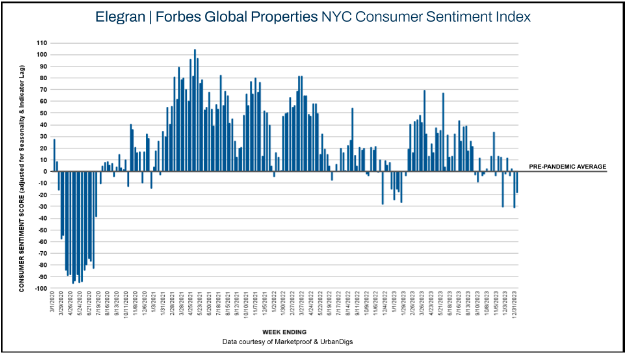

A New Year

As we welcome the New Year, our Elegran | Forbes Global Properties NYC Consumer Sentiment Index improved from -32 to -18 over the New Year week. This indicates that current consumer sentiment is now -18% lower than the average sentiment between January 5, 2015, and February 29, 2020.

For potential buyers who have been hesitating, now may be your time to act. The market has shown increased activity due to recent decreases in interest rates, encouraging some buyers to enter the market.

Buyers, this is your opportunity: Lower activity, reduced prices, greater negotiability, and a challenging listing environment offer a unique moment. As spring listings near, options will expand while putting pressure on unsold inventory. Those looking for a "deal" should focus on listings that have been on the market for 4+ months with multiple price reductions.

Sellers should keep a close watch on competing properties and be ready to adjust their prices based on new inventory to remain attractive to active buyers.

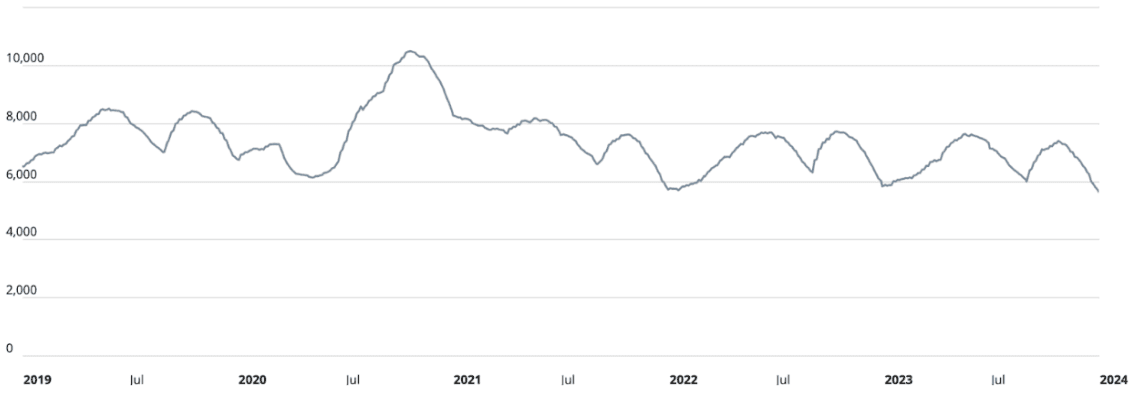

Manhattan Supply

As we would expect from analyzing the repetitive pattern of the chart below, supply reached the second peak of the year during October and will continue to retreat until early January. Why is the supply count important? The answer for many national markets is that supply can become sparse enough to struggle to satisfy demand, and prices can inflate substantially for this reason. But in NYC, there is far more supply than demand. This week, Manhattan’s ratio is 5,627 units of supply to 140 units of demand.

Manhattan Supply | Data courtesy of UrbanDigs

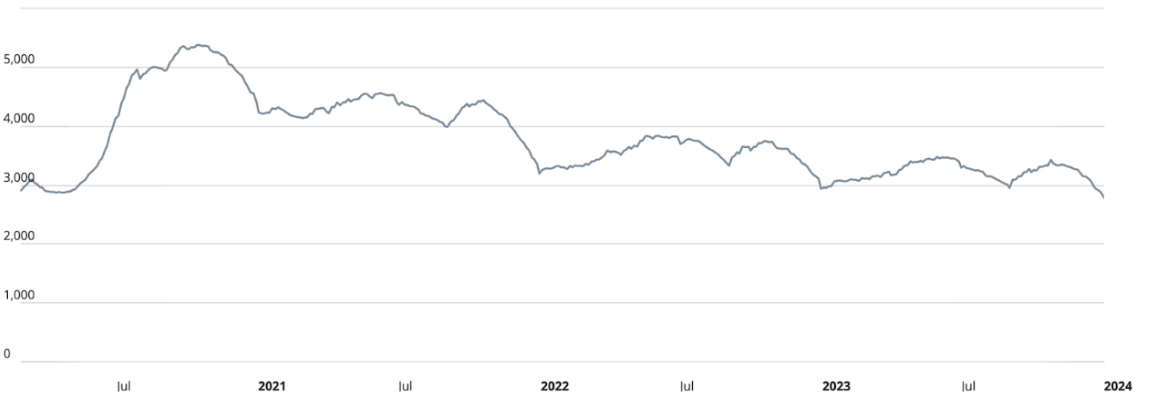

Brooklyn Supply

As we would expect, given the chart below, the metric is in decline and will continue to retreat until early January. The 2,774 units available are far more than are necessary to satisfy this week’s demand of 79 units.

