Contract Volume is Light: Signs of a Slow[er] Spring Season in NYC Real Estate

The Manhattan real estate market is experiencing a deceleration in contract volume, suggesting a cooling off in the traditionally vibrant spring season. Buyers may pause as they navigate challenges: rising interest rates, declining stock markets, increasing geopolitical tensions, an upcoming election, and shifting forecasts about Federal Reserve rate cuts.

Impact of Economic and Geopolitical Factors

Financing buyers are particularly affected by the spike in interest rates, which have returned to their highest levels since last autumn, prompting a reevaluation of the rent-versus-buy decision. Cash buyers, who are more typically engaged in discretionary purchases, may hesitate amid these uncertain times. Recent geopolitical developments, especially the tension between Israel and Iran, add to this uncertainty. While these events have not yet impacted this week’s contract activities, their effects may become apparent shortly.

Market Trends: Manhattan and Brooklyn

In Manhattan, contract activity fell by 12% compared to last year's week and was 24% lower than in 2019. Conversely, Brooklyn saw a decrease of 9% from last year but a notable increase of 60% compared to 2019, highlighting a dynamic shift in buyer interest or market recovery.

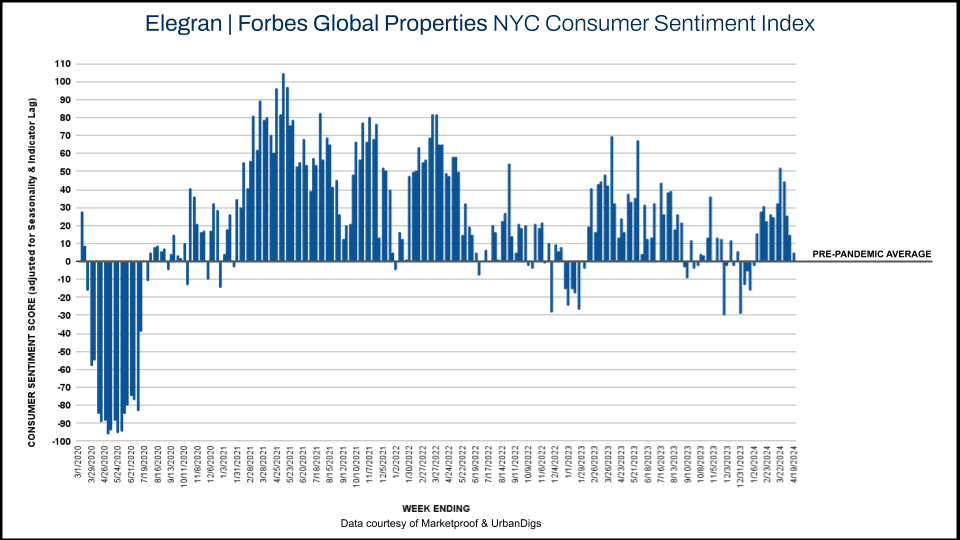

Inventory Levels and Consumer Sentiment

The market is observing an increase in inventory, which is expected during this season and might provide buyers with some negotiating power. According to the Elegran | Forbes Global Properties NYC Consumer Sentiment Index, sentiment aligns closely with the pre-pandemic average at a +5 this week.

Rental Market Dynamics

As we approach the peak rental season, there is momentum in the rental sector, with the highest number of new leases signed in a week since last September. Additionally, there has been a slight decrease in overall inventory, indicating a strengthening rental market.

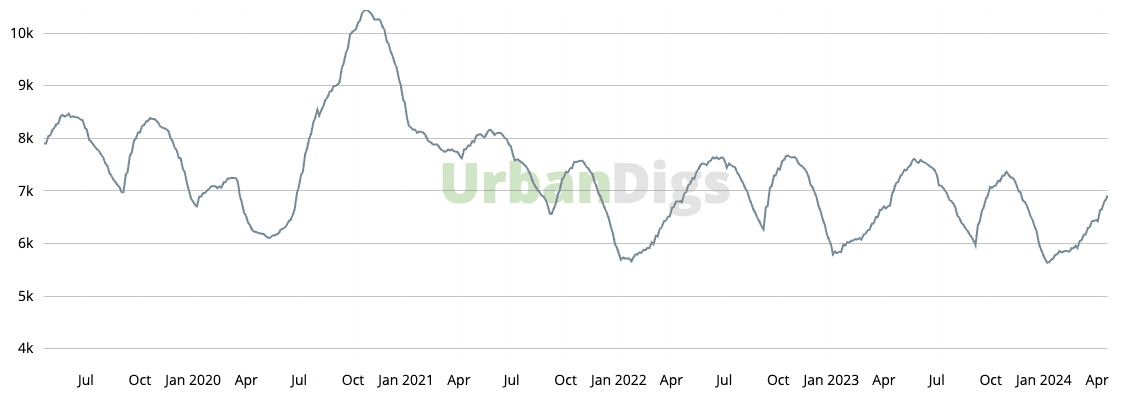

Manhattan Supply

Supply jumped 2.4% to 6,924 units for sale as 435 new listings came to market this week.

