The inflation rate is +151% higher than its long-term average.

JUMBO mortgage rates are up +109% YTD.

^GSPC (the S&P 500 index) has given back –21% YTD.

And yet, demand for NYC residential real estate (as measured by weekly signed contracts) continues to equal or exceed its pre-pandemic average (the period 5 Jan 2015–1 Mar 2020). Floating atop an ocean of investments that purport the primary objective of principal preservation with capital appreciation as a secondary strategy, NYC residential real estate would appear to be the new gold standard. Except that the concept of NYC weathering market volatility isn’t a new story at all; in fact, it’s a story as old as the data allows us to tell.

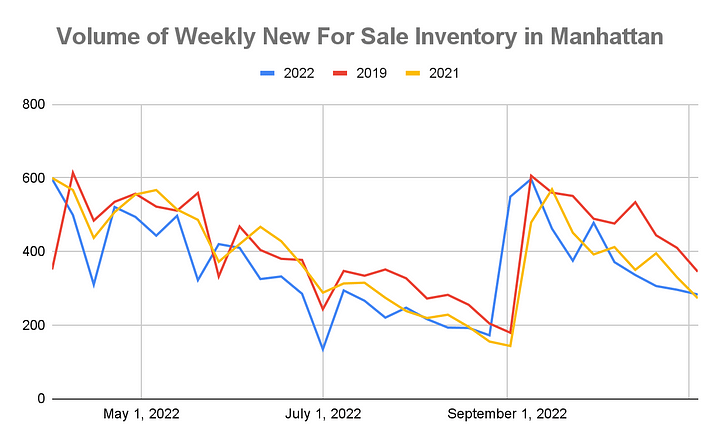

Manhattan Supply

Decreased modestly again this week to 7,569 units. 273 new listings came to market, less than last week, less than the same week last year (not surprisingly), and slightly less than the same week in 2019. Although weekly demand remains equal to or greater than pre-pandemic levels, fewer and fewer sellers are coming to market to meet that demand, and an increasing number of sellers are taking their homes off the market. We believe that the sanguine demand and price inflation that defined 2021 and H1–2022 may have set unrealistic expectations, and sellers are discouraged from participating in a market that is historically normal by most metrics.

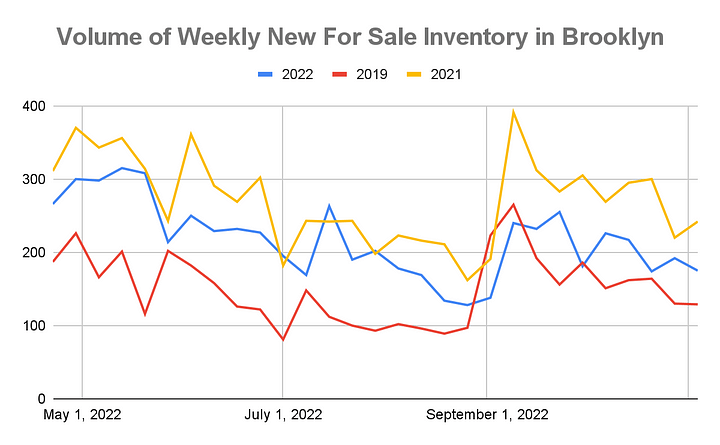

Brooklyn Supply

Decreased slightly this week to 3,450 units for sale and 175 new listings coming to market. New listings are, not surprisingly, significantly less than this time last year 2021, but remain far greater than 2019 (pre-pandemic) levels.

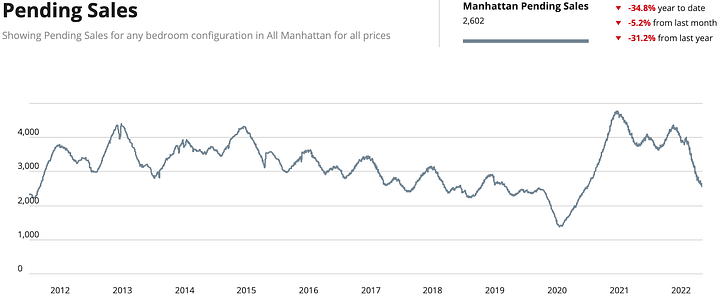

Manhattan Pending Sales

Decreased again this week to 2,602, on par with the same number immediately preceding the rollout of the COVID-19 vaccine in 2021.

