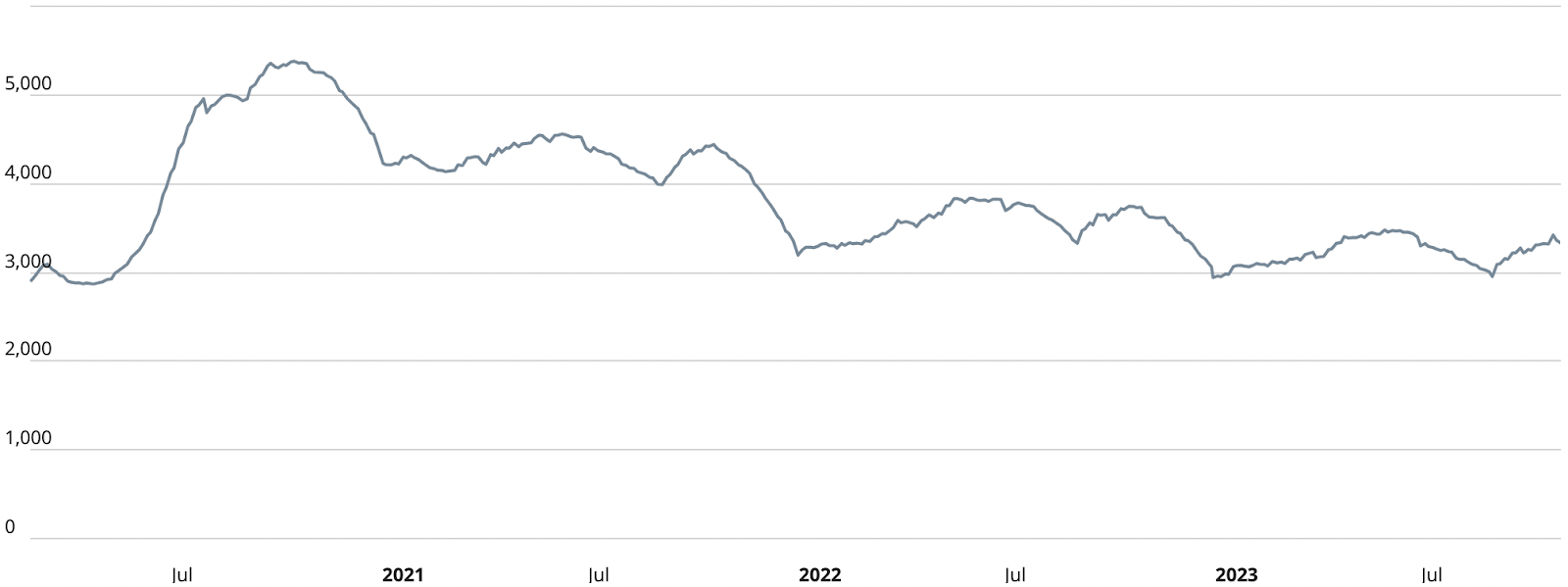

Brooklyn Supply

Brooklyn's real estate supply peaked last week and is expected to decline towards year-end. Currently, with 3,330 units on the market, far exceeding the week's demand of 123 units, buyers are presented with many choices. This surplus aligns with the distinctive nature of New York City's market, which contrasts with the tighter, more competitive national markets.

Brooklyn Supply | Data courtesy of UrbanDigs

Manhattan Pending Sales

Manhattan’s pending sales have taken an unexpected downturn over the past two weeks. This week's count stands at 2,484 pending sales, indicating an early arrival of the seasonal high, a full month ahead of schedule. This premature decline suggests a shift in market activity that could signal a variety of underlying factors affecting buyer engagement and could potentially influence market trends as we approach the winter months.

Brooklyn Pending Sales

Brooklyn's pending sales this week tally at 1,846, reflecting a similar trend to Manhattan with an early and unanticipated downturn. Historically peaking in late November or early December, the figures suggest that this year's peak may have already occurred. This premature decrease could be indicative of broader market shifts or specific local factors influencing Brooklyn's real estate dynamics as we move into the final stretch of the year.