Manhattan Supply | Data courtesy of UrbanDigs

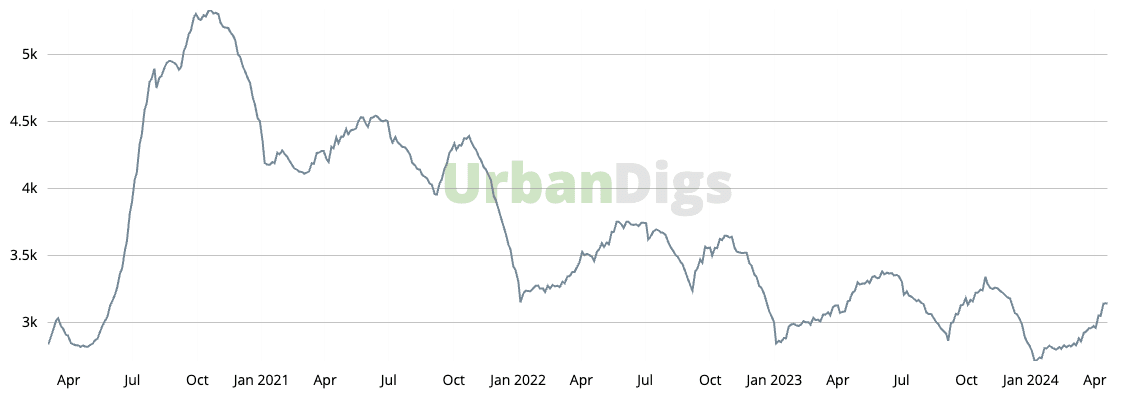

Brooklyn Supply

Supply increased by almost 1% to 3,145 units for sale as 200 new listings came to market this week.

Brooklyn Supply | Data courtesy of UrbanDigs

Manhattan Pending Sales

Pending sales increased by almost 2% to 2,860 units this week.

Brooklyn Pending Sales

Pending sales increased by 2% to 1,845 units this week.

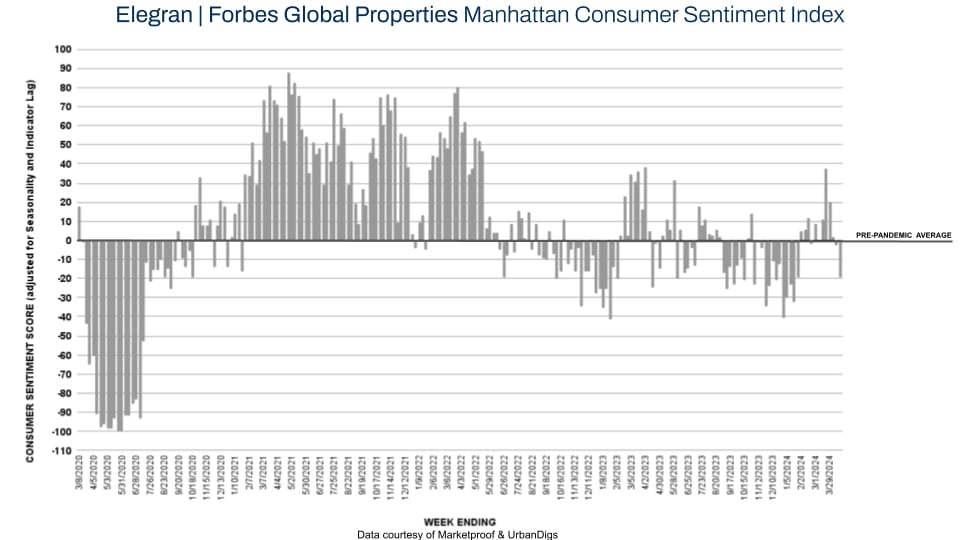

Manhattan Consumer Sentiment

This week, Manhattan’s score on the Elegran | Forbes Global Properties Manhattan Consumer Sentiment Index decreased from -2 to -20, as 204 contracts were signed, a 15% decrease from last week. The Sentiment Index continued to decrease for the second week in a row as contract activity is coming in comparatively light for the spring season.

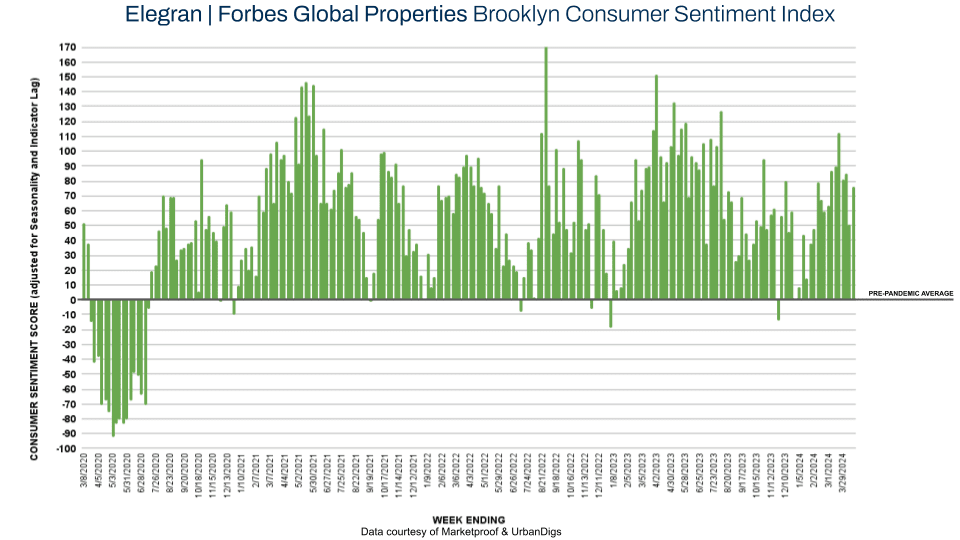

Brooklyn Consumer Sentiment

This week, Brooklyn’s score on the Elegran | Forbes Global Properties Brooklyn Consumer Sentiment Index increased from +51 to +76, as 145 contracts were signed, a 16% increase from last week.

New Development Insights

Marketproof reported that 45 new development contracts were signed in 36 buildings this week. The following buildings were the top-selling new developments of the week:

- Claremont Hall (Morningside Heights) reported 3 contracts

- Elysium (Prospect Lefferts Gardens) reported 3 contracts.