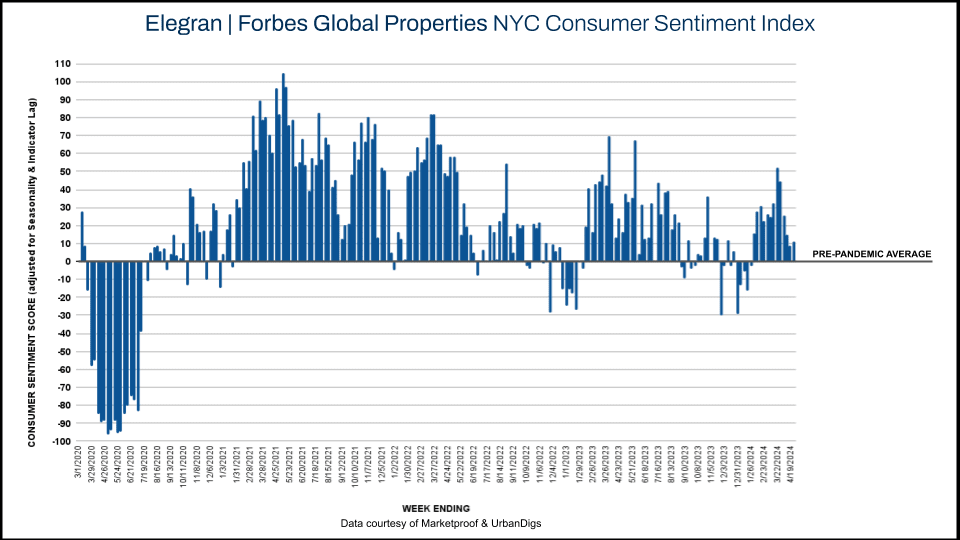

Equities Rebound & Contract Volumes Steady

Manhattan's contract volume increased by 12% this week, rebounding from last week. Overall, the contract volume in Manhattan and Brooklyn remained consistent with the two-month average. As a result, the Elegran | Forbes Global Properties NYC Consumer Sentiment Index measured +11 this week.

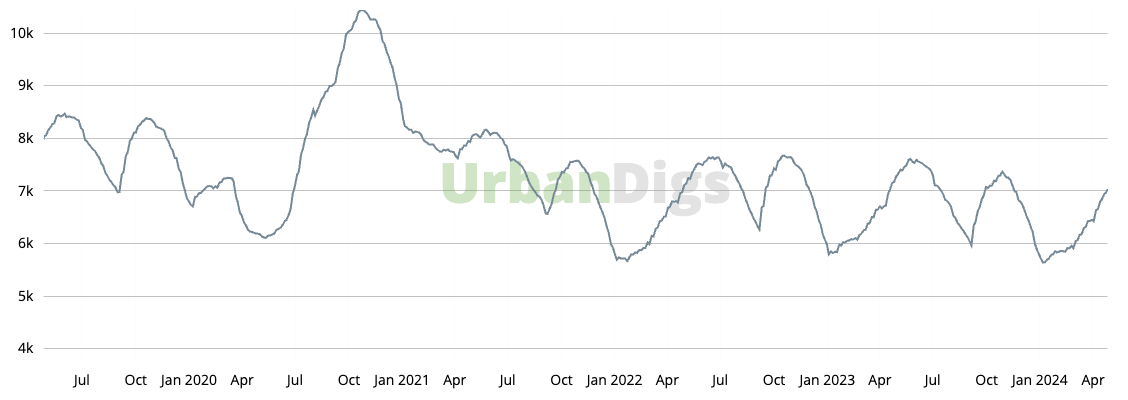

As the spring listing season draws nearer to a close, new listings continue to enter the market. This week, the total supply in Manhattan exceeded 7,000 units for the first time since last fall, although it is still 3% lower than the previous year's figures. In Brooklyn, the supply situation remained largely unchanged from the previous week and continues to be about 3% below last year’s levels.

The equities market experienced a significant rebound this week, recovering from last week's sell-off. This recovery was influenced by mixed inflation data, positive corporate earnings reports, and additional commentary from the Federal Reserve. However, it’s important to note that interest rates have risen this week, which could impact future market movements.

Buyers' confidence in the real estate market is closely linked to the economy's overall health and global stability. When stock markets perform well and economic indicators are positive, potential buyers are more comfortable and confident about purchasing real estate. Conversely, factors like rising inflation or geopolitical tensions can make buyers hesitant, as these elements introduce uncertainty into the market.

Manhattan Supply

Supply jumped by 1.8% to 7,046 units for sale as 426 new listings came to market this week. Supply has crossed above 7,000 units for the first time since mid-November 2023 and remains about 3% lower than last year.

Manhattan Supply | Data courtesy of UrbanDigs

Brooklyn Supply

Supply slightly decreased to 3,142 units for sale as 197 new listings came to market this week.

Brooklyn Supply | Data courtesy of UrbanDigs

Manhattan Pending Sales

Pending sales increased by almost 2% to 2,913 units this week.

Brooklyn Pending Sales

Pending sales increased by 1.6% to 1,874 units this week.

Manhattan Consumer Sentiment

This week, Manhattan’s score on the Elegran | Forbes Global Properties Manhattan Consumer Sentiment Index increased from -20 to -7 as 229 contracts were signed, a 12% increase from last week. The Sentiment Index continues to have a negative metric for the third week as contract activity is coming in comparably light for the spring season.

Brooklyn Consumer Sentiment

This week, Brooklyn’s score on the Elegran | Forbes Global Properties Brooklyn Consumer Sentiment Index decreased from +76 to +72 as 142 contracts were signed, a 2% decrease from last week.

New Development Insights

Marketproof reported that 41 new development contracts were signed in 34 buildings this week. The following buildings were the top-selling new developments of the week:

- Eastlight (Kips Bay), The Treadwell (Lenox Hill), and 50 W 66th St (Lincoln Square) each reported 2 contracts

- 110 North First (Williamsburg), Elysium (Prospect Lefferts Gardens), and 747 Dean St (Prospect Heights) each reported 2 contracts.