Summer Cooldown Sets In, but the Pipeline Holds

New York City's housing market downshifted this week as the summer slowdown took hold. Signed contracts pulled back in both boroughs and sentiment cooled meaningfully - but pending sales continued to climb, a reminder that deals already in motion are still moving toward the closing table. The headline softening is best read as seasonal, compounded by a contract backlog still working through the system after the Juneteenth-shortened week.

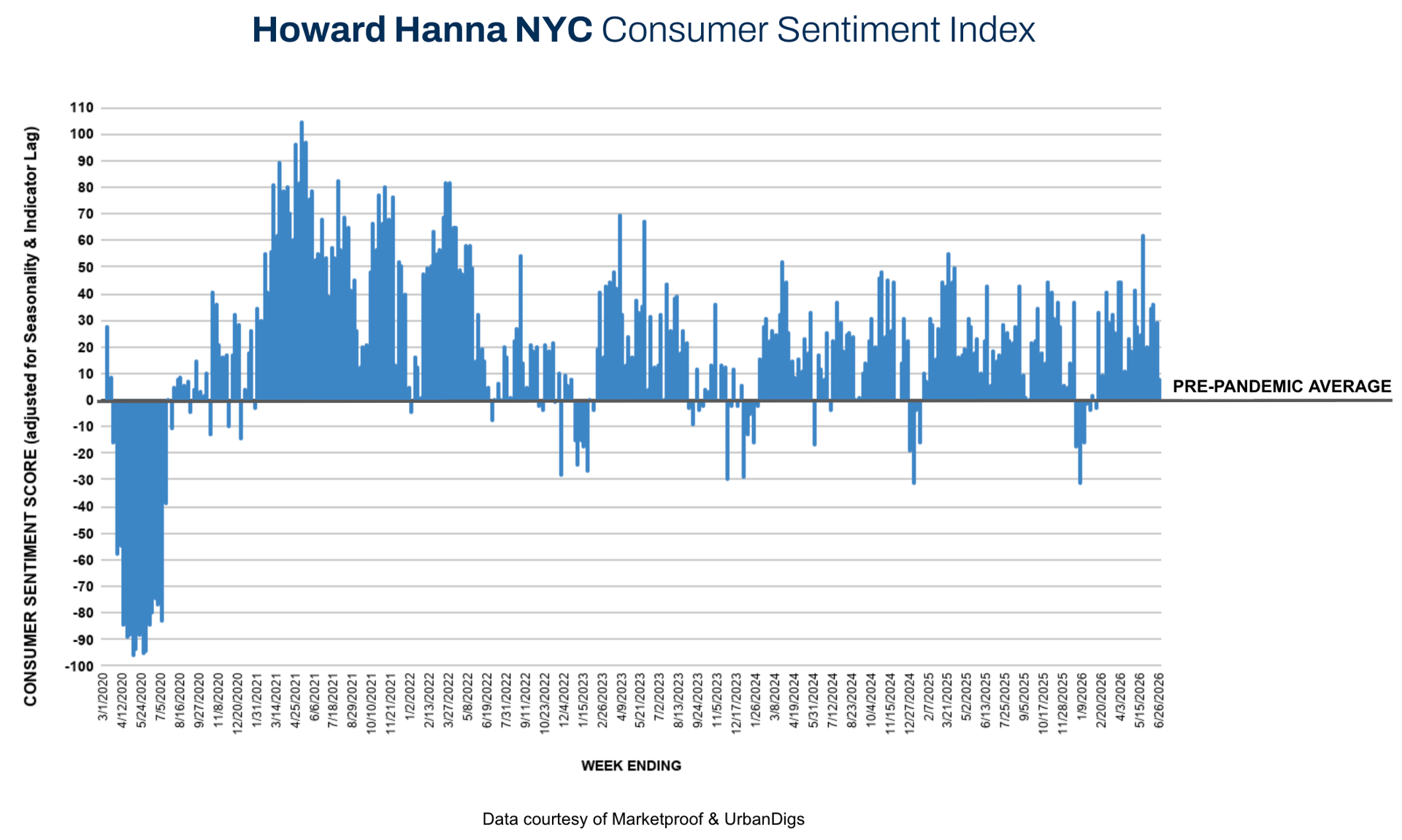

The Howard Hanna NYC Consumer Sentiment Index decreased from +29% to +8% — a typical week-to-week fluctuation that also reflects backlog contracts not yet recorded, following the shortened Juneteenth holiday week that compresses reported activity.