Chart courtesy of UrbanDigs

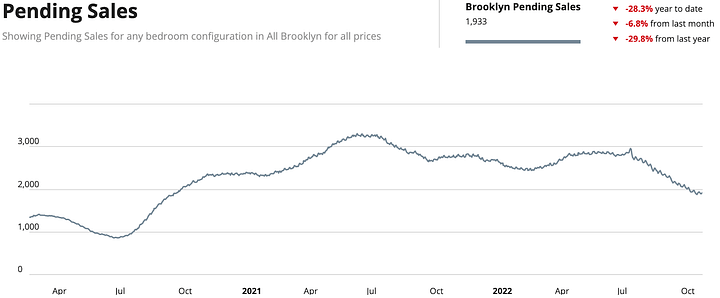

Brooklyn Pending Sales

Remained unchanged at 1,933 and, like Manhattan, have now pulled back to levels previously posted just before the vaccine rollout.

Chart courtesy of UrbanDigs

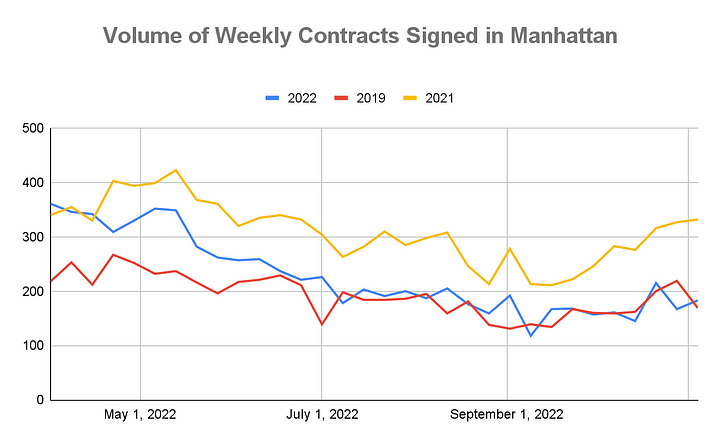

Manhattan Contracts Signed

183 contracts were signed this week. Although this number still appears very lean in comparison to the same week in 2021, we continue to stress that 2021 (and H1–2022) was atypical and that demand for Manhattan residential real estate (as measured by weekly signed contracts) is normal by historical (pre-pandemic) standards.

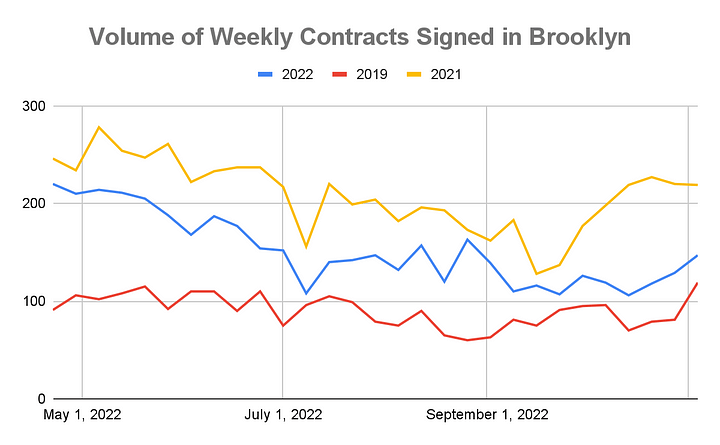

Brooklyn Contracts Signed

147 contracts were signed this week, and, like Manhattan, that’s up from last week and down as expected from the record absorption of 2021. Most importantly, demand for Brooklyn residential real estate (as measured by weekly signed contracts) continues to significantly outperform the pre-pandemic average.

New Development Insights

As reported by Marketproof, this week, 53 new development contracts were reported across 40 buildings. The following were the top-selling new developments of the week:

- Umbrella Factory in East Williamsburg

- 100 Vandam in SoHo

- The 45 Argyle Road in Prospect Park South

- The Hayworth in Carnegie Hill