Brooklyn Supply | Data courtesy of UrbanDigs

Manhattan Pending Sales

Pending sales declined this week, continuing an expected seasonal trend. Pending sales stand at 2,443 units. Expect pending sales to continue trickling lower through February or March, when contract activity is expected to further accelerate ahead of the traditionally busy spring market.

Brooklyn Pending Sales

Pending sales climbed slightly this week to 1,816 units. However, the metric should stay relatively flat and do so through the remainder of the Winter season.

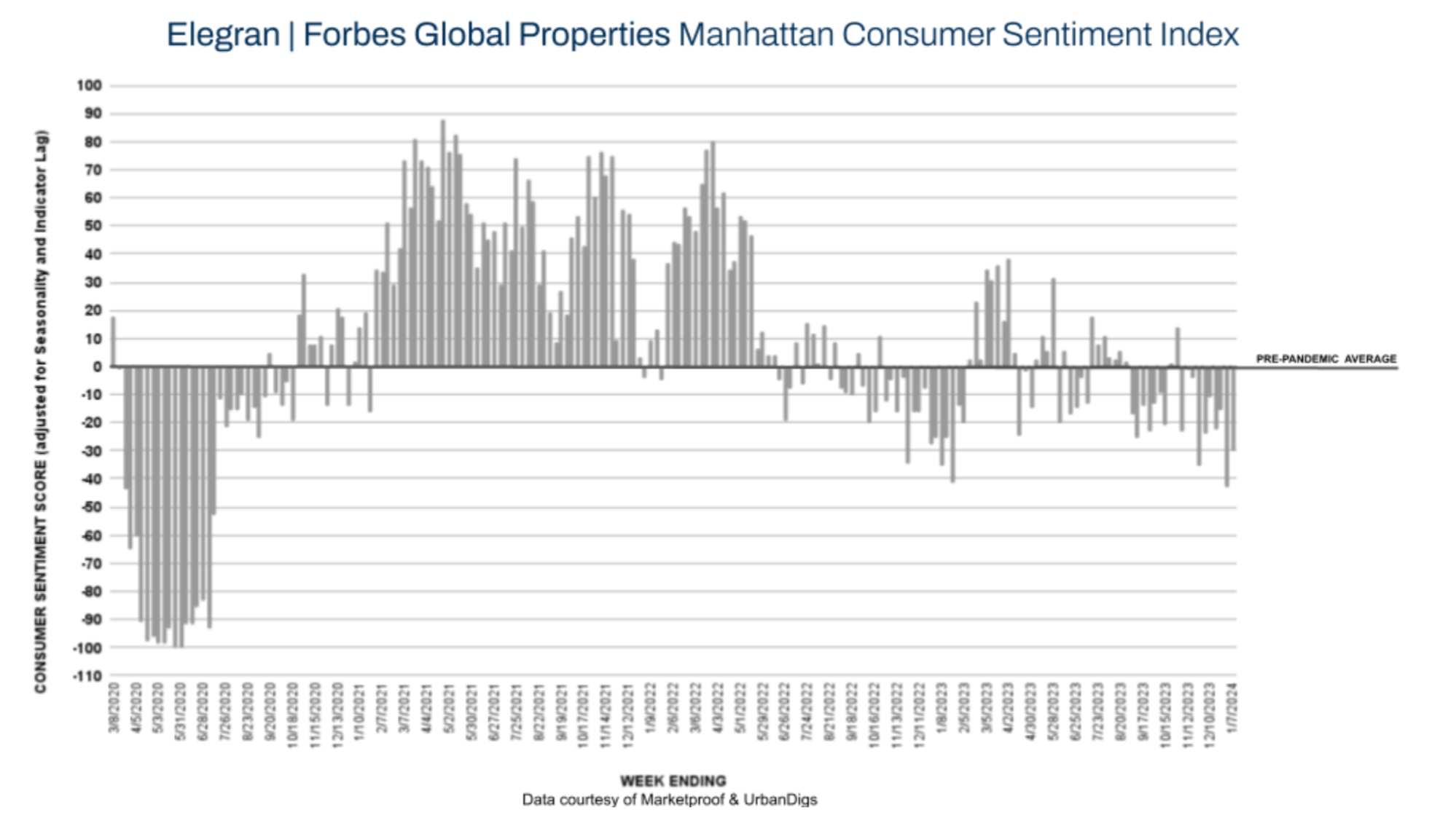

Manhattan Consumer Sentiment

This week, Manhattan’s score on the Elegran | Forbes Global Properties Manhattan Consumer Sentiment Index increased from –43 to —30. This week, 140 contracts were signed, compared to 111 last week.