What This Means for Summer 2026

For buyers: Pending sales are still rising in both boroughs and Manhattan inventory remains 8.2% below last year. The seasonal lull in new contract activity may open a brief window, but the underlying supply constraint has not eased - well-priced homes still move.

For sellers: New-contract momentum has cooled, and new listings are pulling back as well. In a quieter summer market, pricing precision matters more, not less - well-priced product still trades, while aspirational pricing sits.

Overall, the week marks the expected start of the summer slowdown: lighter contract volume, softer sentiment, and tightening supply, offset by a forward pipeline that continues to build in both boroughs.

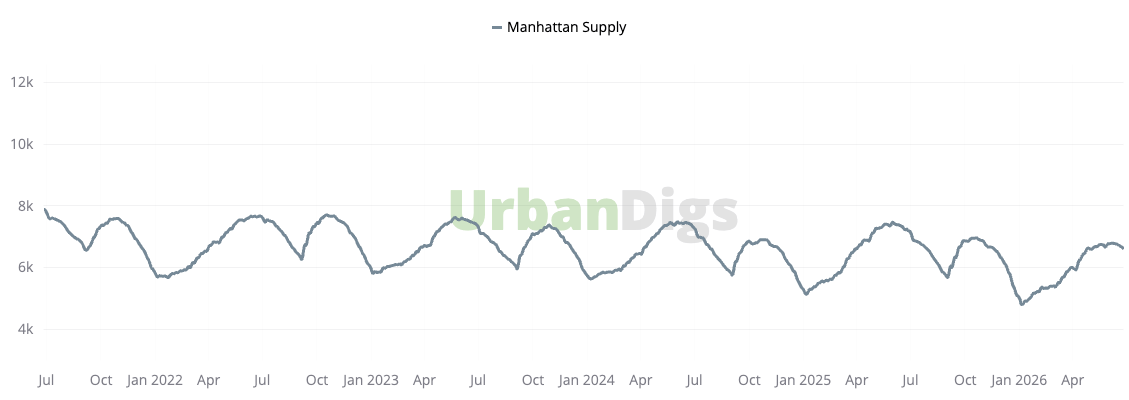

Manhattan Supply

Manhattan Supply: Inventory Tightens Further Below Last Year

Manhattan active inventory held roughly steady at 6,624 homes (−0.9% week-over-week | −8.2% year-over-year), remaining notably below last year's level. New listings totaled 232 units (−26% week-over-week | −11% year-over-year), reflecting a sharp pullback in seller activity on both timeframes.

The takeaway for buyers and sellers: the year-over-year supply deficit continues to deepen, keeping the structural backdrop tight even as new-contract activity cools. For buyers, fewer listings means well-priced homes still attract attention; for sellers, the thin new-listing flow limits direct competition for a well-positioned home.

