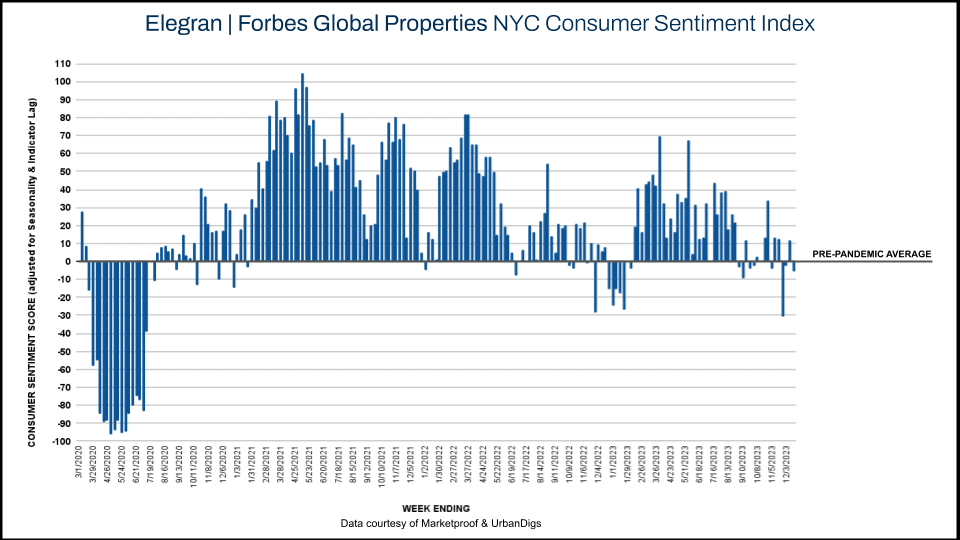

Reversion to the Mean

The Elegran | Forbes Global Properties NYC Consumer Sentiment Index, below, illustrates what we vividly remember - that sentiment was extremely low from March through June 2020. Then, 2021 through much of 2023 saw a boom in demand, regularly registering a score of +40 or more. However, in the last three months, half of the weekly consumer sentiment scores have deviated from the pre-pandemic average by less than 5%.

As the principles of economics dictate, it appears that consumer sentiment is returning to the mean after the period of extreme volatility caused by the COVID-19 pandemic.

The market bifurcation that we’ve discussed is still firmly in place. Compared to their pre-pandemic benchmarks, demand for resale apartments is stronger than for new development, and demand for Brooklyn is stronger than for Manhattan.