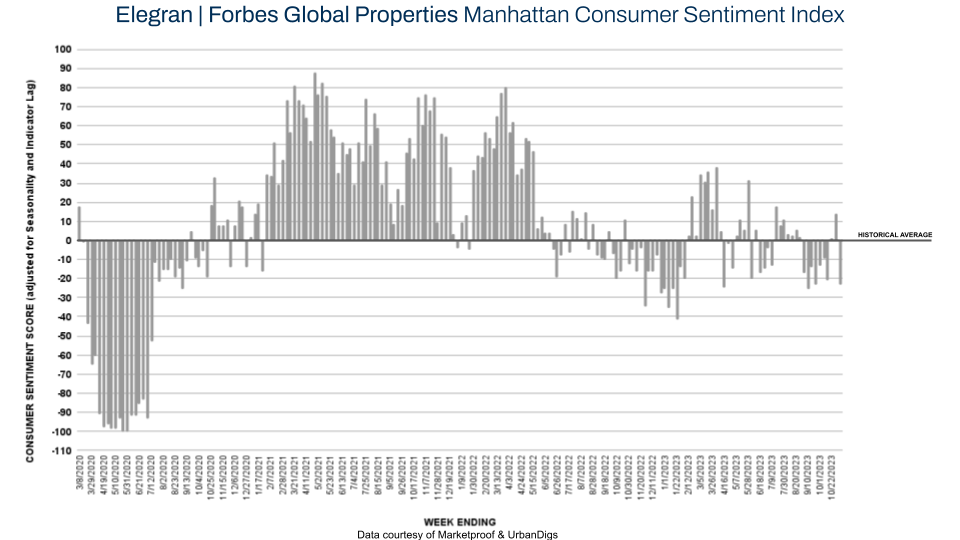

Manhattan Consumer Sentiment

This week in Manhattan, the Consumer Sentiment Index has seen a significant drop, plunging from +14 to -23. This change in attitude toward Manhattan residential real estate is attributed to various factors, including the premature peaking of fall demand, geopolitical unrest, a declining stock market, and rising interest rates. These elements have collectively contributed to the subdued sentiment and are reflective of a broader hesitancy in the market. With buyer activity slowing, the number of contracts signed has decreased to 150 this week, down from 210.

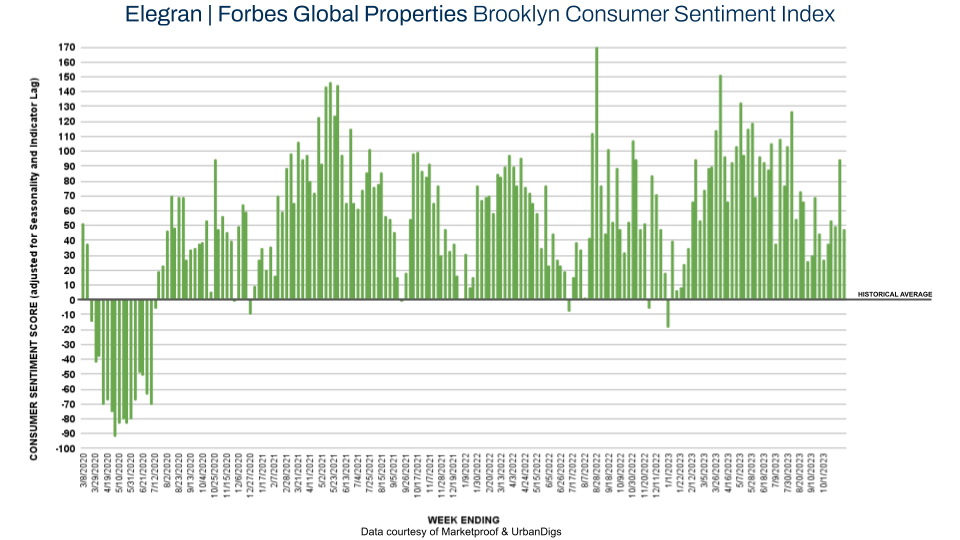

Brooklyn Consumer Sentiment

Brooklyn's Consumer Sentiment Index has halved from +94 to +47 this week, a sharp reduction. Yet, our chart still indicates that sentiment is 47% above its pre-pandemic average. Despite the fall, consumer confidence in Brooklyn has largely remained stronger than historical averages since July 2020. The drop this week, while significant, continues to highlight Brooklyn's resilience and attractiveness to buyers, with 123 contracts signed versus 134 the previous week, suggesting sustained interest in Brooklyn's real estate market.

New Development Insights

Marketproof reported that 27 new development contracts were signed in 24 buildings this week. The following buildings were the top-selling new developments of the week:

- GREENWICH WEST (SoHo)

- 450 WASHINGTON (Tribeca)

- 134-16 35TH AVENUE (Flushing)

Each reported two contracts.