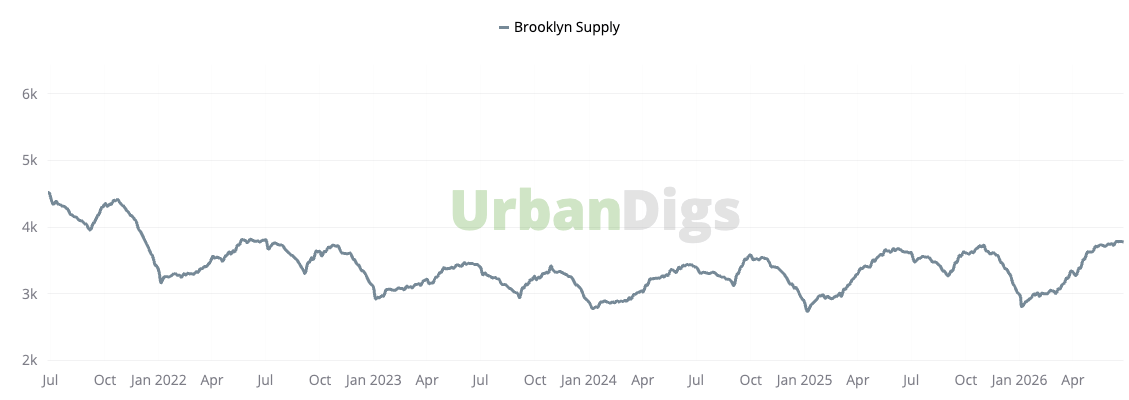

Brooklyn Supply

Brooklyn Supply: Flat on the Week, Higher Than Last Year

Brooklyn inventory remained virtually unchanged at 3,786 homes (no change week-over-week | +4.5% year-over-year) - flat against the prior week with continued year-over-year growth. New listings held roughly steady at 199 units (−1% week-over-week | +18% year-over-year), a modest year-over-year increase in seller participation.

This pattern suggests Brooklyn supply is holding at a level modestly above last year rather than expanding rapidly. For buyers, Brooklyn continues to offer more room than Manhattan; for sellers, the year-over-year rise in listing flow underscores why accurate pricing matters from day one.

Pending Sales

Pending Sales: Forward Pipeline Keeps Building

Even as new-contract activity cooled, pending sales rose in both boroughs — a sign that deals already underway continue to progress toward closing.

- Manhattan pending sales: up +1.7% week-over-week to 4,131 units — a steady gain that signals a strengthening forward transaction pipeline.

- Brooklyn pending sales: up +2% week-over-week to 2,280 units — stable deal flow as buyers continue moving toward contract.