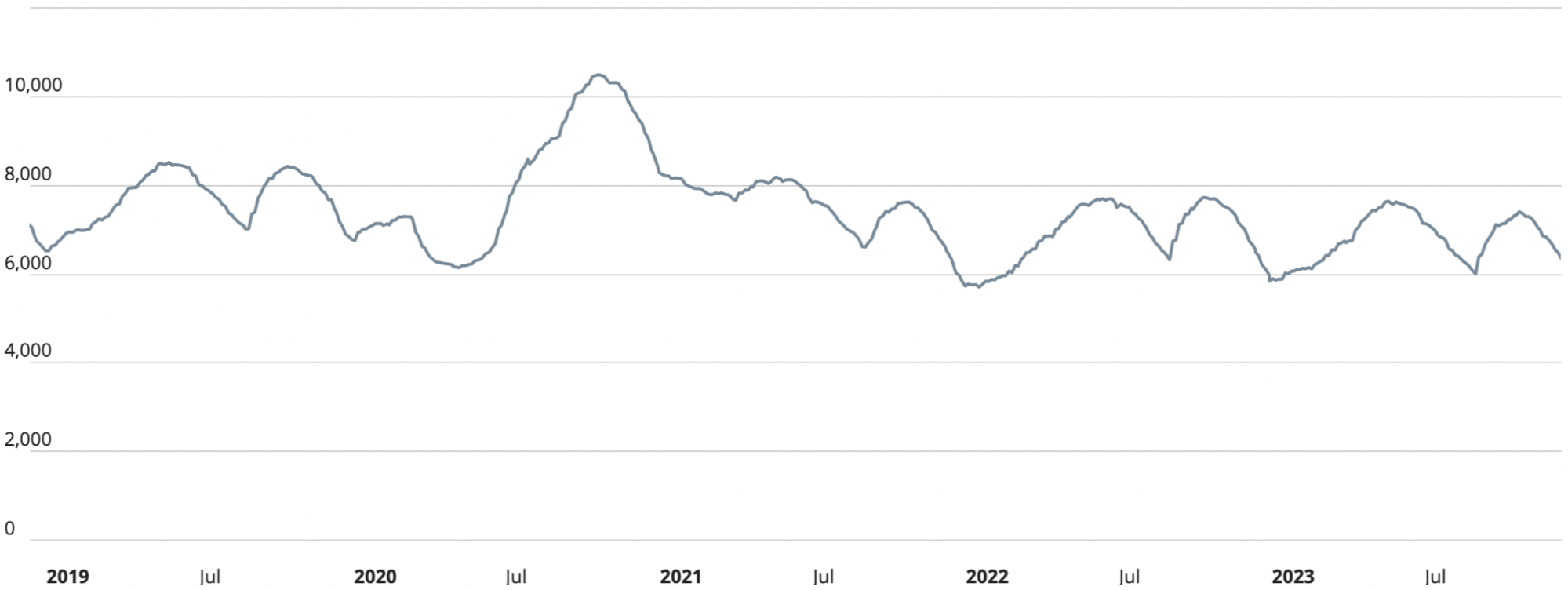

Manhattan Supply

As we would expect from analyzing the repetitive pattern of the chart below, supply reached the second peak of the year during October and should continue to retreat through the year’s end. Why is the supply count important? The answer for many national markets is that supply can become sparse enough to struggle to satisfy demand, and prices can inflate substantially for this reason. But in NYC, there is far more supply than demand. This week, Manhattan’s ratio is 6,339 units of supply to 152 units of demand.

Manhattan Supply | Data courtesy of UrbanDigs

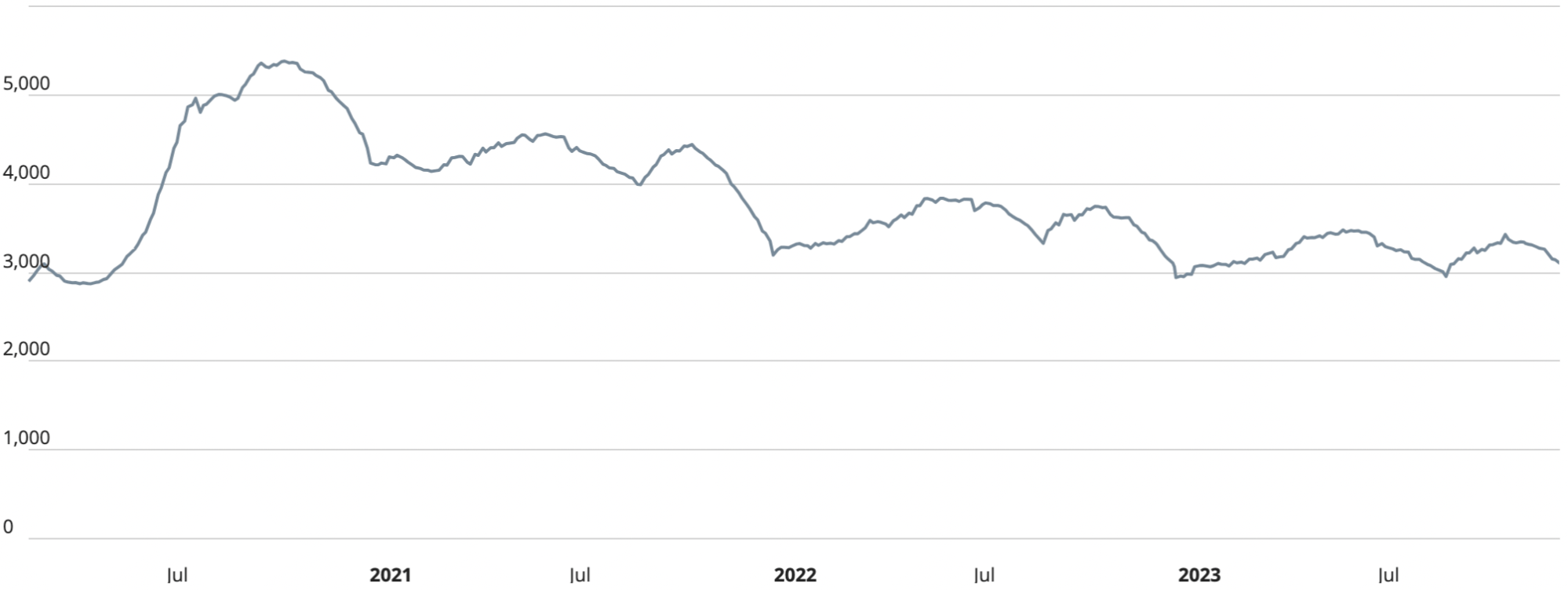

Brooklyn Supply

As we would expect, given the chart below, the metric is in decline and should continue to retreat for the remainder of 2023. The 3,103 units available are far more than are necessary to satisfy this week’s demand of 114 units.