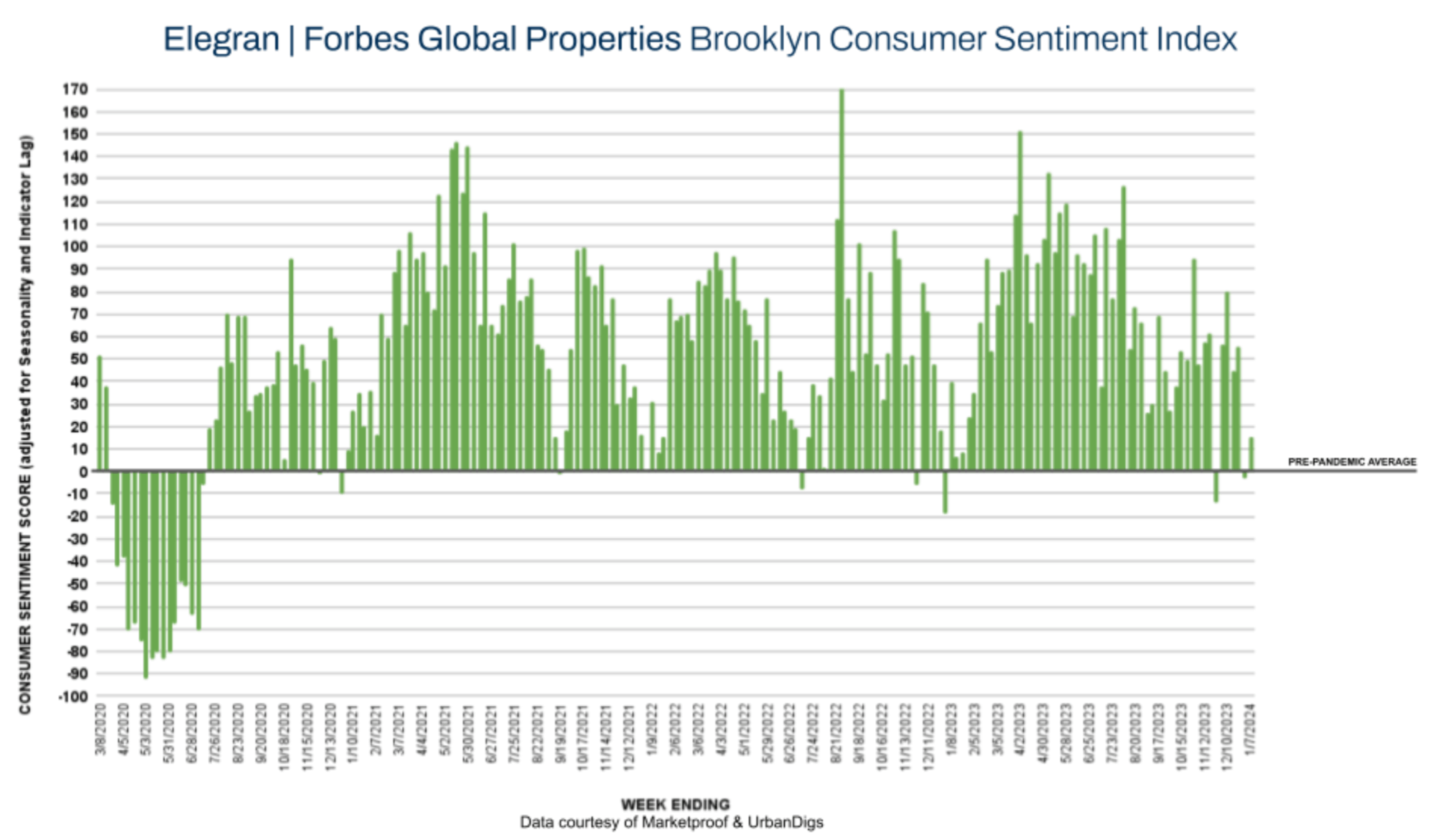

Brooklyn Consumer Sentiment

This week, Brooklyn’s score on the Elegran | Forbes Global Properties Brooklyn Consumer Sentiment Index (below) increased from -3 to +15. This week, 79 contracts were signed, versus 78 last week.

New Development Insights

Marketproof reported that 36 new development contracts were signed in 30 buildings this week. The following buildings were the top-selling new developments of the week:

- One Manhattan Square (Two Bridges) reported two contracts

- The Lumin (Greenpoint) reported four contracts.