Photo by Rihards Gederts | Howard Hanna NYC

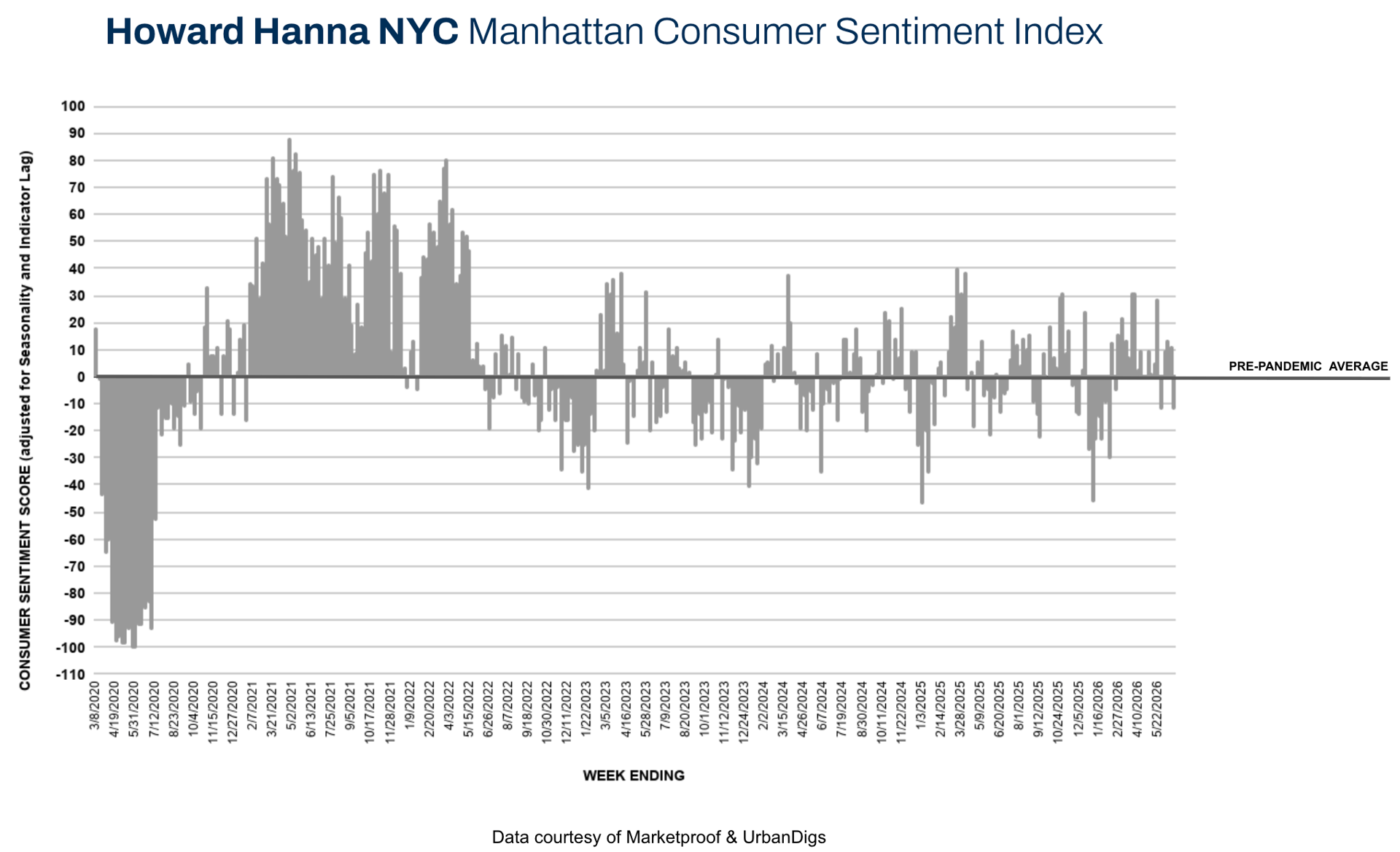

Manhattan Consumer Sentiment

Manhattan Consumer Sentiment: Cools Into Negative Territory

Manhattan recorded 219 signed contracts (−18% week-over-week | −5% year-over-year) — a noticeable pullback on both timeframes. The Howard Hanna NYC Manhattan Consumer Sentiment Index decreased from +11% to −12%, moving into negative territory as the summer slowdown sets in. Some of this reflects backlog contracts not yet recorded following the holiday-shortened calendar.