Brooklyn Supply | Data courtesy of UrbanDigs

Manhattan Pending Sales

For the second week in a row, pending sales unexpectedly climbed this week to 2,457 units. However, the metric should begin to decline again next week and do so through February or March of next year.

Brooklyn Pending Sales

For the second week in a row, pending sales unexpectedly climbed to 1,809 units. However, the metric should begin to decline again next week and do so through the Winter season.

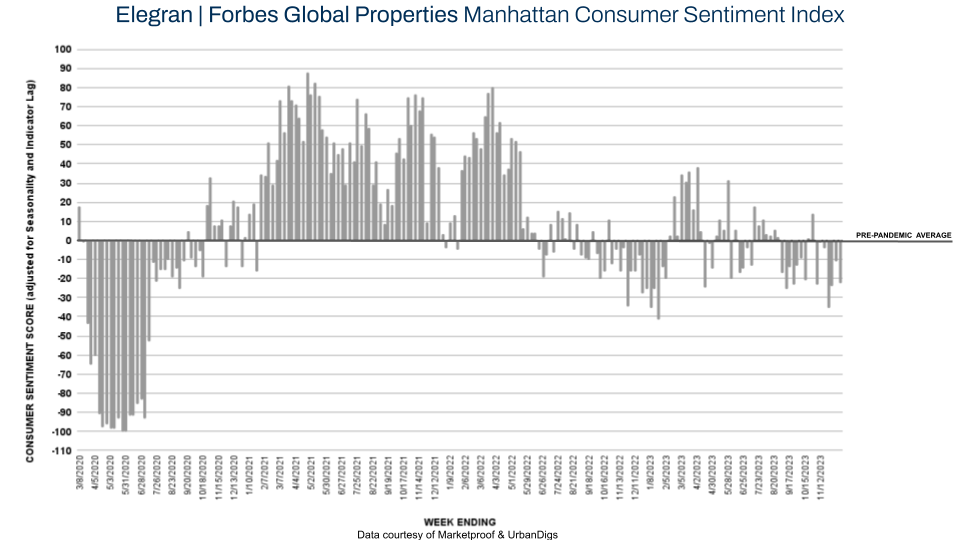

Manhattan Consumer Sentiment

This week, Manhattan’s score on the Elegran | Forbes Global Properties Manhattan Consumer Sentiment Index decreased from -11 to -22. As we learn from the chart below, the borough has spent roughly half the year above its pre-pandemic benchmark and the other half below it. 152 contracts were signed this week compared to 172 last week.

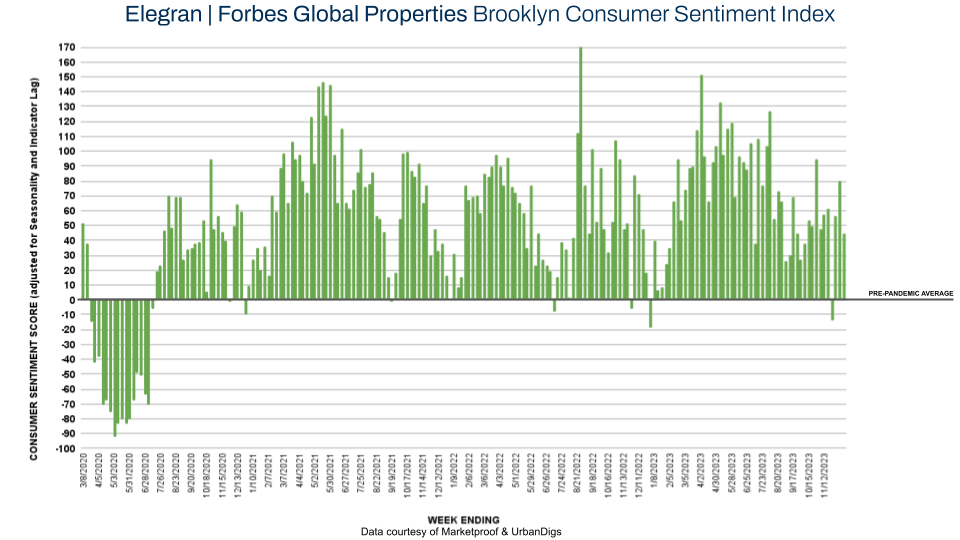

Brooklyn Consumer Sentiment

This week, Brooklyn’s score on the Elegran | Forbes Global Properties Brooklyn Consumer Sentiment Index (below) slipped from +80 to +45. 114 contracts were signed this week versus 133 last week.

New Development Insights

Marketproof reported that 35 new development contracts were signed in 29 buildings this week. The following buildings were the top-selling new developments of the week:

- THE BROOKLYN TOWER (Downtown Brooklyn) and 134-16 35TH AVENUE (Flushing) each reported three contracts.