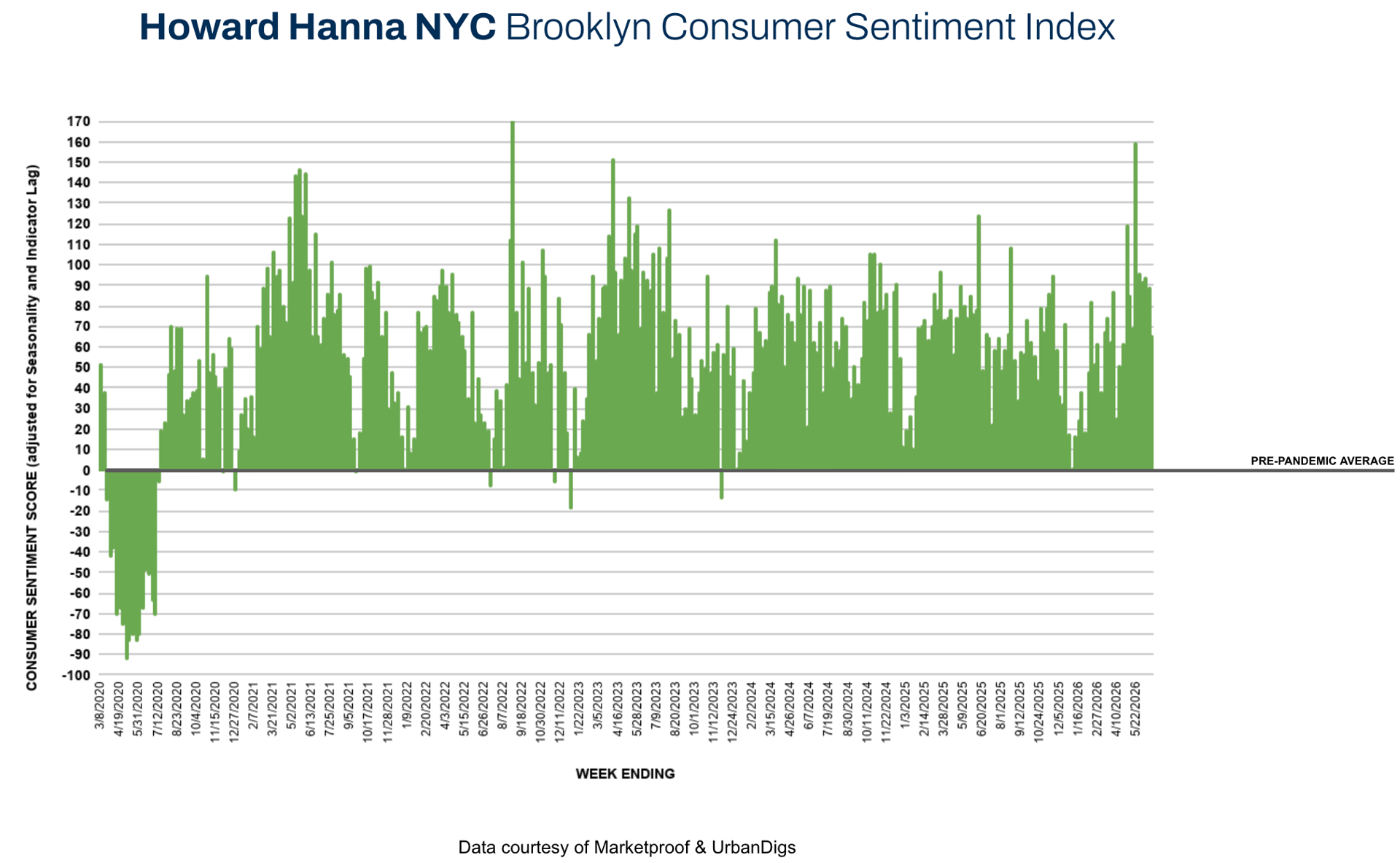

Brooklyn Consumer Sentiment

Brooklyn Consumer Sentiment: Softens but Stays Positive

Brooklyn recorded 137 signed contracts (−12% week-over-week | −1% year-over-year) — a modest contraction on both timeframes. The Howard Hanna NYC Brooklyn Consumer Sentiment Index decreased from +89% to +65%, a meaningful weekly step down that nonetheless leaves Brooklyn firmly in positive territory as the market moves through summer.

New Development Insights

New Development Insights: South Slope and Yorkville Lead

According to Marketproof data, new development activity recorded 25 signed contracts across 21 buildings during the week of June 22, 2026. Top-performing developments included:

- 222 16th Street (South Slope) with three signed contracts

- The Strathmore (Yorkville) with two signed contracts

Demand continues to concentrate in well-located, lifestyle-oriented developments with strong pricing alignment, reinforcing buyer preference for turnkey product in prime neighborhoods.

If you would like to chat about the most recent market activity,

feel free to contact us at [email protected] or

connect with one of our Advisors.

Howard Hanna NYC brings the nation’s largest independent and family-owned brokerage to New York City, uniting the strength of a national network with the insight and sophistication of a local firm. Formed through joining forces with Elegran Real Estate, Howard Hanna NYC delivers a seamless, full-service experience backed by more than 15,000 agents across 500 offices in 14 states. The firm’s forward-thinking, agent-first culture continues to shape the future of real estate across Manhattan and the Tri-State area. Learn more at www.howardhannanyc.com.

```